Comcast Corporation, the largest cable and broadband provider in the United States, ended 2025 with 50.77 million total customer relationships across its Connectivity & Platforms segment. The company faces a structural divergence: its legacy broadband and pay-TV businesses are steadily losing subscribers, while its wireless (Xfinity Mobile) and streaming (Peacock) divisions are experiencing strong growth. In 2025, Comcast lost roughly 587,000 domestic broadband customers and 1.25 million video subscribers, but added a record 1.5 million wireless lines and grew Peacock to 44 million paid subscribers. Analysts do not expect material broadband customer growth until 2027, making 2026 a pivotal transition year.

Domestic Broadband Customers

Current Status (End of 2025)

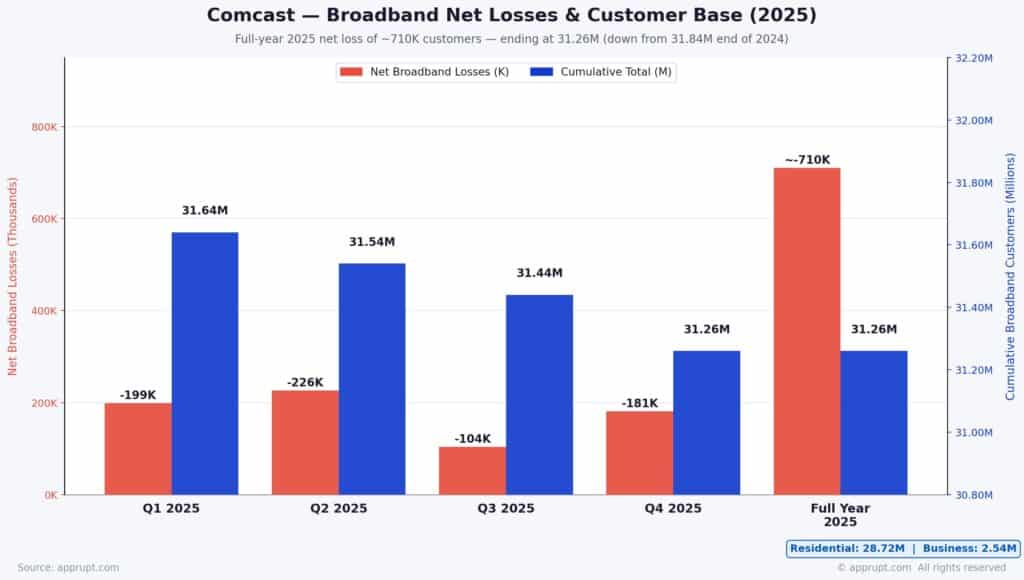

Comcast ended 2025 with 31.26 million total domestic broadband customers, comprising 28.72 million residential customers and 2.54 million business customers. This represents a decline of approximately 587,000 from the 31.84 million at the end of 2024.

The full-year 2025 quarterly breakdown of broadband net losses:

| Quarter | Net Losses | Cumulative Total |

| Q1 2025 | -199,000 | 31.64M |

| Q2 2025 | -226,000 | 31.54M |

| Q3 2025 | -104,000 | 31.44M |

| Q4 2025 | -181,000 | 31.26M |

| Full Year | ~-710,000 | 31.26M |

Historical Broadband Subscriber Trend

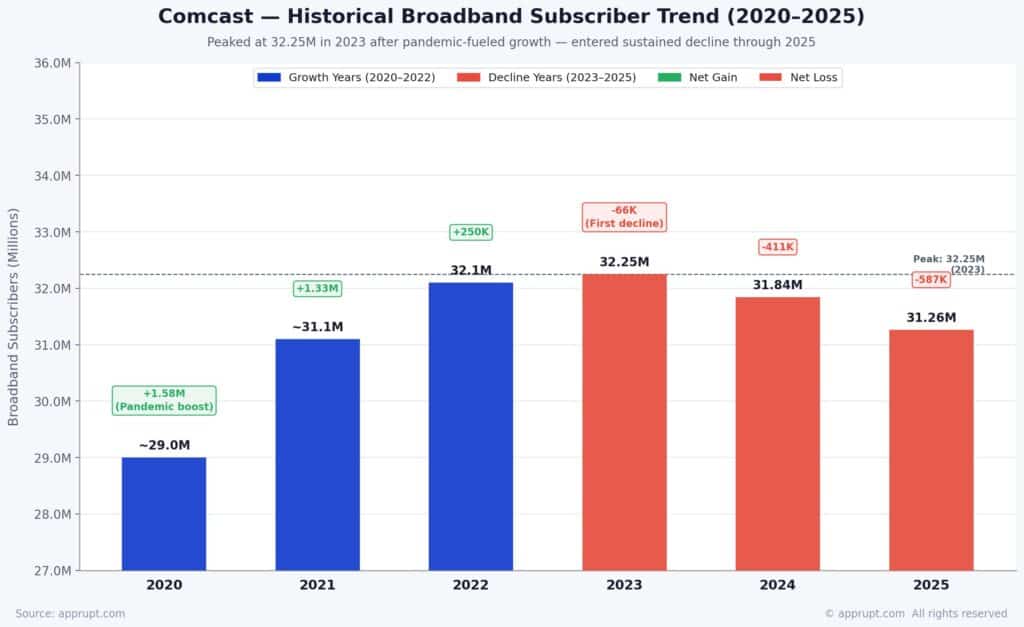

Comcast’s broadband subscriber count peaked in 2023 at 32.25 million after years of pandemic-fueled growth, then entered a sustained decline:

| Year | Broadband Subs (M) | Net Change |

| 2020 | ~29.0 | +1.58M (pandemic boost) |

| 2021 | ~31.1 | +1.33M |

| 2022 | 32.1 | +250,000 |

| 2023 | 32.25 | -66,000 (first decline) |

| 2024 | 31.84 | -411,000 |

| 2025 | 31.26 | -587,000 |

Since Q1 2023 — the last quarter Comcast posted positive broadband net adds (just 5,000) — the company has lost over one million residential and business broadband customers.

Drivers of Broadband Decline

Three factors are eroding Comcast’s broadband base:

- Fiber overbuilders: Telcos and fiber operators are overlaying Comcast’s cable networks with FTTH, offering gigabit speeds with faster upload capabilities at competitive prices.

- Fixed wireless access (FWA): Verizon and T-Mobile’s 5G home internet offerings are siphoning price-sensitive customers. The national mobile-only share of broadband subscribers has rebounded from 7% to nearly 11% (pre-pandemic levels).

- End of the Affordable Connectivity Program (ACP): The ACP’s expiration contributed to a wave of disconnects among subsidy-dependent households transitioning to mobile-only broadband.

Comcast CFO Jason Armstrong acknowledged that fiber competition intensified in Q4 2025 and expects it to continue going forward, while fixed wireless pressure remains “pretty consistent”.

2026 Broadband Outlook and Beyond

Analyst Projections

Analysts broadly agree that Comcast will not see material broadband customer growth until at least 2027. Industry forecasts suggest cable broadband could lose another million subscribers in 2026 as 5G and fiber penetration expand further. Goldman Sachs has downgraded Comcast, expecting Connectivity & Platforms EBITDA to decline approximately 4% year-over-year for several quarters, driven by the decision not to raise broadband prices in early 2026.

Comcast’s Defensive Strategy

To stabilize its broadband base, Comcast has launched the “most significant broadband go-to-market shift in its history”:

- Price locks: New plans include five-year price guarantees, and Comcast will not raise broadband rates in the first half of 2026.

- Simplified pricing: National internet plans feature everyday pricing with everything included — modem, unlimited data — across four speed tiers.

- Free wireless bundling: Most broadband plans now include a free Xfinity Unlimited mobile line for one year, with conversion to paid service expected in H2 2026.

- Network upgrades: Ongoing DOCSIS 4.0 deployment and mid-split technology expansion to deliver multi-gigabit symmetrical speeds.

Management reported “lower voluntary churn” under the new strategy and aims to migrate the majority of its 31.3 million broadband subscribers to the new pricing plans as quickly as possible.

The 2026 Conversion Test

A critical inflection point for Comcast comes in the second half of 2026, when the free wireless lines offered to broadband customers hit their one-year anniversary and transition to paid billing. Approximately half of 2025’s wireless additions were customers taking up the free line offer. Whether those customers stay and pay — or cancel — will reveal the true effectiveness of Comcast’s converged connectivity strategy and determine the trajectory for 2027 and beyond.

Domestic Video (Pay TV) Customers

Accelerating Cord-Cutting

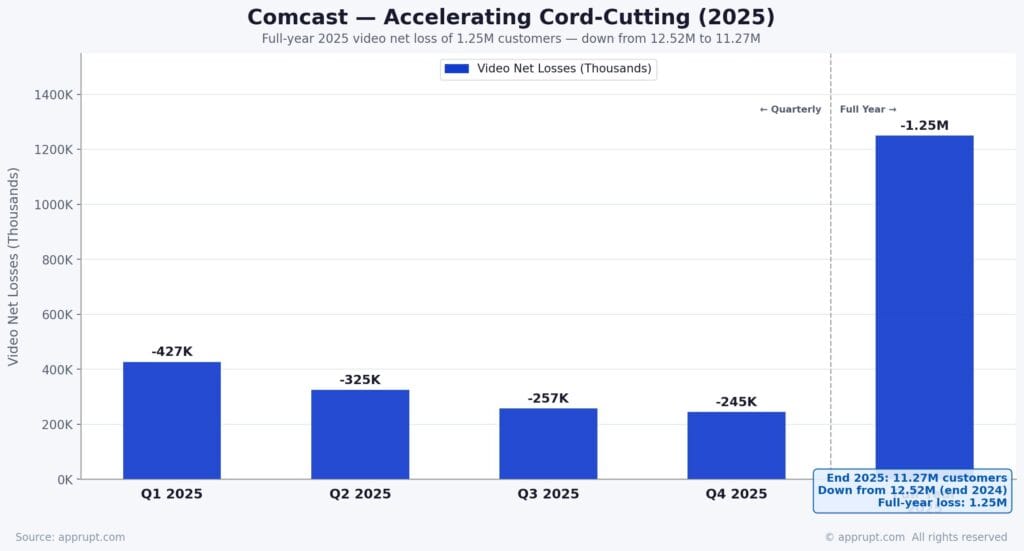

Comcast ended 2025 with 11.27 million domestic video customers, down from 12.52 million at the end of 2024 — a loss of 1.25 million in a single year. The quarterly losses in 2025:

| Quarter | Video Net Losses |

| Q1 2025 | -427,000 |

| Q2 2025 | -325,000 |

| Q3 2025 | -257,000 |

| Q4 2025 | -245,000 |

| Full Year | -1.25M |

Historical Video Decline

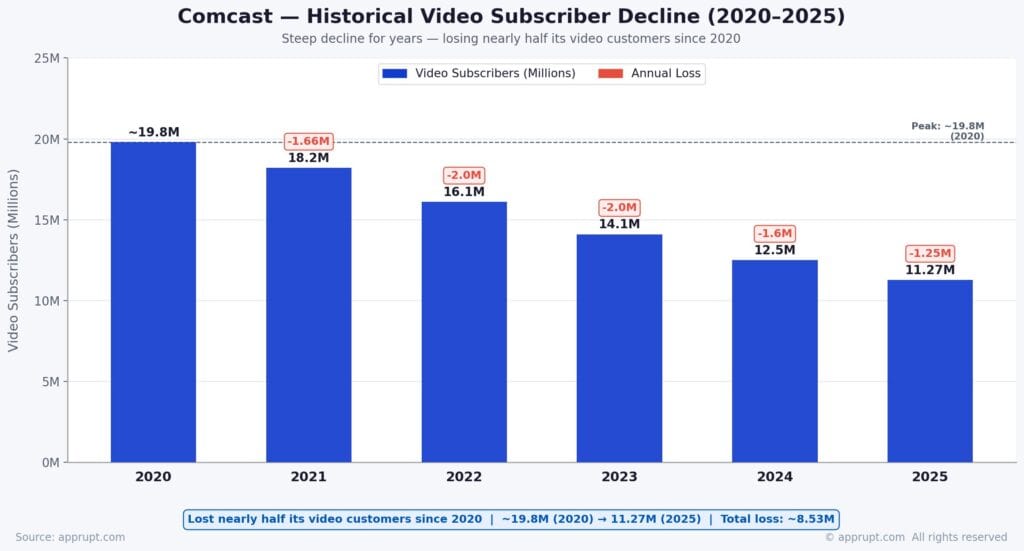

Comcast’s video subscriber base has been in steep decline for years, losing nearly half its customers since 2020:

| Year | Video Subs (M) | Annual Loss |

| 2020 | ~19.8 | — |

| 2021 | 18.2 | -1.66M |

| 2022 | 16.1 | -2.0M |

| 2023 | 14.1 | -2.0M |

| 2024 | 12.5 | -1.6M |

| 2025 | 11.27 | -1.25M |

Across the broader US market, 68.7 million households still subscribe to cable TV as of 2025, down from 105 million in 2010. Cord-cutting households have more than doubled since 2018, reaching a projected 77.2 million by 2025.

Outlook for Video

With the January 2026 spin-off of Versant Media Group (containing CNBC, MSNBC, and other cable networks), Comcast’s remaining video business is increasingly centered on streaming and live sports. The rate of video subscriber losses slowed in Q4 2025 compared to the prior year period (245,000 vs. 311,000), but the structural decline toward streaming remains irreversible.

Wireless (Xfinity Mobile) Customers

Record Growth

Xfinity Mobile delivered its best year ever in 2025, adding 1.5 million net wireless lines and surpassing 9.3 million total lines. This represents over 15% penetration of Comcast’s domestic residential broadband customer base.

| Quarter | Wireless Net Adds |

| Q1 2025 | 323,000 |

| Q2 2025 | 378,000 |

| Q3 2025 | 414,000 (record) |

| Q4 2025 | 364,000 |

| Full Year | ~1.5M |

Historical Wireless Growth

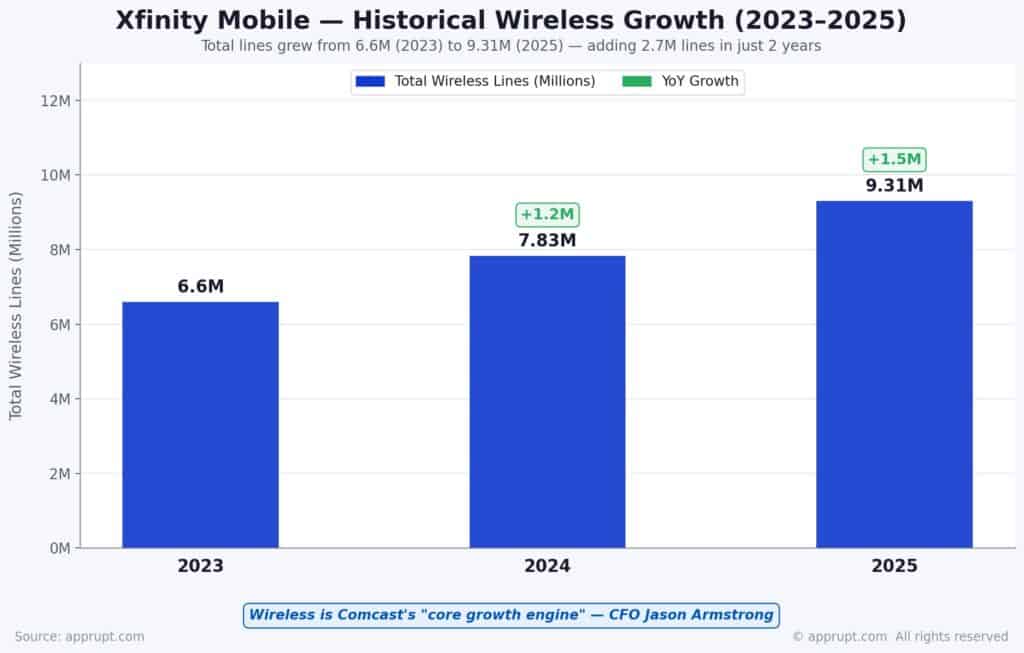

Wireless has been Comcast’s “core growth engine,” as described by CFO Jason Armstrong:

| Year | Total Lines (M) | YoY Growth |

| 2023 | 6.6 | — |

| 2024 | 7.83 | +1.2M |

| 2025 | 9.31 | +1.5M |

The service operates as an MVNO through a deal with Verizon, with a recently updated agreement to support “mutual profitable growth”. Comcast and Charter also signed a separate MVNO deal with T-Mobile for mid-size business wireless services.

2026 Wireless Outlook

Wireless subscriber growth is expected to continue in 2026, though the key uncertainty is the conversion rate of free promotional lines to paid subscriptions in H2 2026. Management expects “a meaningful portion” to convert to paid customers. With only 15% of broadband subscribers currently also on Xfinity Mobile, Comcast sees a “huge runway for growth”. The broadband-wireless convergence strategy positions wireless as both a standalone growth driver and a tool to reduce broadband churn.

Peacock Streaming Subscribers

Reaching 44 Million

Peacock, NBCUniversal’s streaming platform, ended 2025 with 44 million paid subscribers, up 22% year-over-year from 36 million at the end of 2024. The growth was fueled by the debut of the NBA on NBC and Peacock, NFL Sunday Night Football, and original content.

Peacock Growth Trajectory

| Period | Paid Subscribers (M) |

| Q4 2022 | 21 |

| Q4 2023 | 31 |

| Q1 2025 | 41 |

| Q2 2025 | 41 |

| Q3 2025 | 41 |

| Q4 2025 | 44 |

Peacock Revenue and Profitability

Peacock generated $5.4 billion in full-year 2025 revenue, up 10% year-over-year. Q4 2025 revenue reached $1.6 billion, up 23% year-over-year. However, profitability remains elusive — Peacock posted a $552 million adjusted EBITDA loss in Q4 2025, wider than the $372 million loss a year earlier, largely due to costs from the new $2.7 billion-per-year NBA rights deal. Full-year EBITDA losses improved by over $700 million compared to 2024.

Peacock raised its ad-supported subscription price to $10.99/month in 2025, the industry’s highest ad-supported tier price, marking its third price hike since launch. Management signaled confidence that the price increases were “landing very well” with subscribers.

Total Customer Relationships

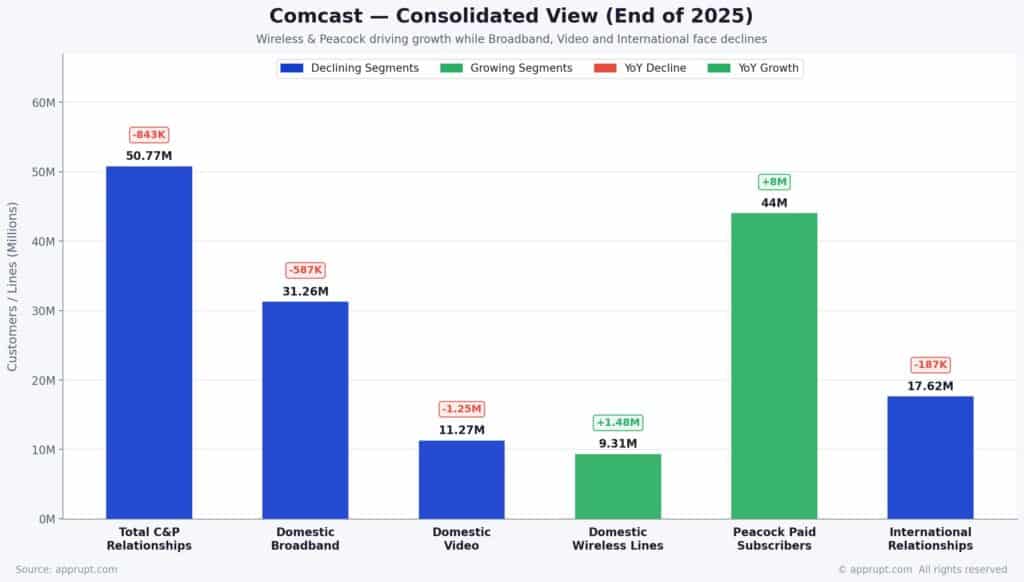

Consolidated View (End of 2025)

| Segment | Customers/Lines | YoY Change |

| Total C&P Relationships | 50.77M | -843K |

| Domestic Broadband | 31.26M | -587K |

| Domestic Video | 11.27M | -1.25M |

| Domestic Wireless Lines | 9.31M | +1.48M |

| Peacock Paid Subscribers | 44M | +8M |

| International Relationships | 17.62M | -187K |

Revenue per Customer

The average monthly total Connectivity & Platforms revenue per customer relationship stood at $132.64 at the end of 2025, up slightly from $132.10 a year earlier. Despite losing customers, Comcast has been growing revenue per relationship through ARPU increases, though this growth is slowing — domestic broadband ARPU rose just 1.1% in Q4 2025 as the company absorbs the impact of reduced rate hikes and free wireless line promotions.

Financial Context

Comcast’s total consolidated revenue was essentially flat at $123.71 billion in 2025, compared to $123.73 billion in 2024. The Connectivity & Platforms segment, which accounts for approximately 66% of total revenue, generated $81.3 billion. Full-year free cash flow reached a record $19.2 billion, up 53% year-over-year.

Despite customer losses in broadband and video, the company returned $11.7 billion to shareholders in 2025, including $6.8 billion in share repurchases that reduced shares outstanding by 5%.

Key Metrics to Watch in 2026 and Beyond

- Broadband stabilization: Whether the new pricing strategy, price locks, and bundling can slow or reverse broadband losses. Analysts target 2027 for potential stabilization.

- Wireless conversion rates: The H2 2026 billing transition for free promotional lines will test customer retention and the viability of the converged broadband-mobile model.

- Peacock path to profitability: With $5.4 billion in annual revenue and still-widening quarterly losses, Peacock’s ability to break even amid rising sports rights costs is a major earnings catalyst.

- Fiber and FWA competition: Fiber overbuild expansion and 5G FWA penetration will continue to pressure Comcast’s broadband pricing power and subscriber retention.

- ARPU trajectory: With broadband prices frozen through at least mid-2026, ARPU growth is expected to slow, pressuring the Connectivity & Platforms segment’s EBITDA by approximately 4% year-over-year.

- Broadband footprint expansion: Comcast’s buildout into previously unserved areas across Indiana, West Virginia, Pennsylvania, and Washington could provide a new source of net subscriber additions.