YouTube TV has emerged as the fastest-growing pay TV distributor in the United States, positioning itself to become the nation’s largest pay TV provider within the next one to two years. As of late 2025, YouTube TV has approximately 9.3–10 million subscribers, up from just 1 million in 2019 — a ten-fold increase in six years. Two leading research firms — Moffett, Nathanson and Omdia — both forecast that YouTube TV will surpass Charter Communications and Comcast to become the #1 U.S. pay TV operator by 2026–2027. With YouTube’s total revenue surpassing $60 billion in 2025 and YouTube TV generating an estimated $8–10 billion in annual revenue, the vMVPD has achieved profitability and is entering a new phase of expansion through genre-specific subscription plans launching in 2026.

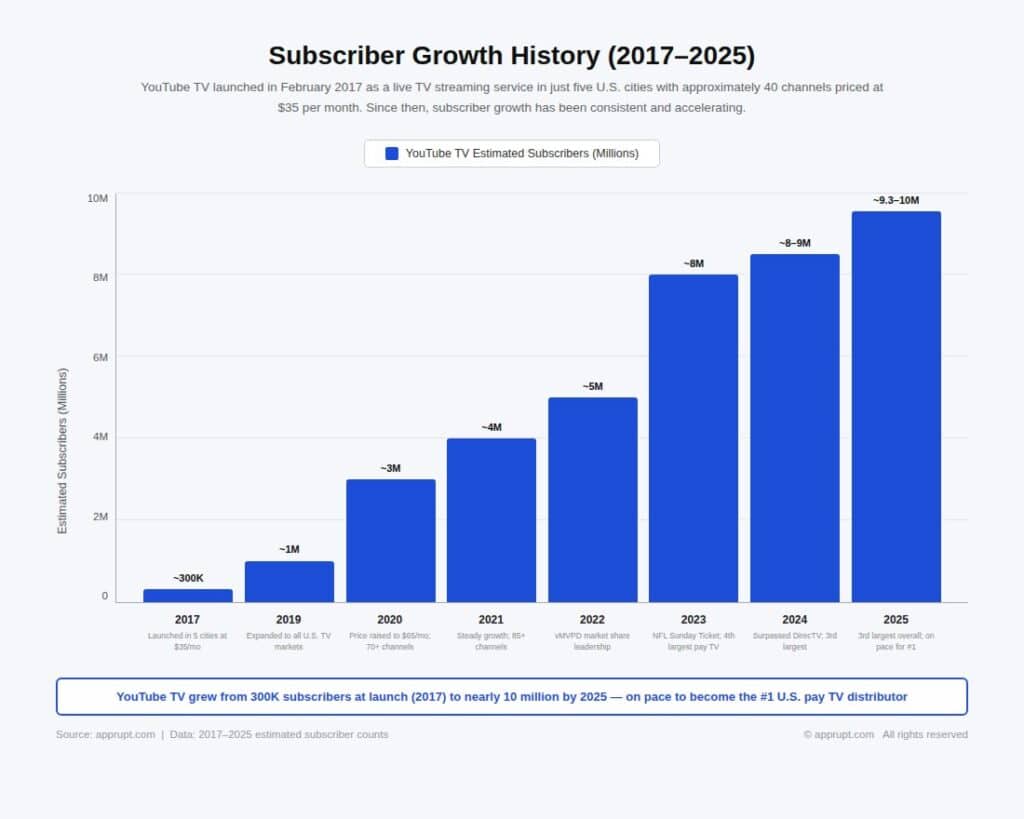

Subscriber Growth History (2017–2025)

YouTube TV launched in February 2017 as a live TV streaming service in just five U.S. cities with approximately 40 channels priced at $35 per month. Since then, subscriber growth has been consistent and accelerating.

| Year | Estimated Subscribers | Key Milestones |

| 2017 | ~300K (launch year) | Launched in 5 cities at $35/mo |

| 2019 | ~1 million | Expanded to all U.S. TV markets |

| 2020 | ~3 million | Price raised to $65/mo; 70+ channels |

| 2021 | ~4 million | Steady growth; 85+ channels |

| 2022 | ~5 million | vMVPD market share leadership established |

| 2023 | ~8 million | NFL Sunday Ticket acquired; 4th largest pay TV distributor |

| 2024 | ~8–9 million | Surpassed DirecTV; 3rd largest distributor |

| 2025 | ~9.3–10 million | 3rd largest overall; on pace for #1 |

YouTube TV achieved a 35% year-over-year subscriber growth rate in 2023, adding approximately 3 million subscribers since mid-2022. Google confirmed YouTube TV was its “fastest-growing product” in 2023. By April 2025, the platform had 9.4 million subscribers, and by November 2025, multiple sources reported the 10 million subscriber milestone had been reached or nearly reached.

Current Market Position (End of 2025)

As of the end of 2025, YouTube TV is the third-largest pay TV distributor in the United States, trailing only Charter Communications and Comcast.

| Rank | Pay TV Distributor | Subscribers (End 2025) | Trend |

| 1 | Charter (Spectrum) | 11.4 million | Declining ~255K/year |

| 2 | Comcast (Xfinity) | 10.6 million | Declining ~1.25M/year |

| 3 | YouTube TV | 9.3 million | Growing ~1.5M/year |

Source: Omdia (December 2025)

YouTube TV commands over 40% of the total virtual MVPD (vMVPD) market, which collectively has approximately 18.2 million subscribers. Its closest vMVPD competitor, Hulu + Live TV, holds 27% of the market, followed by Sling TV at 12% and FuboTV at 9%.

YouTube TV vs. Traditional Cable: The Crossover

The subscriber trajectories of YouTube TV and traditional cable operators are on a collision course. In 2023 alone, 3.8 million subscribers canceled traditional cable services from operators like Comcast, Charter, Altice USA, and Dish — a record year for cancellations. DirecTV lost an estimated 1.8 million satellite subscribers that same year. Meanwhile, YouTube TV has been adding approximately 1.5 million subscribers per year.

MoffettNathanson estimates that 26.5% of consumers who cancel traditional MVPD subscriptions eventually sign up for a virtual MVPD service. This “cable-to-vMVPD migration” pipeline is YouTube TV’s primary growth engine.

Forecasts: 2026 and 2027

Two major research firms have issued projections for YouTube TV’s subscriber trajectory. While both predict YouTube TV will become #1, they differ slightly on timing.

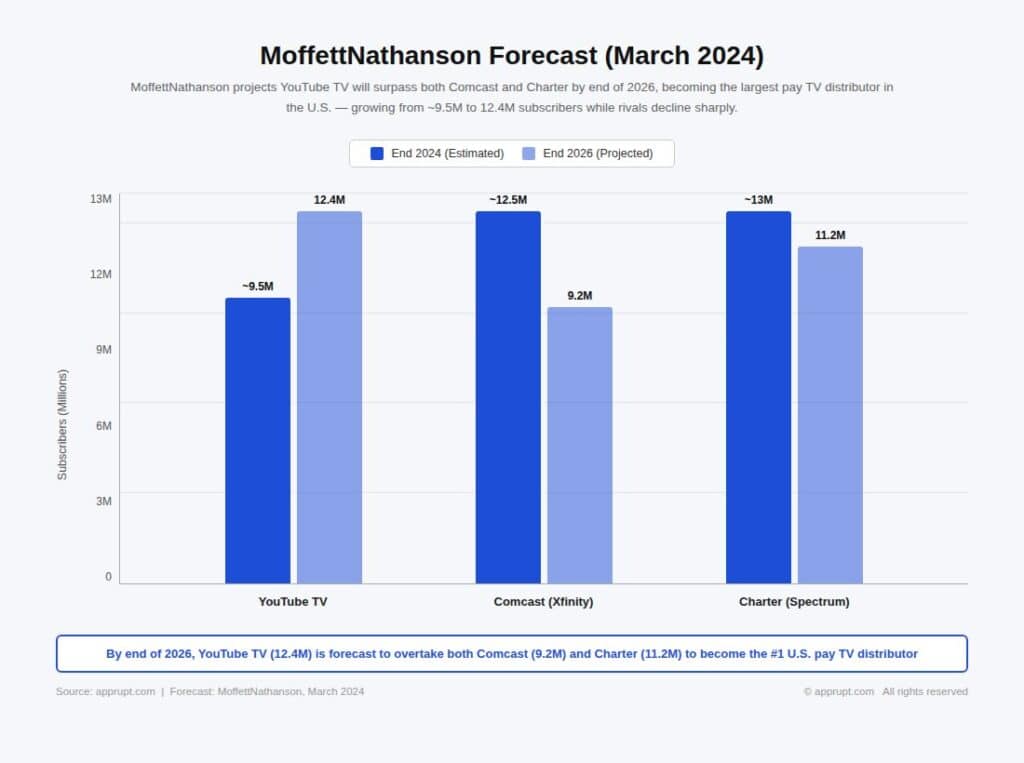

MoffettNathanson Forecast (March 2024)

| Year | YouTube TV | Comcast | Charter |

| End 2024 | ~9.5M | ~12.5M | ~13M |

| End 2026 | 12.4M | 9.2M | 11.2M |

Source: MoffettNathanson

MoffettNathanson projected YouTube TV would reach 12.4 million subscribers by the end of 2026, adding roughly 1.5 million per year. At that point, it would surpass both Comcast (projected at 9.2 million) and Charter (11.2 million) as the largest pay TV operator.

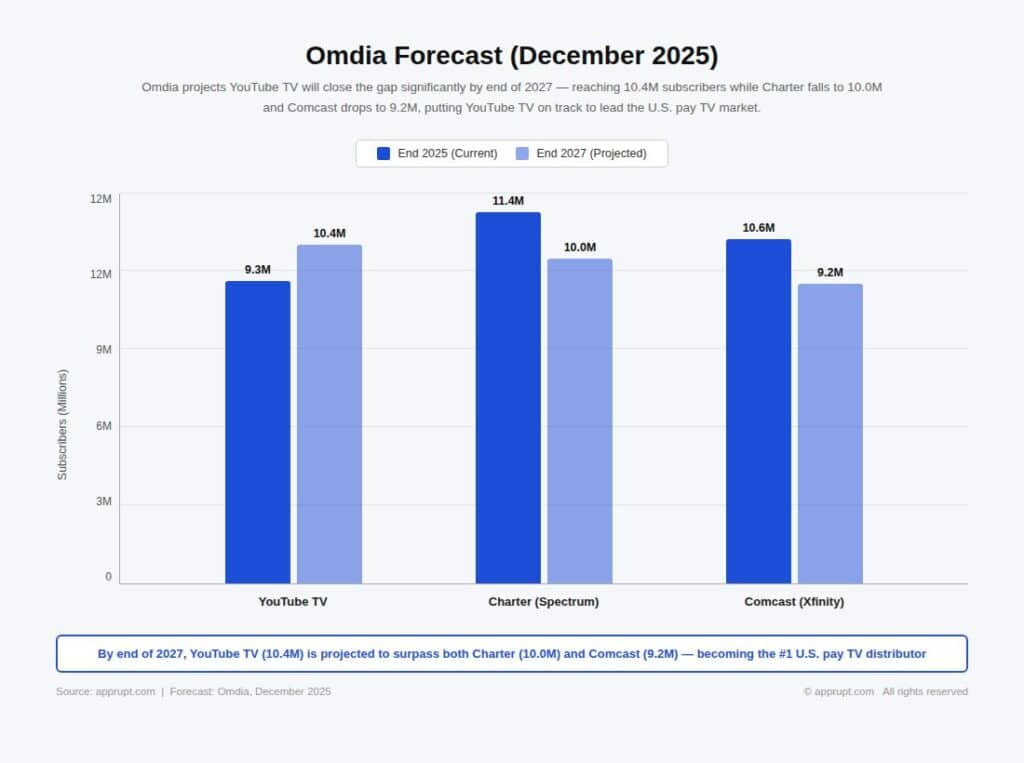

Omdia Forecast (December 2025)

| Year | YouTube TV | Charter | Comcast |

| End 2025 | 9.3M | 11.4M | 10.6M |

| End 2027 | 10.4M | 10.0M | 9.2M |

Source: Omdia

Omdia’s more conservative forecast, issued in December 2025, projects YouTube TV will reach 10.4 million subscribers by 2027 — enough to overtake both Charter and Comcast for the first time. “For the first time in U.S. television history, the largest pay-TV operator will be a virtual provider,” said Maria Rua Aguete, head of media and entertainment at Omdia.

The difference between the two forecasts likely reflects the impact of YouTube TV’s December 2024 price hike (from $73 to $83/month), which may moderate subscriber growth relative to earlier projections.

Revenue and Profitability

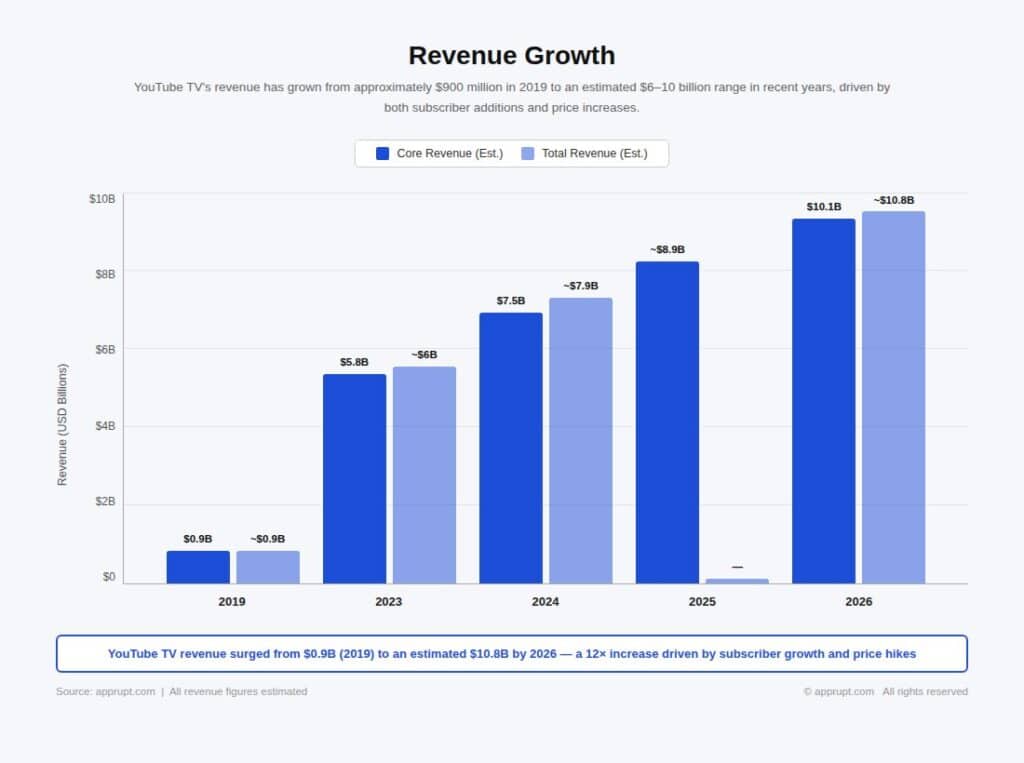

Revenue Growth

YouTube TV’s revenue has grown from approximately $900 million in 2019 to an estimated $6–10 billion range in recent years, driven by both subscriber additions and price increases.

| Year | Core Revenue (Est.) | Total Revenue (Est.) |

| 2019 | $900 million | ~$900 million |

| 2023 | $5.8 billion | ~$6 billion |

| 2024 | $7.5 billion (core) | ~$7.9 billion (incl. Sunday Ticket) |

| 2025 | ~$8.9 billion (Q1 alone = ~$8.93B total YouTube) | — |

| 2026 | $10.1 billion (core) | ~$10.8 billion |

Between 2023 and 2026, YouTube TV’s core revenue is expected to nearly double, reaching over $10 billion. MoffettNathanson projected total revenue (including NFL Sunday Ticket) would approach $11 billion annually by 2026.

Path to Profitability

YouTube TV turned profitable in 2024 after years of operating losses. MoffettNathanson estimated the platform posted $200 million in operating income in 2024, following a $300 million loss in 2023. Operating income is projected to reach $600 million by 2026.

The vMVPD’s cost structure is driven primarily by programming fees paid to content providers. These costs were estimated at $6.3 billion in 2024, rising to $8.6 billion by 2026. YouTube TV’s lower customer acquisition costs — leveraging Google’s existing ad technology and platform rather than expensive truck rolls and hardware — give it a structural margin advantage over traditional cable operators.

YouTube’s Overall Revenue Context

YouTube (including YouTube TV, YouTube Premium, and advertising) generated over $60 billion in total revenue for 2025, exceeding Netflix’s $45.2 billion for the same year. Alphabet CEO Sundar Pichai disclosed that the company has over 325 million paid subscriptions across consumer services, including YouTube Premium, YouTube TV, and Google One.

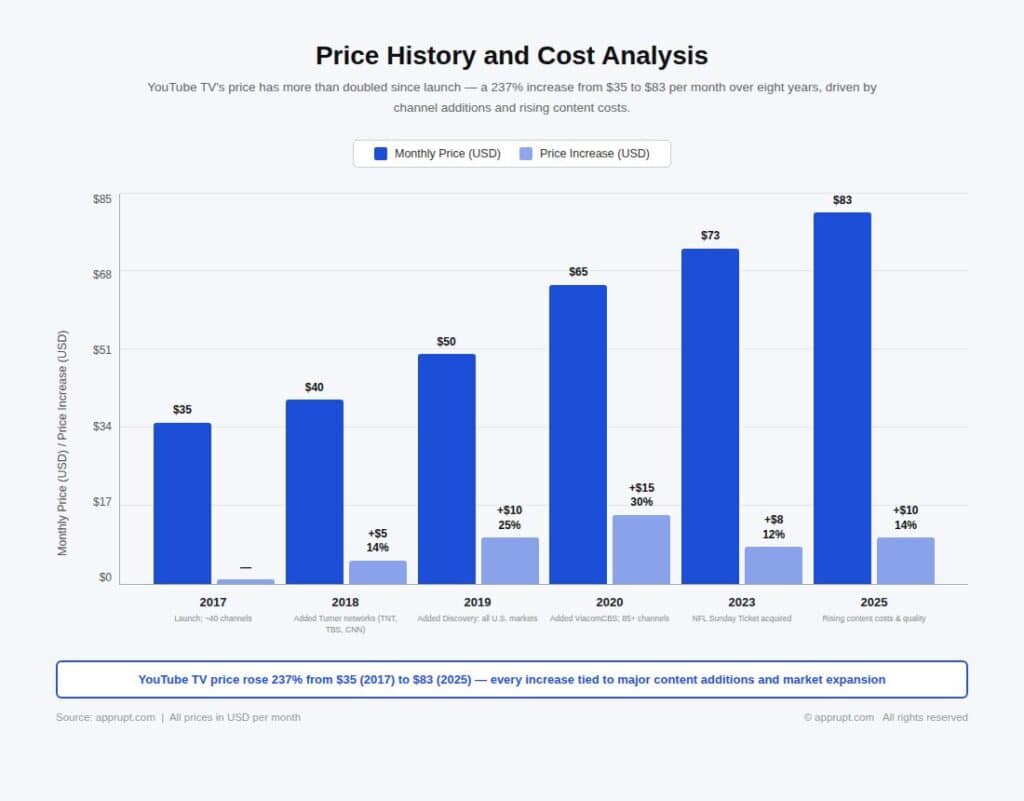

Price History and Cost Analysis

YouTube TV’s price has more than doubled since launch — a 237% increase from $35 to $83 per month over eight years.

| Year | Monthly Price | Price Increase | Rationale |

| 2017 | $35 | — | Launch price; ~40 channels |

| 2018 | $40 | +$5 (14%) | Added Turner networks (TNT, TBS, CNN) |

| 2019 | $50 | +$10 (25%) | Added Discovery channels; expanded to all U.S. markets |

| 2020 | $65 | +$15 (30%) | Added ViacomCBS networks; expanded to 85+ channels |

| 2023 | $73 | +$8 (12%) | NFL Sunday Ticket acquired as exclusive add-on |

| 2025 | $83 | +$10 (14%) | “Rising cost of content and investments in quality” |

Despite the increases, YouTube TV’s $83/month base price remains competitive with traditional cable. The average cable-only package costs $78.58/month, but frequently comes bundled with internet and phone at higher total prices. MoffettNathanson noted that “with traditional MVPD packages now fetching prices in excess of $100, YouTube TV still presents a great value” — especially for younger consumers who value its mobile viewing, no-contract flexibility, and no hardware requirements.

However, the real cost for many households runs higher. Including add-ons and regional sports fees, typical YouTube TV monthly bills range from $88 to $105.

NFL Sunday Ticket: Growth Catalyst

The acquisition of NFL Sunday Ticket in 2023 has been a pivotal growth driver for YouTube TV. The out-of-market NFL package — previously exclusive to DirecTV for decades — was acquired by YouTube in a deal valued at over $2 billion per year.

According to Antenna data, approximately 1.3 million subscribers purchased Sunday Ticket in its first year on YouTube, slightly above the 1.2 million under DirecTV. Critically, 41% of Sunday Ticket customers who purchased the add-on also became new YouTube TV subscribers. For the 2025–26 NFL season, Alphabet CEO Sundar Pichai noted that the NFL achieved its “highest-ever paid subscriber count” for the Sunday Ticket package, though no specific number was disclosed.

Current Sunday Ticket pricing for the 2025 season:

- With YouTube TV: $192/year or $16/month for 12 months (new subscribers)

- Standalone (YouTube Primetime Channels): $240/year or $20/month for 12 months

- Returning subscribers with YouTube TV: $378/year or $31.50/month

NFL Sunday Ticket’s role extends beyond direct subscriber acquisition — it reinforces YouTube TV’s brand positioning as the definitive live sports destination, which is the strongest remaining driver of pay TV subscriptions broadly.

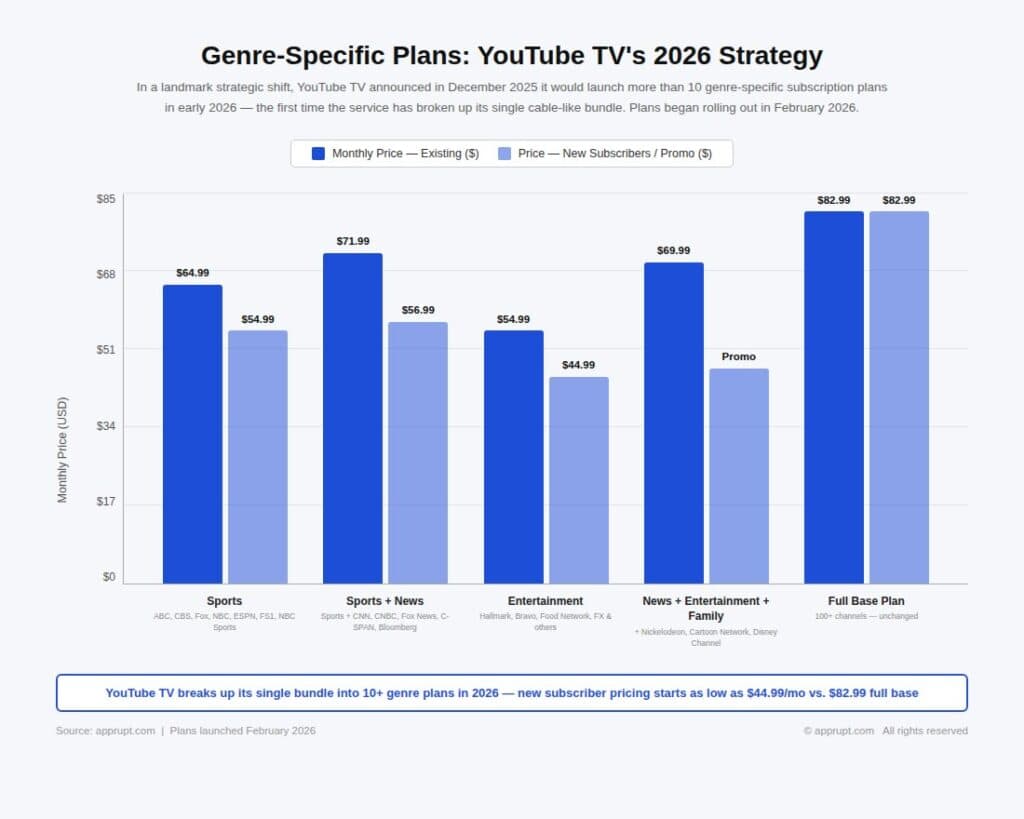

Genre-Specific Plans: YouTube TV’s 2026 Strategy

In a landmark strategic shift, YouTube TV announced in December 2025 that it would launch more than 10 genre-specific subscription plans in early 2026 — the first time the service has broken up its single cable-like bundle.

The new plans began rolling out in February 2026 with the following initial offerings:

| Plan | Monthly Price (Existing) | Price (New Subscribers) | Key Channels |

| Sports | $64.99 | $54.99 (1st year) | ABC, CBS, Fox, NBC, ESPN networks, FS1, NBC Sports |

| Sports + News | $71.99 | $56.99 (1st 3 months) | Sports channels + CNN, CNBC, Fox News, C-SPAN, Bloomberg |

| Entertainment | $54.99 | $44.99 (1st 3 months) | Hallmark, Bravo, Food Network, FX, and others |

| News + Entertainment + Family | $69.99 | Promotional pricing | Entertainment channels + Nickelodeon, Cartoon Network, Disney Channel |

| Full Base Plan | $82.99 | $82.99 | 100+ channels (unchanged) |

All plans include YouTube TV’s core features: unlimited DVR storage, multiview, key plays, fantasy view, up to six household accounts, and the option to add premium add-ons like NFL Sunday Ticket, RedZone, and HBO Max.

“TV should be easy, giving viewers greater control over what they want to watch,” said Christian Oestlien, YouTube VP and Head of Subscriptions. The genre-based approach directly mirrors moves by competitors: DirecTV launched “Genre Packs,” Fubo introduced a sports-focused package in 2025, and Sling TV has long offered à la carte-style bundles.

This strategy addresses two key challenges. First, it creates lower-cost entry points for price-sensitive consumers who may have been deterred by the $83 base price. Second, it gives existing subscribers a reason to stay (rather than churn) by allowing them to downgrade to a cheaper genre plan instead of canceling entirely.

The Disney-ESPN Dispute: A Stress Test

In late October 2025, YouTube TV faced its most significant carriage dispute when negotiations with Disney broke down, resulting in a nearly two-week blackout of more than 20 Disney-owned channels — including ESPN, ABC, FX, National Geographic, and Disney Channel.

The dispute centered on ESPN’s carriage fees, which exceed $10 per subscriber per month — more than any other network in the U.S.. Google claimed Disney was demanding “an unprecedented increase in fees,” while Disney argued Google was “refusing to pay fair rates”. The blackout meant YouTube TV’s approximately 10 million customers missed two Monday Night Football broadcasts and multiple college football games during peak football season.

The companies reached a new multi-year distribution deal on November 14, 2025. YouTube TV offered affected subscribers a $20 credit. The dispute highlighted both the platform’s growing leverage — Disney ultimately needed YouTube TV’s 10 million subscriber base — and its vulnerability to content cost inflation, which remains the primary margin pressure for vMVPDs.

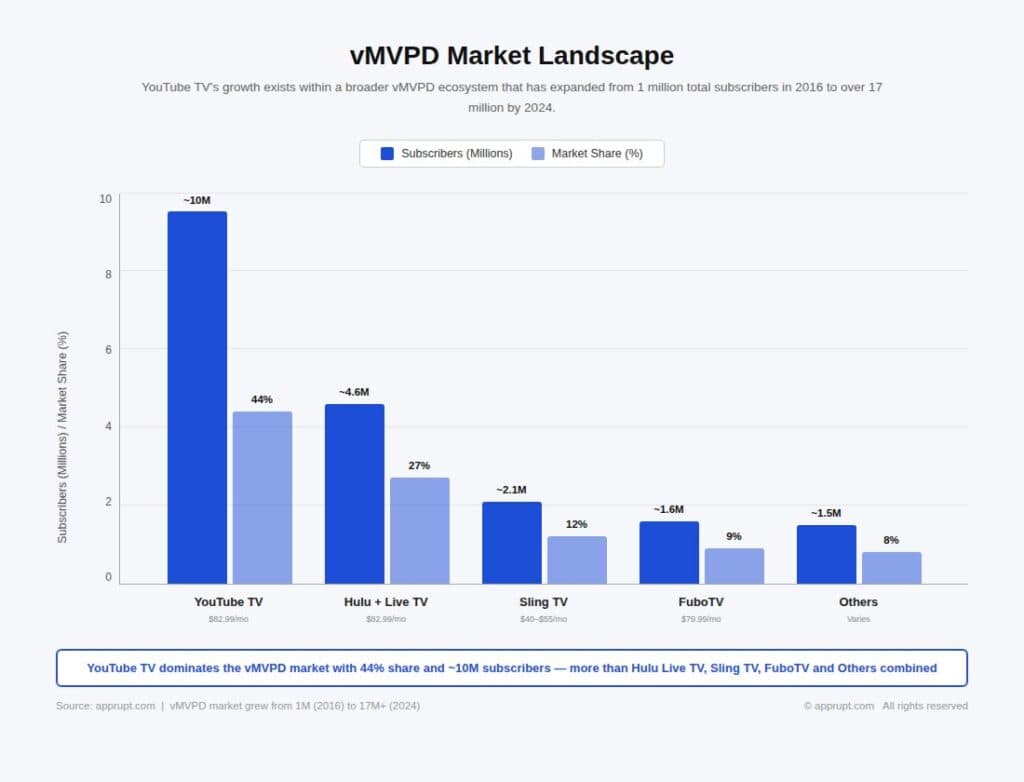

vMVPD Market Landscape

YouTube TV’s growth exists within a broader vMVPD ecosystem that has expanded from 1 million total subscribers in 2016 to over 17 million by 2024.

| vMVPD Service | Subscribers | Market Share | Monthly Price |

| YouTube TV | ~10 million | 44% | $82.99 |

| Hulu + Live TV | ~4.6 million | 27% | $82.99 |

| Sling TV | ~2.1 million | 12% | $40–$55 |

| FuboTV | ~1.6 million | 9% | $79.99 |

| Others | ~1.5 million | 8% | Varies |

YouTube TV and Hulu + Live TV together account for three-quarters of all U.S. vMVPD subscription revenues. However, YouTube TV’s viewer growth CAGR of 28.0% between 2019 and 2024 significantly outpaced the overall vMVPD category’s 11.6% growth rate during the same period.

The streaming share of total pay TV subscribers has risen sharply: from 8% in 2018 to 23% in 2023. Total traditional pay TV (excluding vMVPDs) subscribers declined 12% year-over-year in 2023 to 54.96 million, while vMVPD-inclusive pay TV declined a more moderate 6% to 71.2 million.

Competitive Advantages and Risks

Advantages

- Google ecosystem integration: YouTube TV benefits from Google’s advertising technology, search distribution, and an existing platform with nearly 3 billion global users. Customer acquisition costs are significantly lower than cable operators who must install hardware.

- Sports dominance: NFL Sunday Ticket exclusivity, plus comprehensive coverage across ESPN, Fox Sports, CBS Sports, and NBC Sports, makes YouTube TV the most sports-complete streaming option.

- Superior product features: Unlimited DVR, multiview (watch 4 games simultaneously), key plays highlights, and fantasy view integration are features cable operators have not matched.

- YouTube CTV momentum: YouTube is the most-watched streaming platform on connected TVs, surpassing Netflix. U.S. adults will spend more time watching YouTube than Netflix in 2026. This creates a natural funnel to YouTube TV.

- No contracts: Month-to-month flexibility with no equipment or installation requirements appeals to younger demographics.

Risks

- Rising content costs: ESPN alone costs over $10/subscriber/month. As YouTube TV scales, its programming cost base (estimated at $8.6 billion by 2026) grows faster than revenue from subscriber additions.

- Price ceiling: At $83/month, YouTube TV’s original value proposition as a cheaper cable alternative has eroded. The 237% price increase since 2017 risks subscriber fatigue.

- Carriage disputes: The 2025 Disney blackout demonstrated vulnerability to content owner negotiations. As YouTube TV becomes the largest distributor, it will face more aggressive pricing demands from networks.

- Genre unbundling risks: While genre plans create lower-price entry points, they also allow existing $83/month subscribers to downgrade, potentially reducing ARPU.

Future Outlook

YouTube TV’s trajectory points toward a fundamental restructuring of the U.S. pay TV market. The service is virtually certain to become the #1 pay TV distributor in the U.S. by 2027 at the latest, with a subscriber base of 10–12 million. The gap will widen as Charter and Comcast continue shedding approximately 5–7% of their video subscribers annually.

The introduction of genre-specific plans in 2026 represents YouTube TV’s next growth phase — expanding the addressable market beyond the ~10 million consumers willing to pay $83/month for a full bundle. With a sports-focused plan at $55–65/month and entertainment at $45–55/month, YouTube TV can target the price-sensitive segments of the 80+ million U.S. households that have already cut the cord.

Revenue is projected to surpass $10 billion by 2026, with operating income reaching $600 million. Longer-term, YouTube TV’s integration with YouTube’s broader ecosystem — 3 billion global users, $60+ billion in annual revenue, and dominant connected TV viewing share — gives it structural advantages that no traditional cable operator or competing vMVPD can replicate.