Roku is the dominant connected TV (CTV) platform in the United States, holding 37–39% of the CTV device market throughout 2024–2025 and approximately 34% of all smart TV OS unit shipments in Q1 2025. Over 21% of all U.S. TV viewing occurs on Roku-powered devices — more than all broadcast television. This report provides a detailed breakdown of Roku’s market share across CTV programmatic advertising, smart TV OS shipments, TV viewership, and regional markets, along with competitive positioning and the 2026 outlook.

CTV Device Market Share (Pixalate Data)

Pixalate’s quarterly CTV Device Market Share Reports — based on analysis of 22–27 billion open programmatic ad transactions — are the most frequently cited source for CTV device market share. Share of Voice (SOV) measures the percentage of open programmatic ads served on each device type.

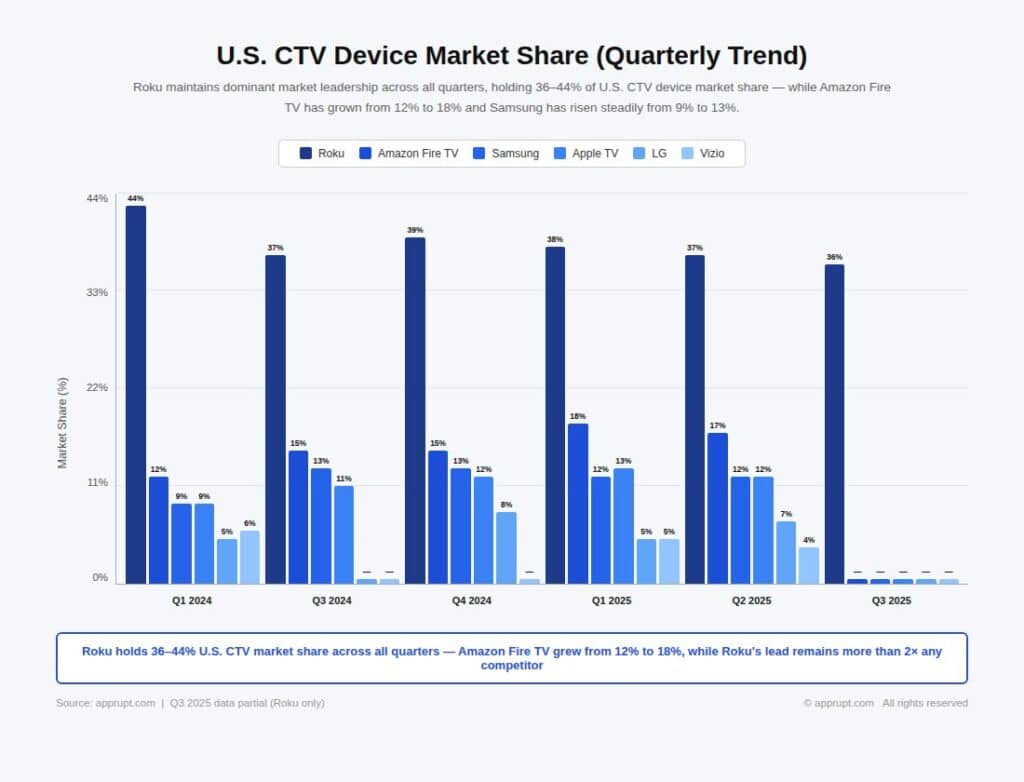

U.S. CTV Device Market Share (Quarterly Trend)

| Quarter | Roku | Amazon Fire TV | Samsung | Apple TV | LG | Vizio |

| Q1 2024 | 44% | 12% | 9% | 9% | 5% | 6% |

| Q3 2024 | 37% | 15% | 13% | 11% | — | — |

| Q4 2024 | 39% | 15% | 13% | 12% | 8% | — |

| Q1 2025 | 38% | 18% | 12% | 13% | 5% | 5% |

| Q2 2025 | 37% | 17% | 12% | 12% | 7% | 4% |

| Q3 2025 | 36% | — | — | — | — | — |

Roku’s U.S. CTV market share declined from a peak of roughly 55% in 2023 to 36–39% in 2024–2025, a drop of approximately 28–29% year over year. This decline reflects growing competition from Amazon Fire TV (+65% YoY in Q1 2025), Samsung (+51% YoY in Q4 2024), and Apple TV (+43% YoY in Q1 2025), rather than an absolute decline in Roku usage. Roku still holds more than double the share of its closest competitor in the U.S..

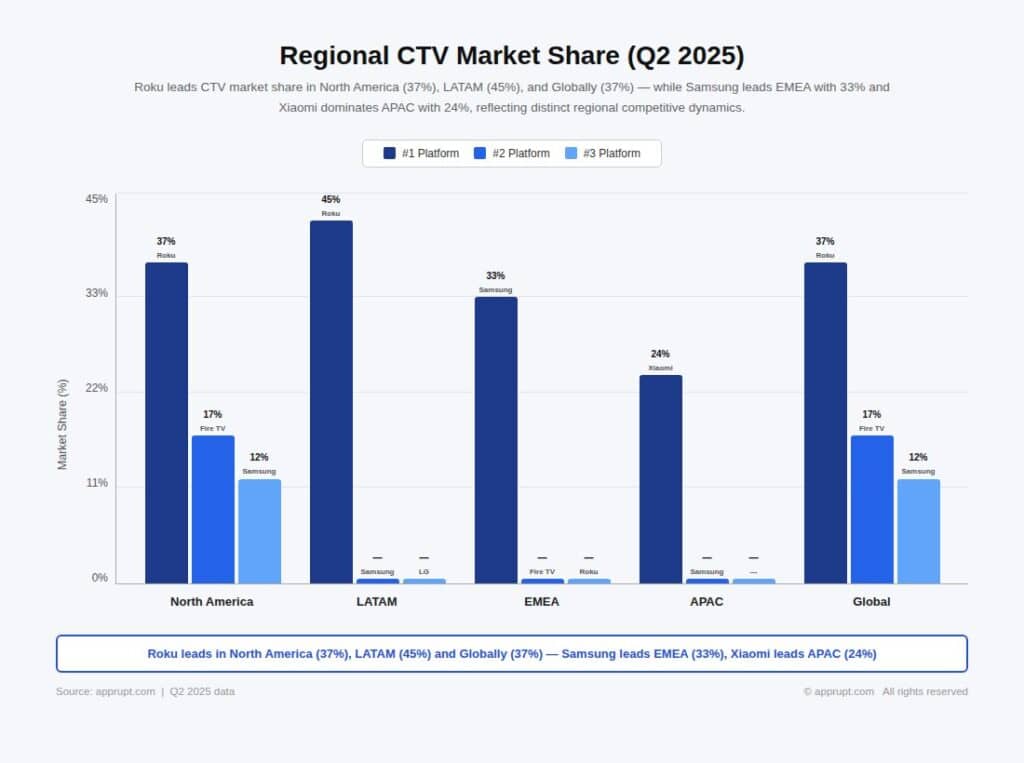

Regional CTV Market Share (Q2 2025)

| Region | #1 Platform | Share | #2 Platform | Share | #3 Platform | Share |

| North America | Roku | 37% | Amazon Fire TV | 17% | Samsung | 12% |

| LATAM | Roku | 45% | Samsung | — | LG | — |

| EMEA | Samsung | 33% | Amazon Fire TV | — | Roku | — |

| APAC | Xiaomi | 24% | Samsung | — | — | — |

| Global | Roku | 37% | Amazon Fire TV | 17% | Samsung | 12% |

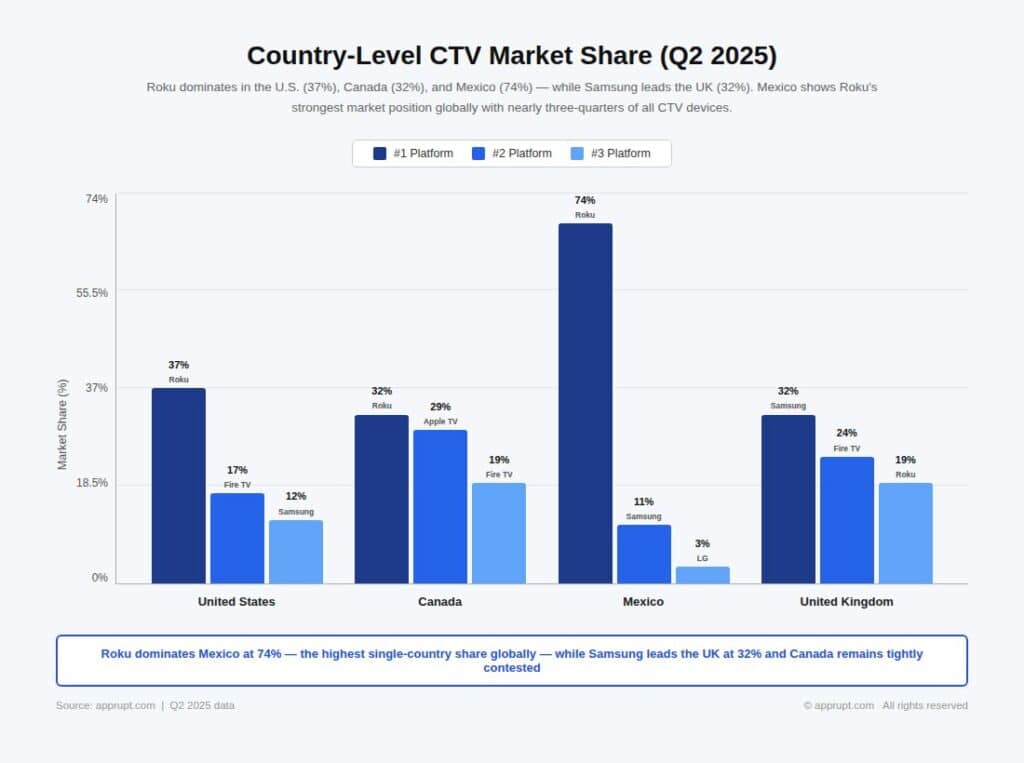

Country-Level CTV Market Share (Q2 2025)

| Country | #1 | Share | #2 | Share | #3 | Share |

| United States | Roku | 37% | Amazon Fire TV | 17% | Samsung | 12% |

| Canada | Roku | 32% | Apple TV | 29% | Amazon Fire TV | 19% |

| Mexico | Roku | 74% | Samsung | 11% | LG | 3% |

| United Kingdom | Samsung | 32% | Amazon Fire TV | 24% | Roku | 19% |

Roku’s most dominant single-country market is Mexico, where it commands an extraordinary 74% CTV device market share. In North America as a whole, Roku’s share stabilized at 36–37% throughout Q2–Q3 2025 after declining from 44% in Q1 2024.

Smart TV OS Unit Shipments

While Pixalate measures programmatic ad impressions, Omdia’s TV Design & Features Tracker measures actual TV unit shipments — a complementary view of market share.

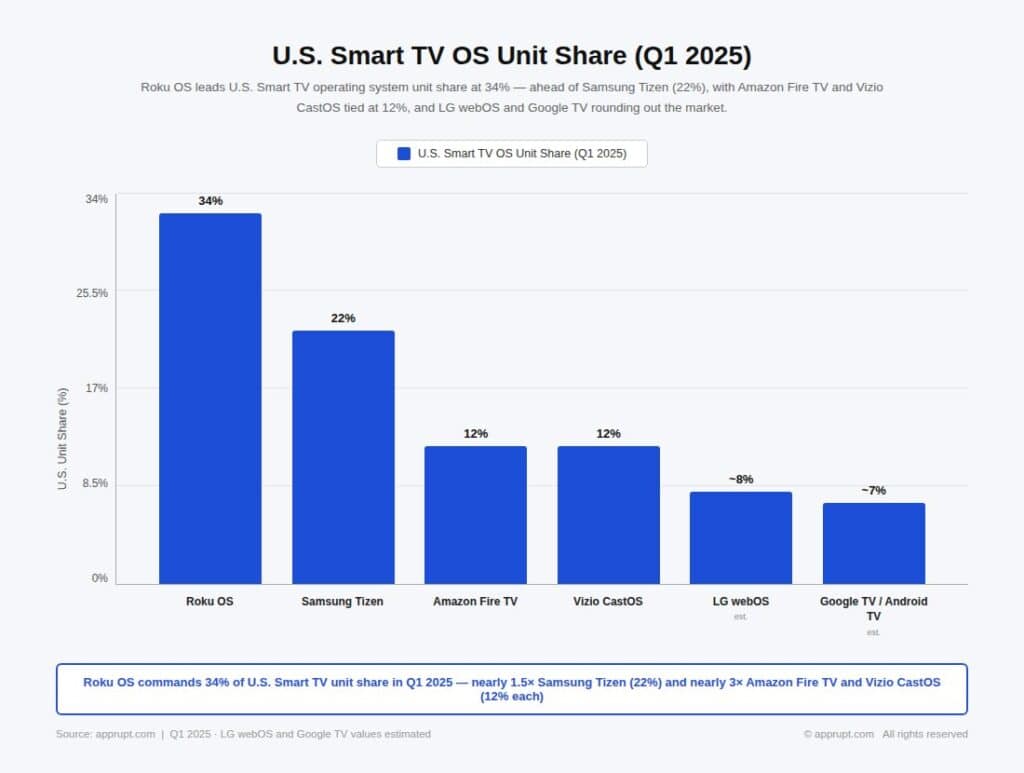

U.S. Smart TV OS Unit Share (Q1 2025)

| TV Operating System | U.S. Unit Share (Q1 2025) |

| Roku OS | 34% |

| Samsung Tizen | 22% |

| Amazon Fire TV | 12% |

| Vizio CastOS | 12% |

| LG webOS | ~8% (est.) |

| Google TV / Android TV | ~7% (est.) |

Roku has held the leading TV OS unit market share in the U.S. for most of the last six years, according to Omdia. Its Q1 2025 share of 34% means Roku sells more smart TV units than the next two TV operating systems (Samsung Tizen at 22% and Amazon Fire TV / Vizio CastOS at 12% each) combined. This claim was reiterated by Roku itself: “In the U.S., Roku TV unit sales are greater than the next two TV operating systems combined”.

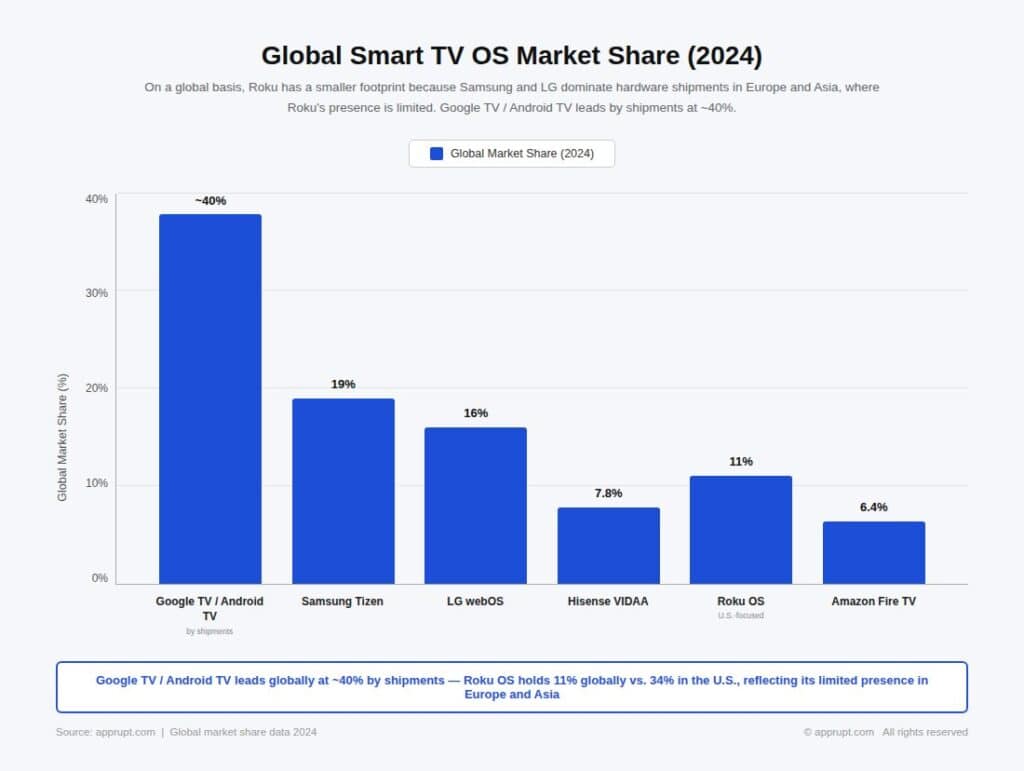

Global Smart TV OS Market Share (2024)

On a global basis, Roku has a smaller footprint because Samsung and LG dominate hardware shipments in Europe and Asia, where Roku’s presence is limited.

| TV Operating System | Global Market Share (2024) |

| Samsung Tizen | 19% |

| LG webOS | 16% |

| Roku OS | 11% |

| Google TV / Android TV | ~40% (by shipments) |

| Amazon Fire TV | 6.4% |

| Hisense VIDAA | 7.8% |

Samsung Tizen leads globally with an estimated 12.9% market share by installed base (120 million smart TV sets), followed by Hisense VIDAA at 7.8%, LG webOS at 7.4%, Roku at 6.4%, and Amazon Fire TV at 6.4%, according to the Connected TV Marketing Association. By shipment volume, Google TV / Android TV commands the largest share at approximately 40% of global smart TV shipments, though it is fragmented across hundreds of OEM brands.

Share of Total TV Viewing

Nielsen’s “The Gauge” provides a broader perspective: the share of all U.S. TV viewing time (streaming + cable + broadcast) attributed to Roku-powered devices.

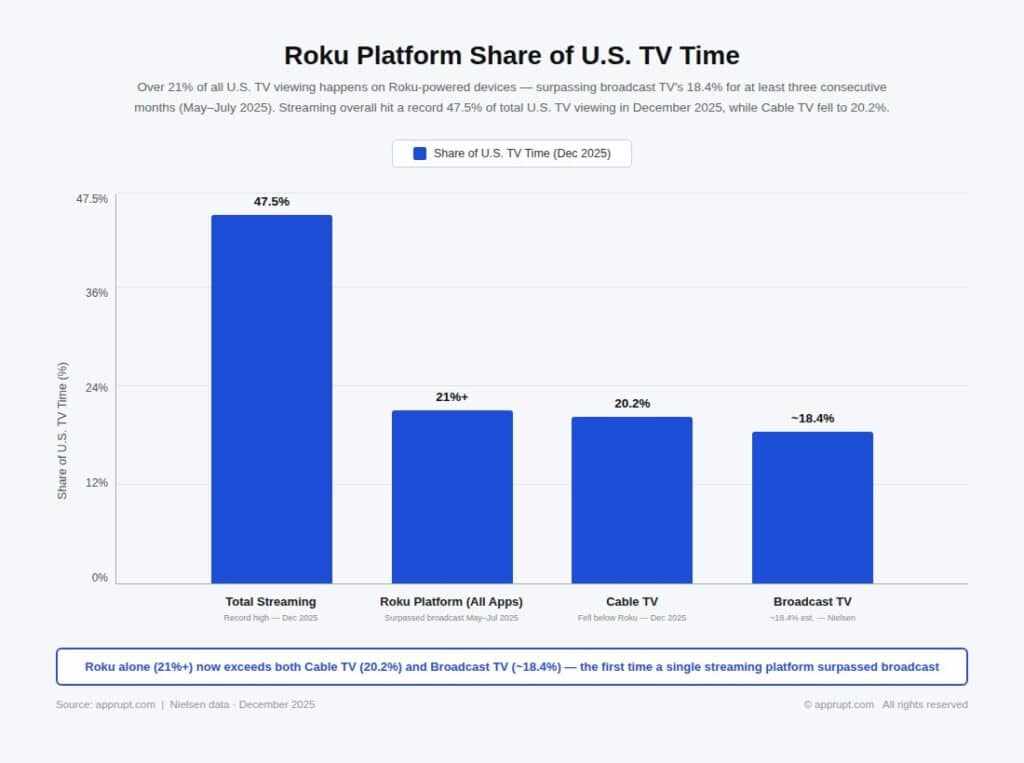

Roku Platform Share of U.S. TV Time

- Over 21% of all TV viewing in the U.S. happens on Roku-powered devices, according to Nielsen.

- This exceeded broadcast TV’s 18.4% share for at least three consecutive months (May–July 2025), marking the first time a single streaming platform surpassed broadcast.

- Streaming overall hit a record 47.5% of total U.S. TV viewing in December 2025.

- Cable TV’s share fell to 20.2% in December 2025.

| Viewing Category | Share of U.S. TV Time (Dec 2025) |

| Total streaming | 47.5% |

| Roku platform (all apps) | 21%+ |

| Cable TV | 20.2% |

| Broadcast TV | ~18.4% |

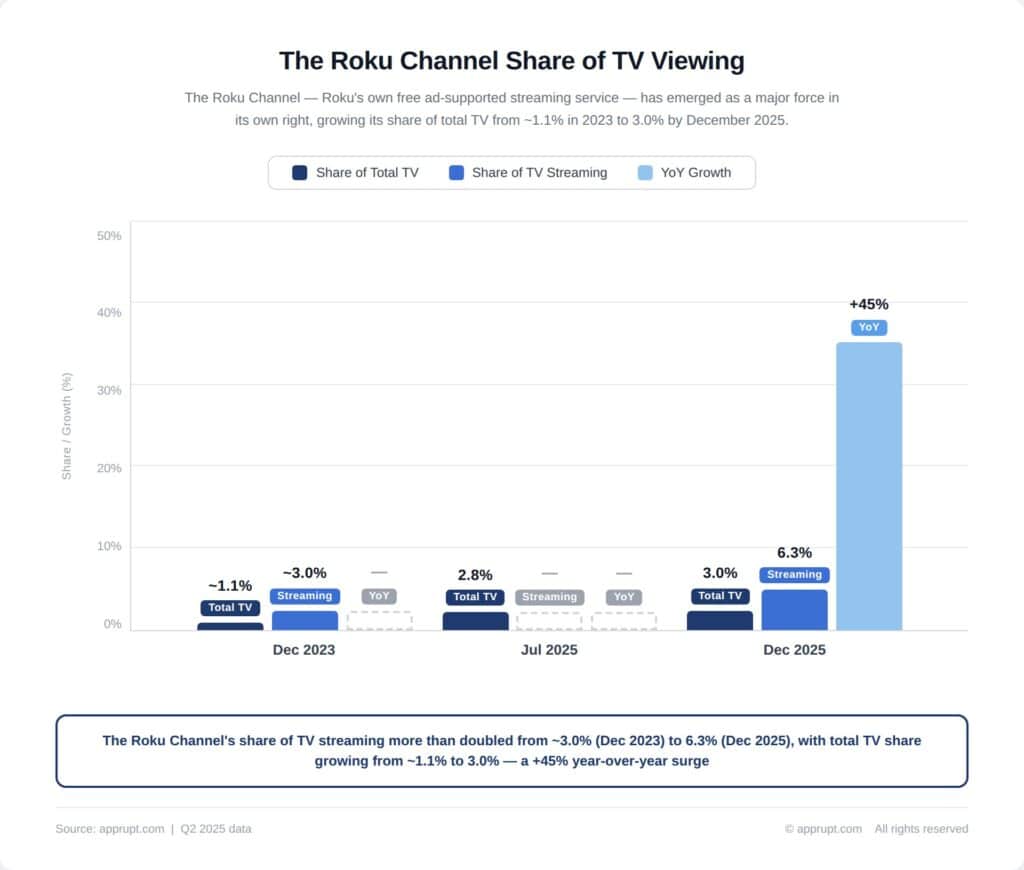

The Roku Channel Share of TV Viewing

The Roku Channel — Roku’s own free ad-supported streaming service — has emerged as a major force in its own right.

| Period | Roku Channel Share of Total TV | Roku Channel Share of TV Streaming | YoY Growth |

| Dec 2023 | ~1.1% | ~3.0% | — |

| Jul 2025 | 2.8% | — | — |

| Dec 2025 | 3.0% | 6.3% | +45% |

The Roku Channel’s 3% share of all U.S. TV viewership in December 2025 makes it larger than Paramount+ and Pluto TV combined (2.5%), Tubi (2%), Peacock (1.7%), and WBD’s HBO Max/Discovery+ (1.4%). Only Netflix (9%), YouTube (12.7%), Disney family (4.7%), and Prime Video (4.3%) have larger shares. The Roku Channel is the fastest-growing streaming service on Nielsen’s Gauge, with its share of TV time up 190% compared to two years prior.

The Roku Channel is also the #2 ad-supported streaming app by share of ad-supported TV time in the U.S. (behind YouTube), according to Nielsen Streaming Ratings from October 2025.

U.S. Household Penetration

- Roku devices are in over 50% of all U.S. broadband households.

- Among U.S. households that stream monthly, 59% report using Roku versus 49% for Samsung Tizen, according to Hub Entertainment Research.

- Roku’s active account base is larger than the subscribers of the six largest traditional pay-TV providers combined.

- Among “most-used TV sets,” Roku brand usage doubled to 8% in 2025, and Fire TV increased to 5%, according to Hub Research.

- Approximately 1 in 3 smart TVs sold in the U.S. is a Roku TV.

CTV Advertising Market Share

Roku’s market share extends beyond device share into the advertising ecosystem, where its scale makes it the largest authenticated CTV advertising platform.

- Roku accounts for an estimated 15–20% of all CTV ad impressions served in the U.S..

- The Roku-Amazon Ads exclusive partnership (June 2025) creates the largest authenticated CTV advertising footprint, reaching 80%+ of U.S. CTV households.

- Roku is projected to generate $5 billion in CTV advertising revenue by 2029, according to Omdia research.

- Total U.S. CTV ad spending was projected to reach $33.48 billion in 2025, growing 16.8% YoY.

- Roku’s video advertising grew faster than the broader U.S. OTT and digital ad markets in 2025, per Standard Media Index data.

OEM TV Partnerships

Roku’s smart TV market share is built on a broad network of TV manufacturer (OEM) partnerships and its own Roku-branded TVs.

Key Partnership Statistics

- Roku works with 45 TV OEM brands across 17 countries.

- Key long-term partners include TCL and Hisense, which have made Roku-powered TVs for nearly a decade.

- Roku partnered with Vestel (one of Europe’s top 3 TV manufacturers) in September 2025 for Roku-powered smart TVs in the UK and Europe.

- New brand partnerships in 2025: Hyundai (Mexico, Colombia, Peru), Noblex (Argentina), Finlandek (Colombia), Vitado (UK), and Finlux (UK, 15th brand in that market).

- Roku-made TVs (Select, Plus, Pro Series, Hiro) are sold at Best Buy, Target, Amazon, and other retailers.

Competitive Threats from Walmart/Vizio

A notable shift occurred in late 2025 when Walmart acquired Vizio and began converting its doorbuster Onn-branded TVs from Roku OS to Vizio OS. The 2025 holiday season was the first in which Walmart’s flagship doorbuster smart TV was powered by Vizio OS rather than Roku, and the first holiday without an exclusive low-cost Roku streaming player at Walmart. In response, Roku is:

- Diversifying retail partnerships with Best Buy and Target.

- Launching Hiro™, a new affordable Roku-branded TV sold exclusively at Target.

- Expanding Roku-made TVs to Canada (Best Buy exclusive).

- Moving TV production to Mexico to optimize costs.

However, some TCL and Hisense models have also shifted to Android TV for lower-cost, small-screen smart TVs, reducing Roku’s share among budget-tier TVs.

Historical CTV Market Share Trend

Roku’s CTV market share has gradually declined from its peak as the market has fragmented, though it maintains a substantial lead.

| Period | Roku U.S. CTV SOV | Trend |

| 2023 (avg) | ~55% | Peak |

| Q3 2024 | 37% | -29% YoY |

| Q4 2024 | 39% | Stabilized |

| Q1 2025 | 38% | Stable |

| Q2 2025 | 37% | Stable |

| Q3 2025 | 36% | Slight decline |

The decline from ~55% to ~37% reflects a normalizing market where competitors — particularly Samsung (with aggressive marketing and Tizen OS), Amazon (with Fire TV’s expanded lineup), and Apple (with growing Apple TV+ adoption) — are gaining traction. Importantly, Roku’s absolute reach has continued growing (90M+ households), even as its relative share decreases in a rapidly expanding market.

Global Smart TV Market Size

The overall smart TV market provides context for Roku’s growth opportunity.

- The global smart TV market was valued at $468.23 billion in 2025 and is projected to reach $985.06 billion by 2032, growing at a CAGR of 11%.

- The smart TV platforms market is estimated at $494.9 million (software/licensing) in 2026, projected to reach $1.17 billion by 2035 at a 10.04% CAGR.

- The Roku smart TV segment alone was valued at $48.08 billion in 2025 and is estimated to grow at a 14.4% CAGR through 2033.

- Global smart TV penetration surpassed 900 million units in 2024, with over 120 million new smart TVs shipped annually.

- More than 85% of households in developed countries own at least one smart TV.

- U.S. homes now own an average of two smart TVs.

2026 Outlook

Factors Supporting Roku’s Market Share

- Path to 100M streaming households: CEO Anthony Wood confirmed Roku is on track to surpass 100 million in 2026.

- FIFA World Cup 2026: Hosted in the U.S., Mexico, and Canada — Roku’s three strongest markets — this event should drive device sales and engagement.

- New retail and OEM partnerships: Best Buy, Target, Vestel (Europe), and new LATAM brands expand distribution.

- Premium subscription bundles: Planned for 2026 launch, bundles increase stickiness and reduce churn.

Competitive Pressures

- Walmart/Vizio integration: Loss of Walmart’s doorbuster TV slot reduces Roku’s exposure at the largest U.S. TV retailer.

- Samsung and Amazon gaining share: Both are investing heavily in smart TV OS expansion and advertising platforms.

- TCL and Hisense diversifying: Some models shifting from Roku OS to Android TV, particularly at lower price points.

- Google TV/Android TV’s global dominance: At ~40% of global shipments, Android TV remains the largest platform worldwide.

Despite these headwinds, Roku’s entrenched position in the U.S. (34% of TV OS unit shipments, 21%+ of all TV viewing, 50%+ broadband household penetration) gives it a substantial moat that competitors have been unable to replicate.