Netflix ended 2025 with a record 325 million paid subscribers globally, generating $45.2 billion in full-year revenue — a 16% year-over-year increase. The company surpassed the 300-million subscriber milestone in Q4 2024 and added approximately 23 million new members in 2025. However, this marks a notable deceleration from the 41 million subscribers added in 2024, raising questions about whether Netflix’s explosive growth phase has peaked. For 2026, Netflix has guided revenue between $50.7 billion and $51.7 billion, signaling continued growth at a 12%–14% clip, while increasing content spending to $20 billion.

Starting in 2025, Netflix stopped reporting quarterly subscriber numbers, stating that revenue is “a more meaningful measure of the health of its business”. The company indicated it will disclose subscriber milestones only when significant thresholds are reached.

Current Subscriber Base (2025–2026)

Global Total

Netflix confirmed 325 million paid memberships at the close of 2025, up from 301.6 million at the end of 2024. During the second half of 2025, Netflix users collectively streamed 96 billion hours, reflecting a 2% year-over-year increase, driven largely by original content which saw a 9% uptick. The company noted its global audience reach is now edging close to 1 billion when accounting for multiple viewers per household.

Ampere Analysis estimated Netflix had approximately 310 million subscribers by the end of Q1 2025, marking 3% quarter-on-quarter growth. Since Netflix no longer reports quarterly figures, third-party estimates are the primary source for intra-year tracking.

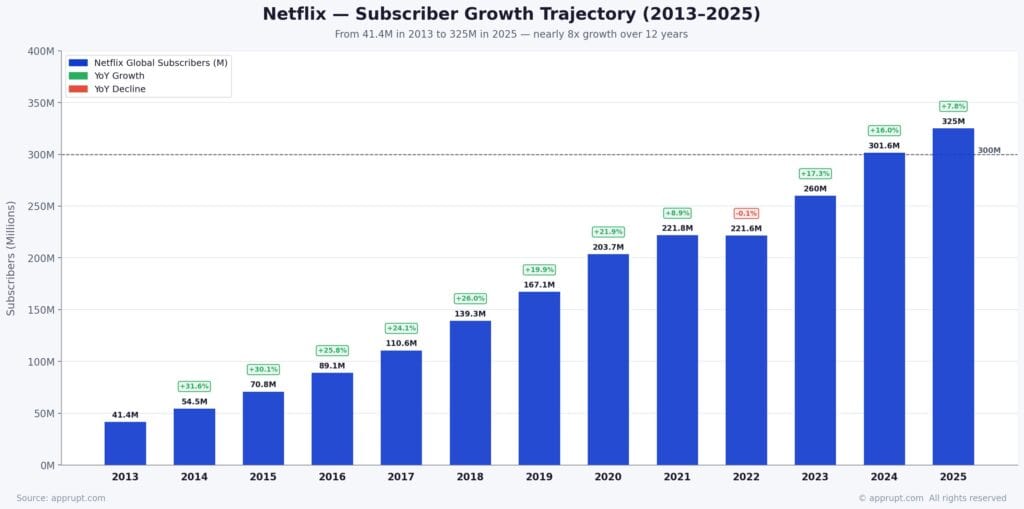

Subscriber Growth Trajectory (2013–2025)

| Year | Subscribers (Millions) |

| 2013 | 41.4 |

| 2014 | 54.5 |

| 2015 | 70.8 |

| 2016 | 89.1 |

| 2017 | 110.6 |

| 2018 | 139.3 |

| 2019 | 167.1 |

| 2020 | 203.7 |

| 2021 | 221.8 |

| 2022 | 221.6 |

| 2023 | 260.0 |

| 2024 | 301.6 |

| 2025 | 325.0 |

Source: Netflix earnings reports, Statista

The 2022 dip was a watershed moment — Netflix lost over 1 million subscribers in H1 2022, triggering a 35% stock plunge and prompting the launch of an ad-supported tier. The recovery since then has been remarkable, adding over 100 million subscribers in three years.

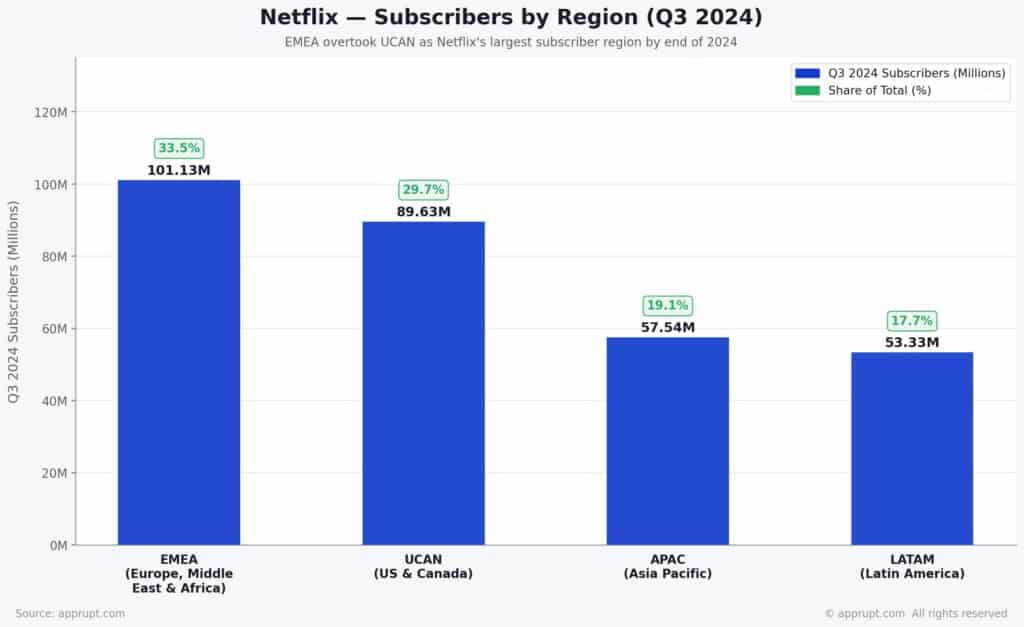

Regional Breakdown

Subscribers by Region

EMEA (Europe, Middle East, and Africa) overtook North America as Netflix’s largest subscriber region by the end of 2024. The last officially reported regional breakdown was for Q3 2024:

| Region | Q3 2024 Subscribers | Share of Total |

| EMEA (Europe, Middle East, Africa) | 101.13M | 33.5% |

| UCAN (US & Canada) | 89.63M | 29.7% |

| APAC (Asia Pacific) | 57.54M | 19.1% |

| LATAM (Latin America) | 53.33M | 17.7% |

Regional Growth Dynamics

EMEA has been the fastest-growing region in absolute terms, gaining approximately 25 million subscribers between 2022 and 2024. The region accounted for more than 101 million of Netflix’s total subscriber base by end-2024.

Asia-Pacific represents the highest percentage growth opportunity. APAC subscribers grew from 33.7 million in 2022 to 57.5 million in Q3 2024 — a 70% increase in under two years. Statista forecasts the region will reach approximately 70.1 million subscribers by 2029.

US & Canada remains the most lucrative market by ARPU but is approaching saturation. Penetration stands at 53% in the US and 48% in Canada. Growth has slowed significantly, with Ampere estimating just 1.15 million net adds in Q1 2025 compared to 4 million in Q4 2024.

Latin America has grown steadily from 39.6 million in 2022 to 53.3 million in Q3 2024, benefiting from localized content and pricing strategies.

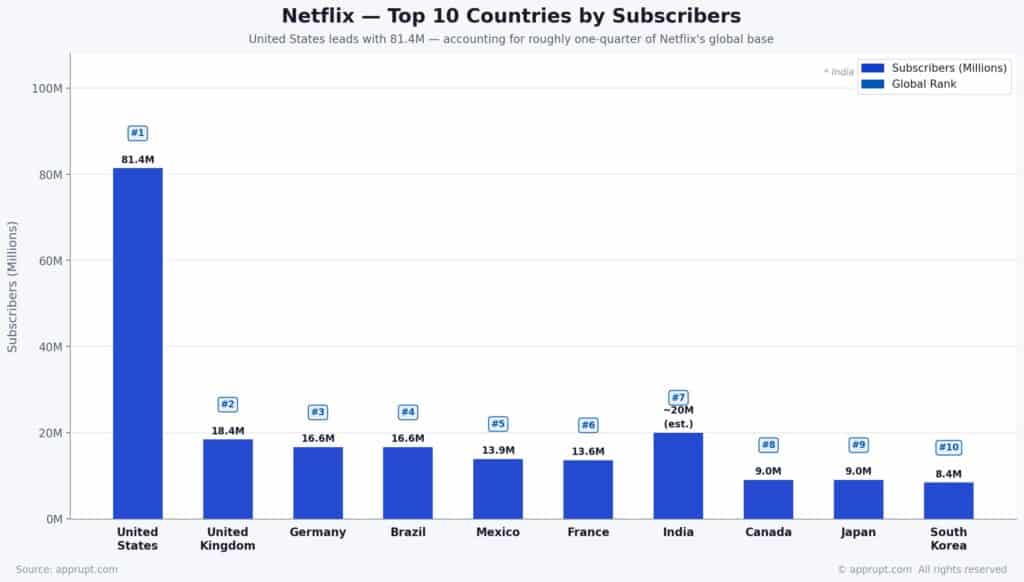

Top Countries by Subscribers

The United States accounts for roughly one-quarter of Netflix’s entire global subscriber base:

| Rank | Country | Subscribers |

| 1 | United States | 81.4M |

| 2 | United Kingdom | 18.4M |

| 3 | Germany | 16.6M |

| 4 | Brazil | 16.6M |

| 5 | Mexico | 13.9M |

| 6 | France | 13.6M |

| 7 | India | ~20M (est.) |

| 8 | Canada | 9.0M |

| 9 | Japan | 9.0M |

| 10 | South Korea | 8.4M |

Netflix in India

India has emerged as a pivotal growth market. It became Netflix’s second-largest market for new subscriber additions in Q4 2025. Industry estimates place Netflix India’s subscriber base at approximately 20–22 million users across direct-to-consumer and bundled plans. Netflix India’s revenue reached approximately $905 million in 2025 (about 2% of global revenue), with net profit surging 63% in FY25. Penetration remains below 1% of India’s population, indicating enormous headroom for growth. Netflix is investing $2 billion in Indian content and plans to release 25 new Indian titles.

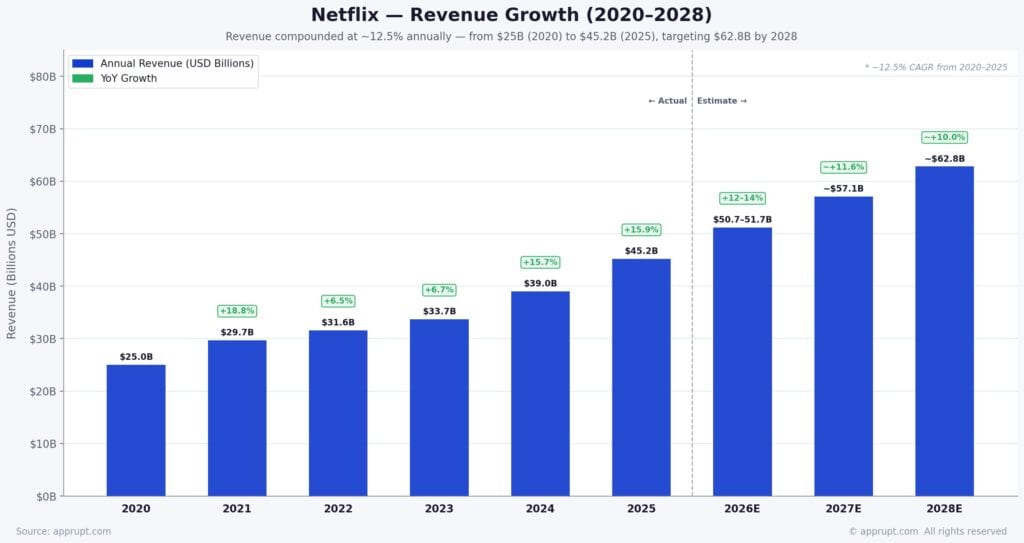

Revenue and Financial Performance

Revenue Growth

Netflix’s revenue has compounded at approximately 12.5% annually from $25 billion in 2020 to $45.2 billion in 2025.

| Year | Revenue | YoY Growth |

| 2020 | $25.0B | — |

| 2021 | $29.7B | 18.8% |

| 2022 | $31.6B | 6.5% |

| 2023 | $33.7B | 6.7% |

| 2024 | $39.0B | 15.7% |

| 2025 | $45.2B | 15.9% |

| 2026E | $50.7B–$51.7B | 12%–14% |

| 2027E | ~$57.1B | ~11.6% |

| 2028E | ~$62.8B | ~10.0% |

Source: Netflix earnings, MarketScreener consensus estimates

Netflix management has stated a long-term revenue target of $80 billion by 2030, equating to approximately 12.2% annual growth from 2025 levels.

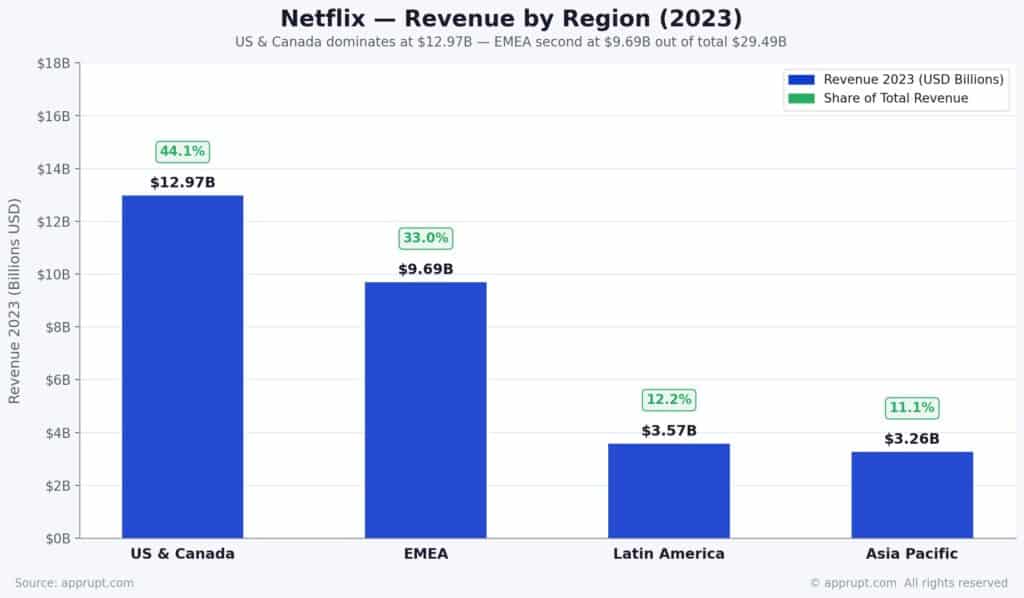

Revenue by Region

| Region | Revenue (2023) |

| US & Canada | $12.97B |

| EMEA | $9.69B |

| Latin America | $3.57B |

| Asia Pacific | $3.26B |

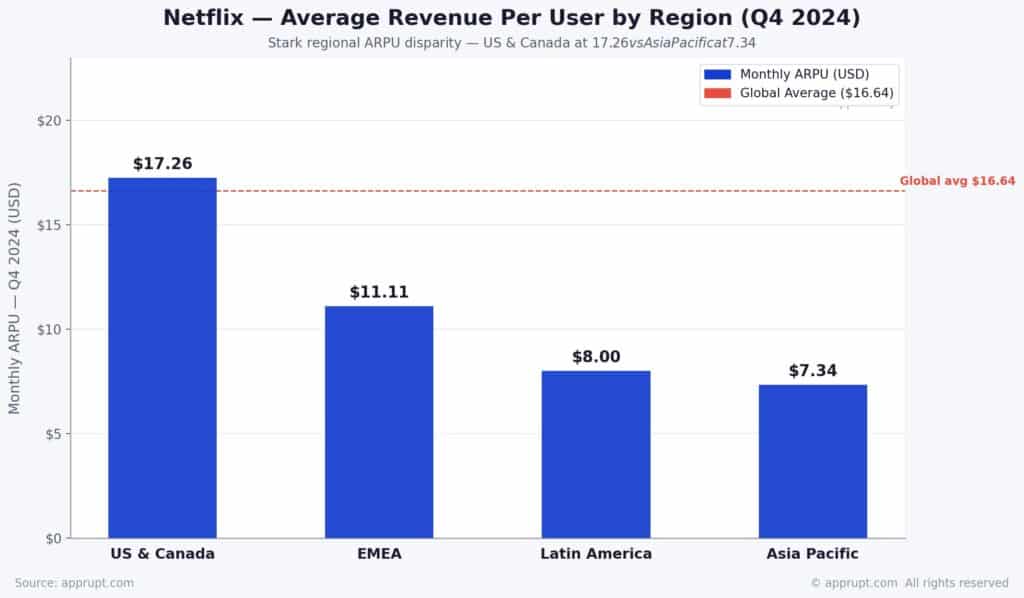

Average Revenue Per User (ARPU)

Netflix’s global average monthly ARPU stood at $16.64 as of Q4 2024. The stark regional disparities reflect different pricing strategies and economic conditions:

| Region | Monthly ARPU (Q4 2024) |

| US & Canada | $17.26 |

| EMEA | $11.11 |

| Latin America | $8.00 |

| Asia Pacific | $7.34 |

| The gap between UCAN and APAC ARPU highlights the structural under-monetization of international markets — a key opportunity for revenue growth even without major subscriber additions. |

Ad-Supported Tier

The ad-supported tier, launched in November 2022, has become a central pillar of Netflix’s growth strategy. Key statistics:

- 42% of Netflix subscribers now choose the Standard With Ads plan (Q2 2025), up from just 14% in 2023 — a threefold increase

- 40% of active Netflix accounts are on ad tiers (Q3 2025), up from 26% a year earlier

- Netflix reported 190 million monthly active viewers (MAVs) on its ad-supported tier by November 2025

- 45% of US Netflix household viewing hours were on the ad-supported tier by August 2025

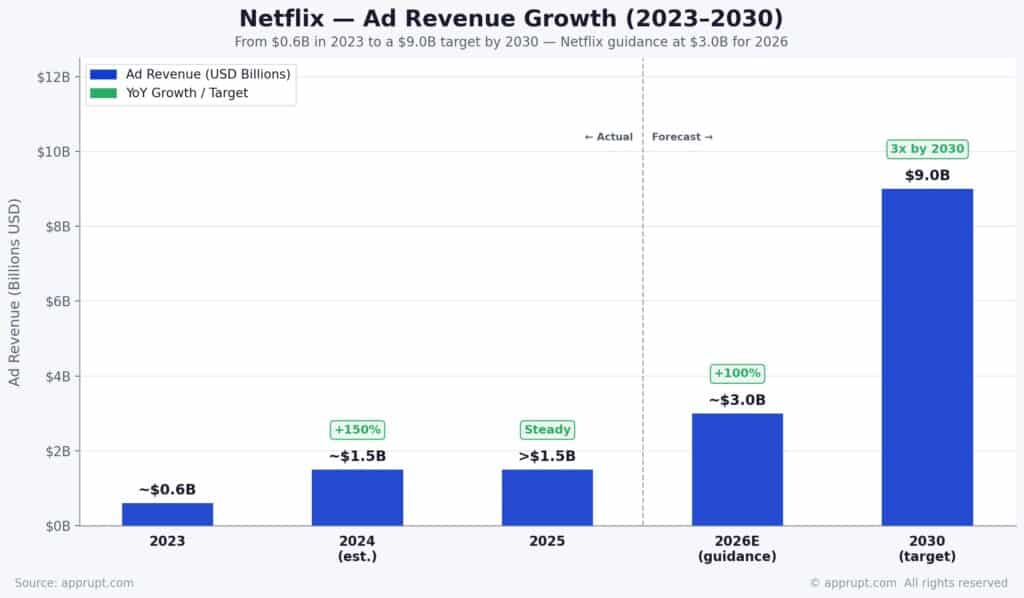

Ad Revenue Growth

| Year | Ad Revenue |

| 2023 | ~$0.6B |

| 2024 | ~$1.5B (est.) |

| 2025 | >$1.5B |

| 2026E | ~$3.0B (Netflix guidance) |

| 2030 target | $9.0B |

Netflix’s ad-supported audience skews older (two-thirds aged 35+) and less affluent, with only 28% reporting household incomes over $100,000 compared to 39% of ad-free subscribers. The tier is particularly successful at attracting cord-cutters and cord-nevers — 34% of Standard With Ads users do not subscribe to any traditional pay-TV service.

Netflix is on track to capture nearly 10% of global connected TV (CTV) ad spend by 2027, according to WARC forecasts.

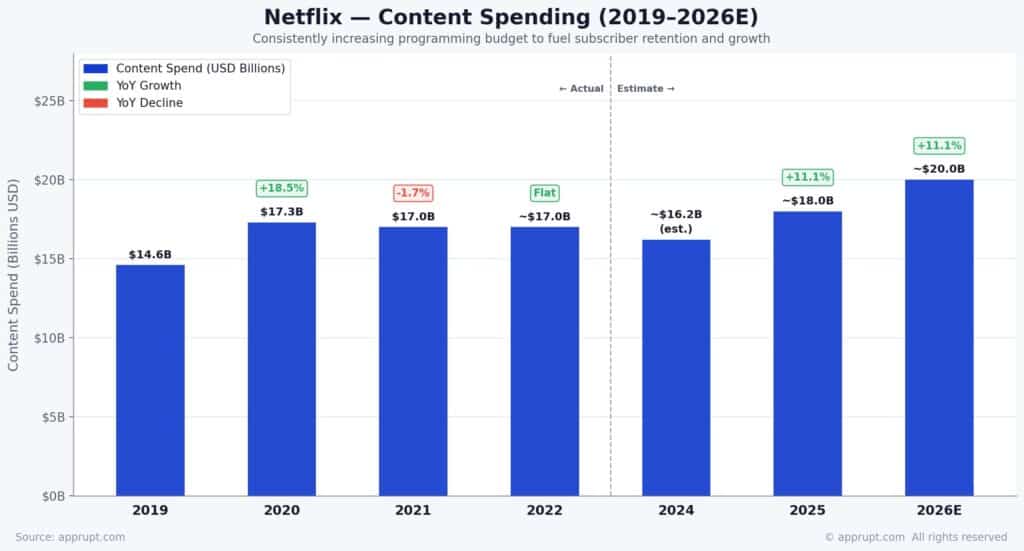

Content Spending

Netflix has consistently increased its programming budget to fuel subscriber retention and growth:

| Year | Content Spend |

| 2019 | $14.6B |

| 2020 | $17.3B |

| 2021 | $17.0B |

| 2022 | ~$17.0B |

| 2024 | ~$16.2B (est.) |

| 2025 | ~$18.0B |

| 2026E | ~$20.0B |

In 2025, Netflix released 597 new originals, up from 589 in 2024 and 568 in 2023. The library now contains approximately 4,400 originals and a total of about 7,865 titles. The 10% content spending increase planned for 2026 is expected to be front-loaded in the first half of the year.

Competitive Landscape

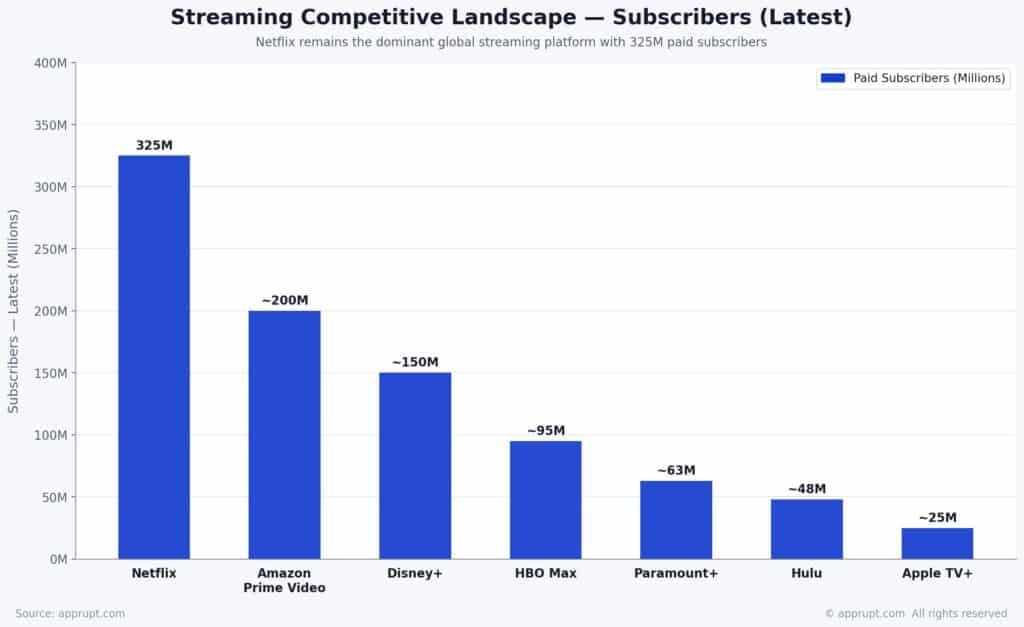

Netflix remains the dominant global streaming platform by paid subscribers:

| Platform | Subscribers (Latest) |

| Netflix | 325M |

| Amazon Prime Video | ~200M |

| Disney+ | ~150M |

| HBO Max | ~95M |

| Paramount+ | ~63M |

| Hulu | ~48M |

| Apple TV+ | ~25M |

Amazon Prime Video leads in ad-tier adoption, with 82% of its audience on ad-supported plans compared to Netflix’s 40%. Disney+ sits at 44% and HBO Max at 28%.

Netflix captures approximately 7% of available consumer entertainment spending and holds a 21% market share among US SVOD platforms. By 2029, Netflix is projected to claim a 29% share of global subscription streaming revenue, which is expected to exceed $170 billion annually.

Growth Projections (2026–2030)

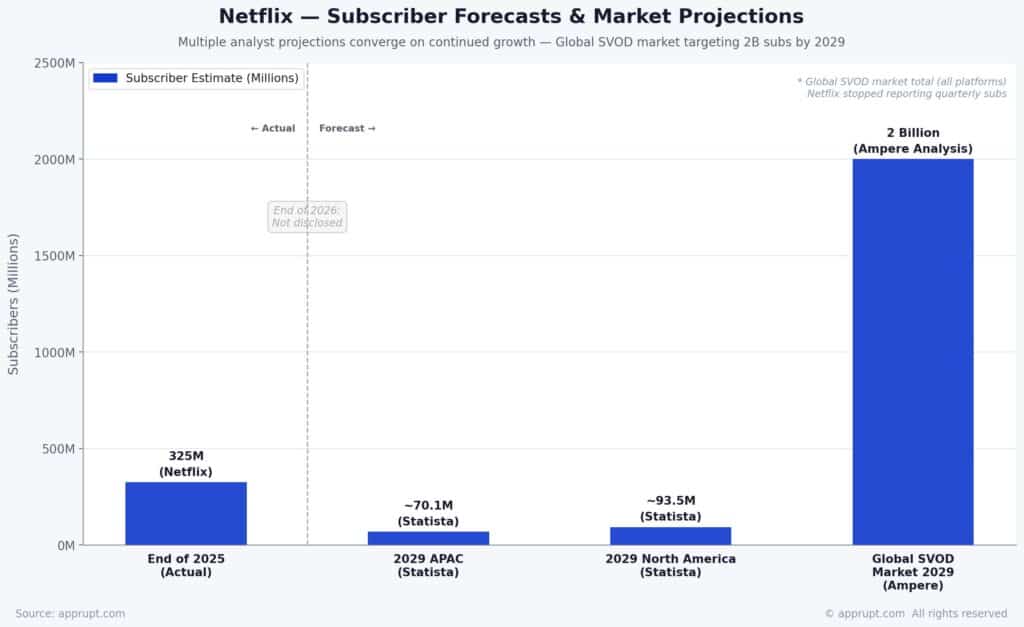

Subscriber Forecasts

Netflix’s decision to stop reporting quarterly subscriber numbers makes precise forecasting difficult. However, multiple analyst projections converge on continued growth:

| Period | Subscriber Estimate | Source |

| End of 2025 | 325M (actual) | Netflix |

| End of 2026 | Not disclosed | — |

| 2029 (APAC alone) | ~70.1M | Statista |

| 2029 (North America) | ~93.5M | Statista |

| Global SVOD market | 2 billion total subs by 2029 | Ampere Analysis |

The broader global SVOD market is projected to surpass 2 billion paid subscriptions by 2029, up from 1.8 billion today, though this represents a marked slowdown from the previous five years when subscriptions doubled.

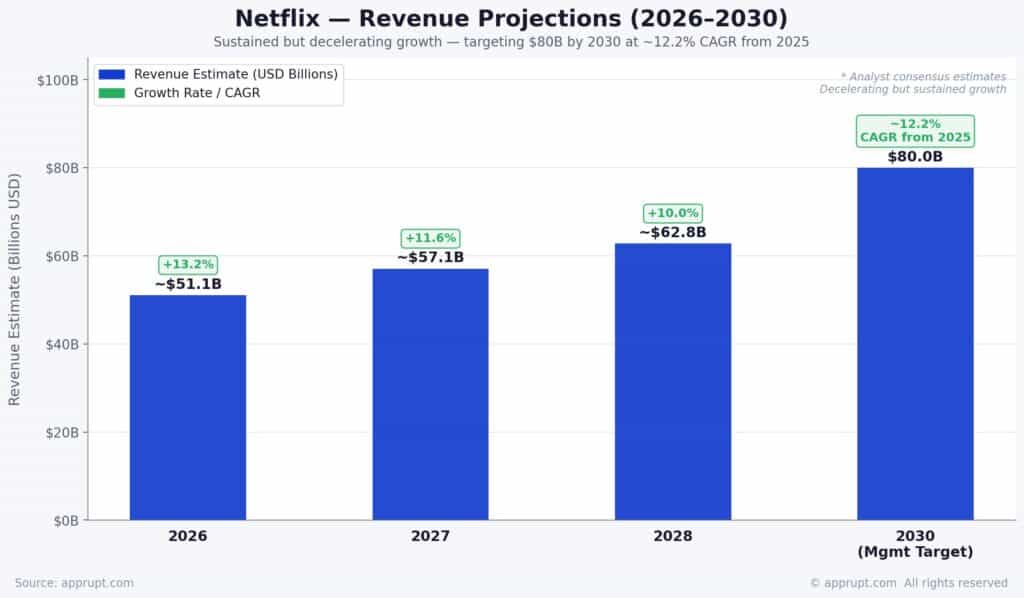

Revenue Projections

Analyst consensus estimates paint a picture of sustained but decelerating revenue growth:

| Year | Revenue Estimate | Growth Rate |

| 2026 | ~$51.1B | 13.2% |

| 2027 | ~$57.1B | 11.6% |

| 2028 | ~$62.8B | 10.0% |

| 2030 (mgmt target) | $80.0B | ~12.2% CAGR from 2025 |

Netflix’s earnings are forecast to grow at approximately 15.6% per annum, with revenue growing at 9.7% per annum over the medium term. Operating margins are expected to expand from approximately 29% in 2025 to around 33% by 2027–2028 as scale economics and advertising revenue improve profitability.

Key Growth Drivers

1. Ad-Supported Tier Expansion

Advertising revenue is expected to roughly double from $1.5 billion in 2025 to approximately $3 billion in 2026, with a long-term target of $9 billion by 2030. Netflix now reaches 190 million monthly active viewers through its ad tier across 12 countries.

2. International Expansion

The Asia-Pacific and African regions remain structurally under-penetrated. India — with penetration below 1% of its population — was Netflix’s second-largest growth market in Q4 2025. Netflix is investing $2 billion in Indian content to accelerate this growth.

3. Live Events and Sports

Netflix has expanded into live programming, including NFL Christmas Day games that drew 30 million viewers each, WWE Raw, and live interactive shows. These events drive engagement spikes and create premium ad inventory.

4. Warner Bros. Discovery Acquisition

Netflix has announced plans to acquire Warner Bros. Discovery for $82.7 billion, which would unite two of the world’s largest entertainment companies. Co-CEO Ted Sarandos has committed to maintaining 45-day theatrical windows for Warner Bros. films.

5. Gaming and Interactive Content

Netflix continues expanding into cloud gaming, with gaming engagement contributing to increased average viewing time and helping attract younger demographics.

6. AI Integration

Netflix is implementing AI systems for subtitle localization, ad customization, and algorithmic personalization. The company aspires to expand into video podcasts, music partnerships, and deeper gaming integrations.

Challenges and Risks

- Growth deceleration: Subscriber additions slowed from 41 million in 2024 to 23 million in 2025, a 44% decline in net adds

- Market saturation: Penetration in the US (53%), UK (57%), and Australia (65%) limits further growth in mature markets

- Unpaid usage: An estimated 41% of Netflix users access the platform without paying, representing both a risk and an opportunity for conversion

- Rising content costs: Content amortization is growing 10% in 2026, pressuring operating margins in the near term

- Competitive intensity: Amazon Prime Video, Disney+, and regional platforms like JioHotstar continue to compete aggressively for market share and content rights

- Opaque reporting: The cessation of quarterly subscriber reporting reduces transparency for investors and analysts

- Macroeconomic pressure: Potential tariff-driven inflation could impact US consumers’ willingness to pay for premium streaming amid price increases

Conclusion

Netflix’s position as the world’s leading streaming platform remains firmly intact with 325 million paid subscribers and $45.2 billion in annual revenue. The shift toward ad-supported monetization, international expansion into under-penetrated markets, and diversification into live events and gaming provide multiple avenues for continued growth. Revenue is projected to surpass $50 billion in 2026 and potentially reach $80 billion by 2030. However, the era of hyper subscriber growth appears to be winding down, with Netflix increasingly focused on revenue-per-user optimization and margin expansion rather than raw subscriber additions. The pending Warner Bros. Discovery acquisition, if completed, could fundamentally reshape Netflix’s competitive position and content portfolio for the decade ahead.