The global IPTV (Internet Protocol Television) market is experiencing explosive growth in 2026, with market valuations ranging from $109.34 billion to $221.62 billion depending on scope definitions across different research firms. IPTV subscribers are projected to reach approximately 398 million globally by 2026, officially surpassing cable TV subscribers for the first time. The market is expanding at a compound annual growth rate (CAGR) of 14.8%–17.4%, driven by 5G deployment, AI-powered personalization, cloud-based infrastructure, and the global shift from traditional cable to IP-based content delivery.

Asia-Pacific dominates the subscriber landscape with China alone accounting for 226 million IPTV subscribers, while North America leads in revenue generation. The industry faces headwinds from cord-cutting to pure OTT services and growing piracy networks, but remains positioned for strong growth through 2032 and beyond.

Global Market Size and Valuation

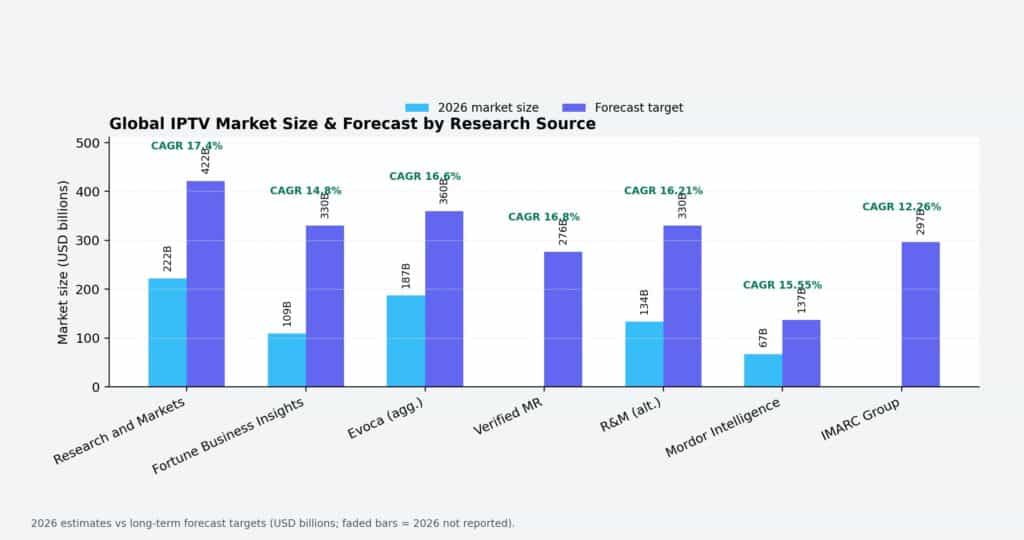

The IPTV market has seen remarkable growth from $72.24 billion in 2020 to an estimated $187.01 billion in 2026. Different research firms report varying 2026 valuations due to differences in scope — whether they include hardware sales, OTT revenues, or only managed IPTV services:

| Source | 2026 Market Size | Forecast Target | CAGR |

| Research and Markets | $221.62B | $421.53B by 2030 | 17.4% |

| Fortune Business Insights | $109.34B | $330.19B by 2034 | 14.8% |

| Evoca (aggregated) | $187.01B | $359.7B by 2029 | 16.6% |

| Verified Market Research | — | $276.38B by 2032 | 16.8% |

| Research & Markets (alt.) | $133.76B | $330.44B by 2032 | 16.21% |

| Mordor Intelligence | $66.63B | $137.22B by 2031 | 15.55% |

| IMARC Group | — | $296.84B by 2033 | 12.26% |

The wide range in estimates — from $66.63 billion (Mordor Intelligence, which excludes unmanaged OTT and device revenues) to $221.62 billion (Research and Markets, which includes broader ecosystem components) — underscores how critical scope definitions are when interpreting IPTV market data. What remains consistent across all sources is a double-digit CAGR ranging from 12% to 17.4%, signaling robust demand.

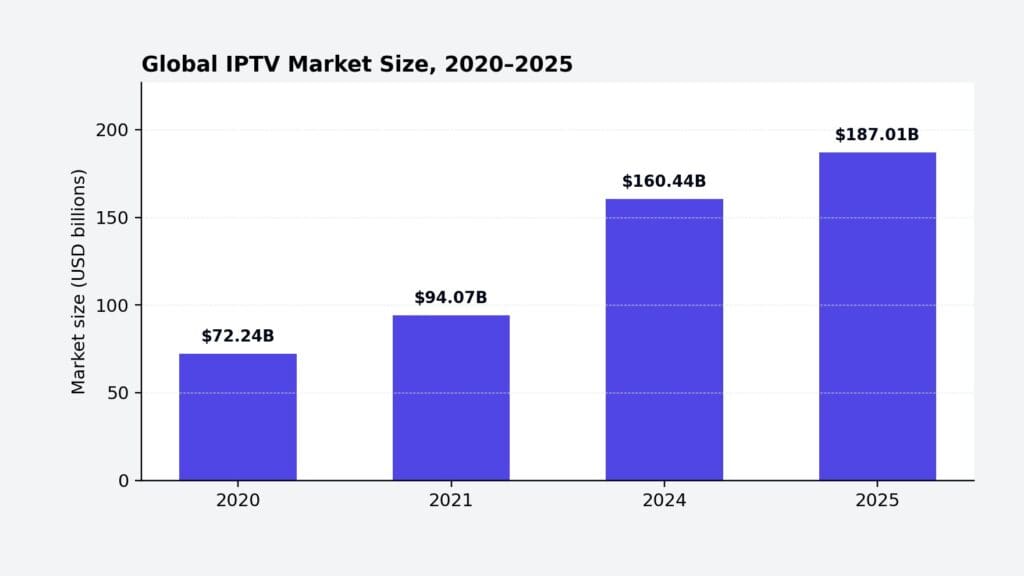

Historical Market Growth Trajectory

The IPTV market has shown accelerating momentum over the past six years:

| Year | Market Size (USD Billion) |

| 2020 | $72.24 |

| 2021 | $94.07 |

| 2024 | $160.44 |

| 2025 | $187.01 |

This trajectory represents a 159% increase from 2020 to 2025, accelerated by pandemic-driven shifts in viewing habits, increasing cord-cutting, and the rollout of fiber-to-the-home infrastructure that surpassed 600 million global lines by late 2025.

Global Subscriber Statistics

Total IPTV Subscribers

IPTV holds approximately 250 million active subscribers worldwide as of 2026, with projections indicating the total will reach 398 million by end of 2026, officially surpassing global cable TV subscriber numbers for the first time in history. The 63 million subscriber additions between 2021 and 2026 reflect the ongoing global transition from traditional broadcast to IP-based content delivery.

Subscribers by Region and Country

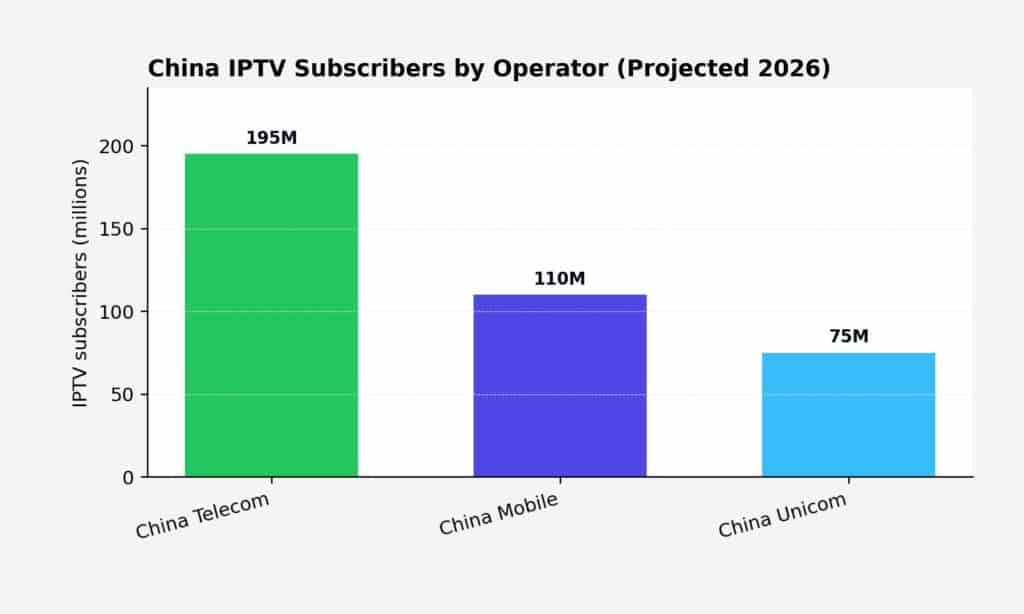

China dominates the global IPTV subscriber base with 226 million subscribers projected by 2026, accounting for approximately 57% of global IPTV subscribers. The three major Chinese telecom operators drive this dominance:

| Operator | IPTV Subscribers |

| China Telecom | 195 million |

| China Mobile | 110 million |

| China Unicom | 75 million |

China is expected to add 19 million IPTV subscribers between 2021 and 2026, while simultaneously losing 39 million cable TV subscribers during the same period. By end-2026, China will retain only 89 million cable subscribers, down sharply from previous years.

India is projected to contribute 178 million pay TV subscribers by 2026, though its IPTV-specific segment has been complex. Notably, India’s registered IPTV connections fell 85.7% from 619,284 to 88,504 between 2023 and 2025, even as the number of IPTV service providers increased from 23 to 53. Major telecom players like Airtel have begun testing IPTV services, suggesting the Indian market may be on the cusp of a new growth phase. India’s fiber base crossed 35 million lines by mid-2025, supporting approximately 2 million new IPTV additions each month.

Together, China and India will supply roughly half of the world’s total pay TV subscribers by 2026, with China alone providing nearly one-third of the global total at 315 million.

Regional Market Analysis

Revenue Share by Region

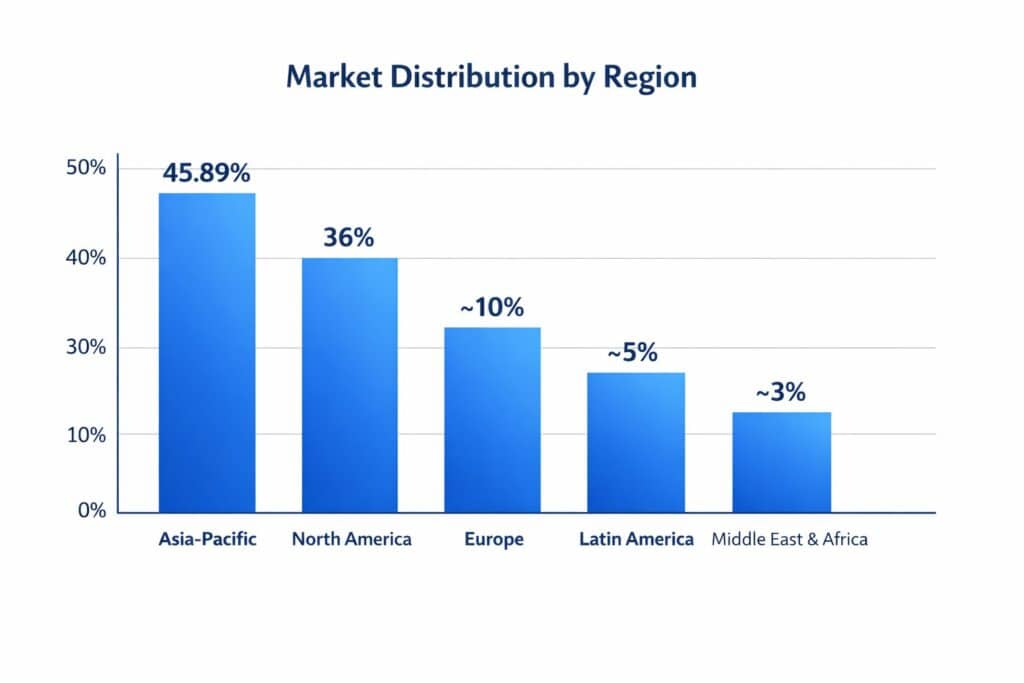

Asia-Pacific is the undisputed leader in IPTV, accounting for 45.89% of global revenue in 2025 and growing at a 16.3% CAGR from 2026 to 2031. The region’s dominance is fueled by population scale, affordable internet access, and rapid technology adoption.

| Region | Revenue Share | Key Drivers |

| Asia-Pacific | 45.89% | 380M Chinese IPTV subs, India fiber growth, Japan 4K adoption |

| North America | 36.00% | Streaming dominance, bundled services, fiber expansion |

| Europe | ~10% | Super-aggregation platforms, MagentaTV bundling Netflix/Disney+ |

| Latin America | ~5% | Brazil’s 28M fiber homes, Claro and Vivo 4K IPTV launches |

| Middle East & Africa | ~3% | Saudi STC and UAE Etisalat bundling IPTV with 5G |

North America

The United States remains the largest single IPTV market by revenue, valued at $32.6 billion in 2024 and projected to grow to $106.7 billion by 2033 at a 12.4% CAGR. The U.S. leads with widespread streaming adoption, while Canada focuses on bundled IPTV services. Despite overall pay-TV subscriber losses — with U.S. cable subscribers dropping to 68.7 million in 2025 from 105 million in 2010 — fiber broadband footprints continue to expand, giving operators headroom to upsell streaming bundles.

Europe

Europe faces persistent cord-cutting, with a 3.2% decline in pay-TV subscribers in 2024, hardest hit in Spain and Italy. However, super-aggregation platforms are reversing app fatigue — Viaccess-Orca’s unified guide platform served 15 European operators by late 2025, reducing average monthly churn by 18%. Deutsche Telekom’s MagentaTV added 400,000 subscribers in 2024 after years of decline, largely by bundling Netflix and Disney+ under a single interface. Germany and the UK are key contributors, comprising about 30% of Europe’s IPTV market share.

Emerging Markets

Africa is seeing mobile operators pair fixed-wireless home broadband with IPTV, bypassing copper scarcity. Nigeria’s broadband lines reached 8.2 million by mid-2025, up from 5.1 million two years earlier. In the Middle East, Saudi Arabia’s STC and UAE’s Etisalat bundled IPTV with 5G to secure 3.5 million subscribers across 2024-2025. Brazil leads South America with 28 million fiber-connected homes, enabling Claro and Vivo to launch 4K IPTV services.

Market Segmentation

By Revenue Model

Subscription-based IPTV dominates the market with 71.4% of revenue in 2025, driven by live sports and bundled OTT offers. However, advertising-supported video-on-demand (AVoD) is the fastest-growing segment at 16.3% CAGR.

| Revenue Model | Revenue Share (2025) | Growth Rate (CAGR) |

| Subscription IPTV | 71.4% | 14.8% |

| Ad-Supported (AVoD) | Growing rapidly | 16.3% |

| Pay-Per-View | Declining | Migrating to subs/AVoD |

The free, ad-supported streaming segment is expected to account for 73.6% of the IPTV market in the coming years, indicating a massive structural shift toward advertising-supported models. Cost-sensitive households increasingly opt for free tiers with four to six minutes of ads per hour, particularly in India, Brazil, and Indonesia. Connected-TV ad spend in the U.S. was projected at $29.5 billion for 2025.

By Streaming Type

Live and linear television still delivered 54.6% of streaming revenue in 2025, anchored by sports and news programming. Video-on-demand is advancing at a 15.61% CAGR as consumers shift to asynchronous viewing patterns. Research from Boston Consulting Group tracked a 12-minute daily decline in live viewing against an 18-minute rise in on-demand viewing across Europe between 2022 and 2024.

Sports remain the stronghold of live viewing — 92% of UEFA 2024 Champions League streams were consumed in real time. However, highlights, condensed replays, and personalized clip compilations are growing quickly among younger viewers.

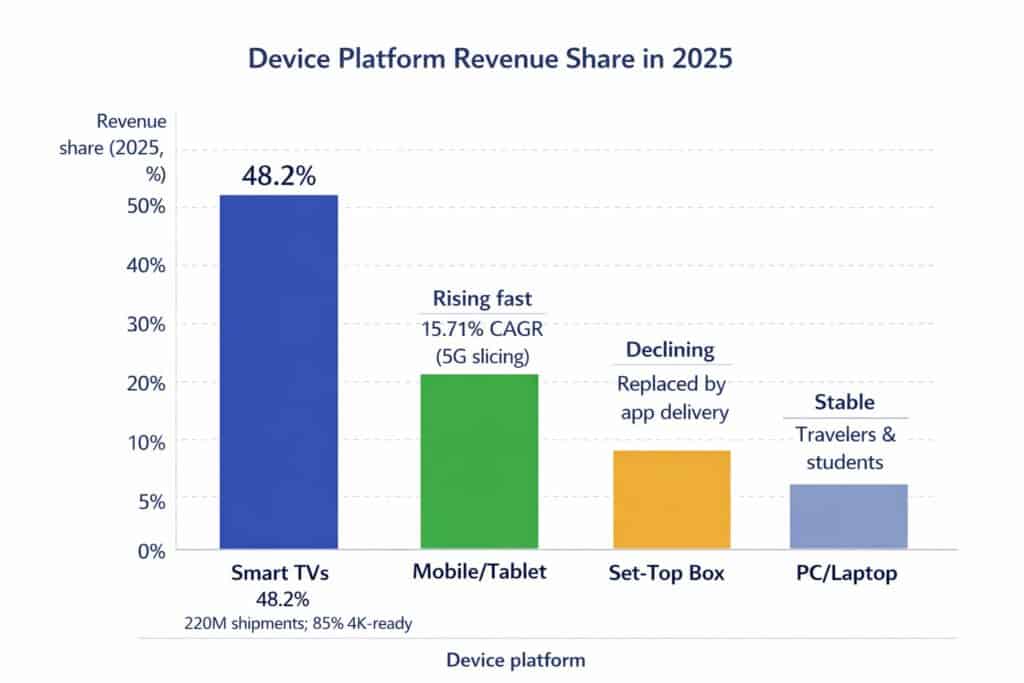

By Device Platform

| Device | Revenue Share (2025) | Trend |

| Smart TVs | 48.2% | 220M shipments in 2025, 85% supporting 4K |

| Mobile/Tablet | Rising fast | 15.71% CAGR, driven by 5G network slicing |

| Set-Top Box | Declining | Being replaced by app-based delivery |

| PC/Laptop | Stable | Serves travelers and students |

Mobile and tablet viewing is rising at 15.71% CAGR as 5G subscriptions hit 1.9 billion globally by mid-2025, with edge caching dropping latency under 10 milliseconds.

By Component

Hardware generated 63.2% of revenue in 2025, driven by set-top boxes, middleware servers, and encoders. Services revenue is climbing at 15.8% CAGR as operators shift toward opex-friendly managed platforms and cloud middleware from Ericsson, Cisco, and Huawei.

IPTV vs. Cable TV

Subscriber Crossover

2026 marks a historic inflection point: IPTV subscribers will officially surpass cable TV subscribers globally. This shift is primarily driven by China, where the massive migration from cable to IPTV continues unabated.

In the United States, streaming now captures 47.3% of all TV viewing time compared to cable’s 24.1%. Cable subscribers have dropped to 68.7 million households in 2025, a 35% decline from 105 million in 2010. U.S. pay-TV providers lost 5.9 million subscribers in 2024 alone, dropping below 70 million for the first time in decades.

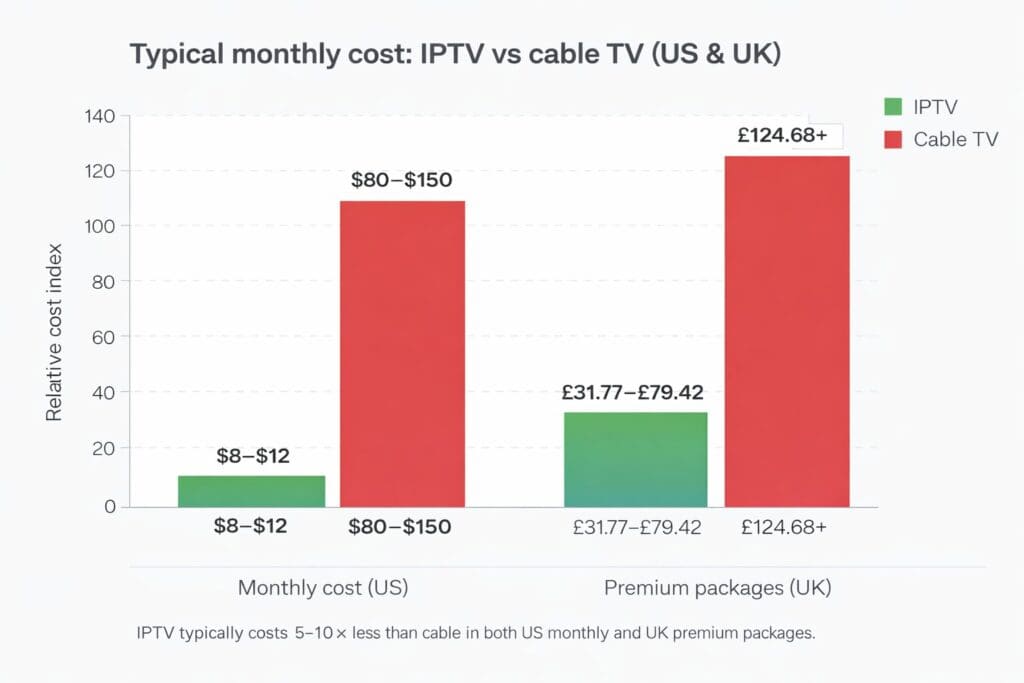

Cost Comparison

IPTV offers dramatically lower costs than traditional cable, particularly in the United States:

| Metric | IPTV | Cable TV |

| Monthly cost (US) | $8–$12 | $80–$150 |

| Premium packages (UK) | £31.77–£79.42 | £124.68+ |

| Equipment | One-time purchase ($30–$100) | Monthly rental ($10–$20/box) |

| Contract | Month-to-month | Long-term contracts with penalties |

| Content library | 15,000+ live channels, 40,000+ VOD | Pre-defined bundles |

Key Growth Drivers

5G Networks and Infrastructure

The advent of 5G offers significant growth potential through network slicing and enhanced content distribution. 5G leverages MIMO and beamforming techniques to maximize network utilization, providing reduced distortion and greater precision in signal transmission. The ability to distribute heavy traffic from cloud-based content libraries due to high bandwidth capability further accelerates IPTV adoption.

AI-Powered Personalization

Artificial intelligence is increasingly embedded in IPTV platforms for personalized recommendations, dynamic content curation, voice search, and targeted advertising. AI-based voice-enabled search allows users to explore content using natural language, and AI-enabled set-top boxes with voice assistants help service providers gain larger subscriber bases. Behavioral data analysis supports targeted advertising, improving CPMs by up to 3x relative to broadcast television.

Fiber-to-the-Home Rollouts

Global fiber lines surpassed 600 million by late 2025, creating throughput for data-hungry 4K and 8K streams that consume 25 Mbps and 100 Mbps respectively. Operators now price ultra-high-definition tiers at 30%–50% premiums. By mid-2025, 68% of NTT East and West fiber customers were watching 4K IPTV weekly.

Telco Convergent Bundles

Telecom bundling is a major growth lever. China Telecom’s Smart Home bundle combined gigabit fiber, 200+ channels, and unlimited mobile data for $42/month, adding 8.5 million accounts in nine months of 2025. Reliance Jio’s postpaid fiber plan bundling 14 OTT apps and four SIM cards registered 2.3 million additions by mid-2025.

Cloud-Based IPTV Solutions

IPTV providers are migrating to cloud-native infrastructure with auto-scaling bandwidth, CDN integration, lower costs, and faster deployment. Cloud-based services enable seamless updates, security patching, and high availability — critical for scaling operations.

Interactive IPTV and Smart Home Integration

IPTV is becoming increasingly interactive, with emerging capabilities including real-time voting during live shows, multi-angle sports viewing, in-video shopping, and AR overlays for fitness and tutorial content. Integration with smart home ecosystems means voice-controlled television is becoming mainstream.

Piracy and Challenges

Illegal IPTV Networks

Piracy remains a significant challenge. Over 1.5 million households across Denmark, Finland, Norway, and Sweden now subscribe to illegal IPTV platforms — a 16% increase from spring 2024, representing 200,000 additional households joining within just one year. Illegal IPTV usage is more common among younger individuals and men, with men representing 60% or more of users.

In 2025, Europol coordinated its most aggressive EU-wide enforcement operations against IPTV networks, with investigators from over 15 countries tracing €47 million in cryptocurrency linked to illegal streaming services. They mapped 69 piracy and streaming sites and flagged 25 IPTV operations attracting nearly 12 million visitors annually. Piracy costs Europe approximately $1 billion annually.

Silent Push researchers uncovered a massive piracy network spanning over 1,000 domains and 10,000 IP addresses, affecting more than 20 major brands including Netflix, Disney+, HBO, Prime Video, and multiple sports leagues. These illicit services offer approximately 22,500 channels and 100,000 movies for as little as $15/month.

Cord-Cutting to Pure OTT

The shift toward pure OTT streaming platforms poses a restraint on managed IPTV growth, with an estimated -2.8% impact on CAGR in North America and Europe. Ofcom reported 1.4 million fewer traditional TV homes in the UK in 2024, with streaming-only households reaching 62%.

Bandwidth Bottlenecks

Unicast bandwidth bottlenecks during peak sporting events remain a concern. Akamai logged 18.7 million concurrent UEFA 2024 Championship streams, forcing adaptive bit-rate downgrades for 22% of viewers as edge servers saturated. Large live events can exceed provisioned capacity by up to 50% during early minutes.

Competitive Landscape

The IPTV market features moderate concentration, with incumbent telcos commanding local scale through fiber assets and established billing relationships.

Key Industry Players

| Category | Major Players |

| Telecom Operators | AT&T, Verizon, Deutsche Telekom, Orange, BT, Telefónica, China Telecom |

| Equipment/Middleware | Cisco (Infinite Video Platform), Ericsson (MediaFirst), Huawei (OptiXstar) |

| CDN Providers | Akamai, Cloudflare, Broadpeak |

| Challengers | Amino Technologies, Sagemcom, Broadpeak (cloud-native stacks) |

Ericsson activated MediaFirst for three additional European operators in June 2025, each cutting operating costs by up to 30% through cloud delivery. Huawei’s OptiXstar uses machine learning to allocate bandwidth dynamically, reducing buffering by 32% in field trials. Comcast’s open-source RDK middleware now powers 80 million boxes worldwide.

Future Outlook (2027–2032)

The IPTV market is projected to maintain strong double-digit growth through the end of the decade, with most forecasts placing the market between $330 billion and $421 billion by 2030–2032. Key trends that will define the next phase include:

- 8K content becoming mainstream as fiber penetration deepens and video compression (HEVC, AV1) cuts bandwidth requirements by 40%

- AVoD overtaking subscription as the primary revenue model, with hybrid models combining small fees with lighter ad loads gaining favor

- Super-aggregation platforms that merge linear channels with Netflix, Disney+, and free ad-supported streams becoming the default interface

- VR and AR integration with IPTV for immersive viewing experiences, particularly in gaming and interactive entertainment

- 5G fixed-wireless access bypassing fiber in emerging markets, enabling IPTV delivery in regions lacking traditional broadband infrastructure

- AI-driven churn prediction identifying at-risk subscribers and enabling proactive retention strategies

The convergence of telecommunications and entertainment will continue to accelerate, with IPTV positioned not merely as an alternative to traditional television, but as its successor.