India’s subscription video-on-demand (SVOD) market is experiencing a transformative growth phase, driven by telecom bundling, sports-led streaming, regional content expansion, and the rapid adoption of Connected TV (CTV). The SVOD segment crossed the $1 billion revenue milestone in 2024 and is projected to reach approximately $2.68 billion by 2030. India is on track to overtake China as the world’s largest SVOD market by subscription count by 2030, with an estimated 358 million individual subscriptions. However, monetization remains structurally low, with blended ARPU at approximately $0.5 per month, and premium VOD revenue will remain 4.5x smaller than China’s and 2.5x smaller than Japan’s.

India SVOD Market Size and Revenue

SVOD Revenue Trajectory

India’s SVOD revenue has grown at a compound annual growth rate of 13–15.5% over recent years. GlobalData projected SVOD service revenue to grow from $1.3 billion in 2021 to $2.7 billion by 2026 at a 15.5% CAGR. According to MPA’s AVB 2026 report, SVOD revenue crossed the $1 billion mark in 2024 and is forecast to nearly double to $2.68 billion by 2030. PwC’s Global Entertainment & Media Outlook 2025–2029 projects total OTT revenue in India to reach $3.5 billion by 2029, with SVOD accounting for nearly 69% of the total.

Total Online Video Market

India’s total online video and OTT market revenue is projected to more than double from $4.31 billion in 2024 to $9.17 billion by 2030. AVOD continues to dominate the revenue mix, growing from $3.25 billion in 2024 to an estimated $6.48 billion by 2030, accounting for over 70% of total online video revenue. The India OTT market (including all segments beyond just media) was valued at $5.4 billion in 2025 and is projected to reach $28.1 billion by 2034 at a 19.09% CAGR.

| Metric | 2024 | 2026 (Proj) | 2029 (Proj) | 2030 (Proj) |

| SVOD Revenue | ~$1.1B | ~$1.8–2.7B | ~$2.4B (PwC) | $2.68B (MPA) |

| AVOD Revenue | $3.25B | — | — | $6.48B |

| Total OTT Revenue | $4.31B | — | $3.5B (OTT only, PwC) | $9.17B |

ARPU and Monetization Challenges

India’s SVOD market operates on a high-volume, low-ARPU model. Blended SVOD average revenue per user remains at approximately $0.5 per month, or roughly $9–12 per year. OTT revenue projections for FY2025–26 indicate the AVOD–SVOD split is shifting closer to 55:45, with SVOD ARPU at ~$1.50–$2.50/month and AVOD at ~$0.15–$0.25/month.

Subscriber Growth

Subscription Volumes

SVOD subscriptions have shown strong recovery after a dip in 2023. After falling due to cricket content moving behind paywalls on Disney+ Hotstar, subscriptions rebounded from 110 million to 120 million in H1 2024. By 2024, total paid subscriptions stood at 111 million across 47 million subscribing households (FICCI-EY), while Futuresource pegged subscriptions at 126 million, representing ~45% of Indian households.

Active paid OTT subscriptions reached 148.2 million as of mid-2025, according to Ormax Media. MPA’s latest data places total SVOD subscriptions at over 357 million, reflecting individual platform subscriptions across 75.7 million SVOD households, with an average household subscribing to approximately 4.7 OTT services.

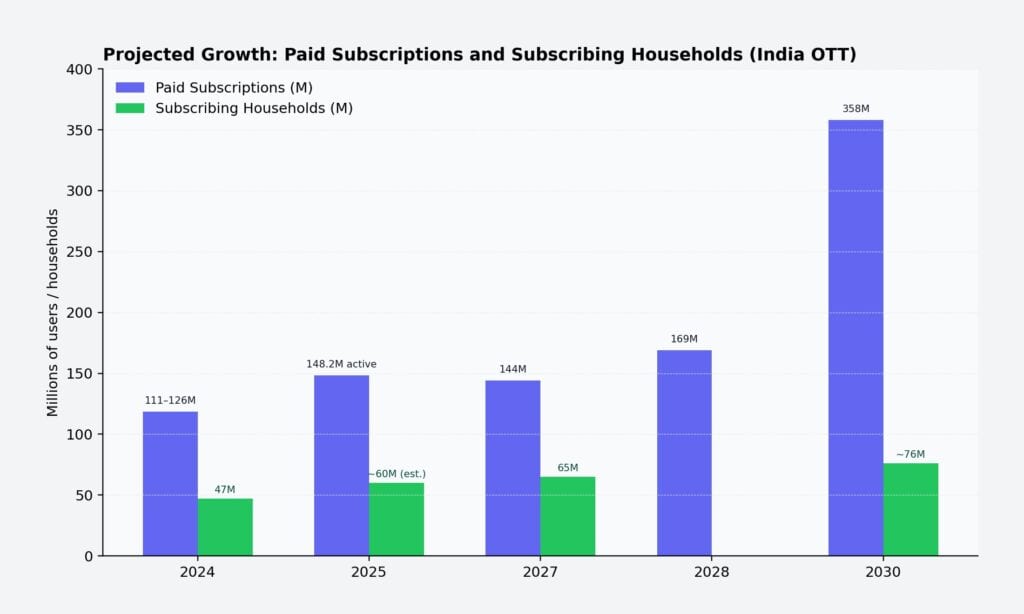

Projected Growth

| Year | Paid Subscriptions | Subscribing Households | Source |

| 2024 | 111–126M | 47M | FICCI-EY, Futuresource |

| 2025 | 148.2M active | ~60M (est.) | Ormax Media |

| 2027 | 144M | 65M | FICCI-EY |

| 2028 | 169M | — | PwC |

| 2030 | 358M | ~76M | MPA |

The FICCI-EY report projects subscribing households will grow from 47 million in 2024 to 65 million by 2027, with total paid subscriptions reaching 144 million—a nearly 30% increase. On average, each household will maintain 2.2 subscriptions. PwC forecasts the number of OTT subscriptions will reach 169 million by 2028 at a 10.8% CAGR.

India to Overtake China by 2030

According to MPA’s AVB 2026 report, India will surpass China to become the world’s largest SVOD subscription market by 2030, with 358 million individual subscriptions. Despite this, India’s combined premium VOD revenues (subscriptions + advertising) will remain 4.5x smaller than China’s and 2.5x smaller than Japan’s, underscoring the persistent monetization gap.

OTT User Base and Streaming Audience

India’s total streaming audience reached 601.2 million users in 2025, representing 41.1% of the country’s population, according to Ormax Media’s annual report. While the audience continues to grow, the rate has slowed to 10% YoY from 13–14% in 2023 and 2024, signaling market maturity.

The market is supported by 700 million internet users actively consuming audio and video content. With more than 50 active OTT subscription platforms—many streaming in regional languages—India has one of the most fragmented but competitive streaming ecosystems globally.

Platform Landscape

Market Share (Q2–Q3 2025)

The Indian SVOD market is consolidating around a top three—JioHotstar, Amazon Prime Video, and Netflix—which together command nearly two-thirds of the market.

| Platform | Interest Share (Q2-Q3 2025) | Estimated Subscribers | Revenue (Est.) |

| JioHotstar | 23–25% | ~225M+ subs | ~$1.1B |

| Amazon Prime Video | 23% | 32M+ paid | ~$500M+ |

| Netflix | 19% | 20–24M | ~$690–905M |

| Apple TV+ | 14–15% | — | — |

| Zee5 | 10% | — | — |

| Sony LIV | 5% | — | — |

JioHotstar Dominance

JioHotstar, formed from the merger of Disney’s Indian operations (Disney+ Hotstar) with Reliance’s JioCinema in 2025, has emerged as the largest platform by far. When JioHotstar shifted IPL viewers from a freemium model to paid subscriptions in early 2025, its subscriber base surged from ~50 million to nearly 300 million within four months. The platform holds exclusive streaming rights for IPL cricket and for Warner Bros./HBO and Disney content in India, with a local content library spanning 320,000 hours—roughly six times the size of Netflix’s Indian catalogue.

Netflix India

Netflix India’s revenue reportedly reached $905 million in 2025 (HSBC estimate), representing about 2% of Netflix’s global total. The platform has expanded to over 24 million subscribers in India and maintains strong urban engagement, though its absence from sports content and selective approach to mainstream Indian content limits incremental growth.

Amazon Prime Video

Amazon Prime Video crossed 32 million subscribers in India, generating revenues exceeding $500 million, aided significantly by bundling with Amazon’s e-commerce ecosystem. In June 2025, Amazon Prime Video turned its entry-level offering in India into an AVOD service with limited advertisements, reflecting the global shift toward ad-supported tiers.

Connected TV (CTV) Revolution

One of the most significant structural shifts in India’s streaming landscape is the explosive growth of Connected TV usage.

India’s CTV user base surged 85% year-on-year, from 69.7 million in 2024 to 129.2 million in 2025, representing approximately 35–40 million CTV households. CTV has overtaken laptops and tablets to become the #2 device for streaming in India after smartphones. Among OTT audiences, 21% now use CTV to stream videos, up from 13% in 2024.

Key CTV statistics:

- 50% CTV penetration among OTT audiences in India’s six metro cities

- 75.8 million CTV users in small towns and villages (up from 40.4 million in 2024)

- Delhi NCR, Karnataka, and Maharashtra lead as top states for CTV penetration

- 44% of Indian viewers pay for 3–4 streaming platforms; average viewer subscribes to 3 services and spends over ₹1,360/month

- CTV households may surpass 60 million, overtaking India’s shrinking pay-TV base of ~59.91 million DTH subscribers

This shift from mobile-first to multi-screen viewing is transforming family consumption patterns and driving premium content strategies across platforms.

Key Growth Drivers

Telecom Bundling

OTT bundling by telecom operators is the single largest driver of subscription growth. Bharti Airtel launched IPTV services with content from 29 OTT apps, while Jio and Vi offer more than a dozen streaming apps with their plans. This strategy mirrors the role previously played by Distribution Platform Operators in the pay-TV era.

Sports Content

Sports, especially cricket, remains the most powerful subscriber acquisition tool. IPL 2024 and the ICC Men’s T20 World Cup were the top two sports properties driving viewership, with sports content attracting the highest number of unique viewers—9 of the top 15 titles in H1 2024 belonged to the sports genre. JioHotstar’s control of IPL streaming rights has been central to its massive subscriber growth.

Regional and Local Content

Local content accounted for 86% of premium VOD engagement in H1 2024. Platforms are investing heavily in regional language originals—Tamil, Telugu, Malayalam, Bengali, Marathi—to reach Tier 2 and Tier 3 audiences. The “language barrier has been completely broken” in Indian streaming, with audiences increasingly open to diverse content.

Digital Infrastructure

India’s broadband subscriber base has grown from 788 million to 944 million between 2022 and 2025. The upcoming expansion of 5G networks will further aid SVOD growth by facilitating seamless streaming experiences. Cheap mobile data (driven by Reliance Jio’s market entry) and improved digital payment systems like UPI continue to lower barriers to adoption.

Future Outlook (2026–2030)

Revenue Projections

The SVoD segment is forecast to sustain annual value growth of approximately 13% through 2029, driven by tailored offers, regional productions, exclusive sports rights, and short-form formats such as micro-dramas. Between 2025 and 2030, the premium video-on-demand category across Asia-Pacific (including SVOD and premium AVOD) will add about $12.5 billion in incremental revenue, reaching $52 billion.

Market Structure Evolution

- Consolidation: The market is consolidating around the top three players. The decline in “others” category share indicates shrinking space for smaller, standalone services.

- Hybrid models: Almost all major SVOD services now have ad-supported tiers. A hybrid AVOD+SVOD offering is seen as the way forward, especially given India’s relatively low digital ad rates.

- Content diversification: While crime and action genres dominate (60%+ of content), platforms will need to diversify to appeal to women, youth, and elderly audiences.

- SVOD share increase: SVOD is expected to account for 65% of the OTT market by 2028, up from current levels.

Emerging Trends

- Micro-dramas: Short-form scripted content targeting younger audiences is emerging as a new growth format.

- AI-enabled content: AI is being deployed across the content value chain for personalization, campaign optimization, and production efficiency.

- CTV advertising: As CTV households surpass pay-TV, advertising budgets are rapidly rebalancing toward connected screens.

- Subscription stacking: Multi-platform household consumption is deepening, with the average subscribing household paying for 2.2–4.7 services depending on the measurement source.

Data Summary

| Statistic | Value | Source |

| India SVOD revenue (2024) | ~$1.1B | MPA |

| India SVOD revenue (2030 proj.) | $2.68B | MPA |

| Total OTT market (2024) | $4.31B | MPA |

| Total OTT market (2030 proj.) | $9.17B | MPA |

| SVOD subscriptions (2025) | 148.2M active paid | Ormax |

| SVOD subscriptions (2030 proj.) | 358M | MPA |

| Subscribing households (2024) | 47M | FICCI-EY |

| Subscribing households (2027 proj.) | 65M | FICCI-EY |

| OTT streaming audience (2025) | 601.2M | Ormax |

| Connected TV users (2025) | 129.2M | Ormax |

| SVOD ARPU (monthly) | ~$0.50 | MPA |

| #1 platform by subs | JioHotstar (~225M+) | MPA |

| India to overtake China (SVOD subs) | By 2030 | MPA |