Free Ad-Supported Streaming TV (FAST) has transitioned from a niche disruptor to a core pillar of the global television ecosystem. The global FAST market is projected to grow from approximately $10.6 billion in 2025 to $12.23 billion in 2026, with long-term forecasts placing it between $18.8 billion and $46.49 billion by 2030–2033 depending on the research firm and scope. FAST viewership in the United States surged 43% year-over-year through August 2025, reaching 1.8 billion hours, while platforms like Tubi, Samsung TV Plus, and The Roku Channel each now exceed or approach 100 million monthly active users globally. With nearly 1,900+ active FAST channels worldwide, 64% of U.S. homes watching FAST content, and CTV ad spending projected to hit $38 billion in 2026, the sector is firmly positioned as a structural growth engine in television.

FAST Channel Global Market Size & Revenue Forecasts

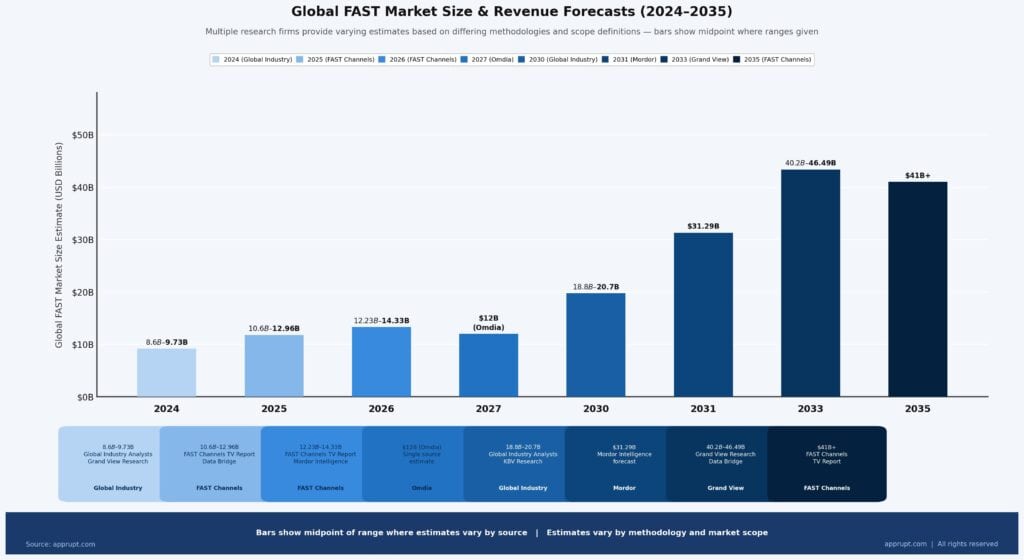

Multiple research firms provide varying FAST market size estimates based on differing methodologies and scope definitions. The table below consolidates the key projections:

| Year | Market Size Estimate | Source |

| 2024 | $8.6B–$9.73B | Global Industry Analysts; Grand View Research |

| 2025 | $10.6B–$12.96B | FAST Channels TV Report; Data Bridge |

| 2026 | $12.23B–$14.33B | FAST Channels TV Report; Mordor Intelligence |

| 2027 | $12B (Omdia) | Omdia |

| 2030 | $18.8B–$20.7B | Global Industry Analysts; KBV Research |

| 2031 | $31.29B | Mordor Intelligence |

| 2033 | $40.2B–$46.49B | Grand View Research; Data Bridge |

| 2035 | $41B+ | FAST Channels TV Report |

The compound annual growth rates (CAGR) across forecasts range from 13.9% to 17.31% depending on the period and source. A key contextual point: FAST channel revenue grew almost 20x between 2019 and 2022, from approximately $200 million to just under $4 billion. The market is expected to at least triple from its 2022 base by 2027.

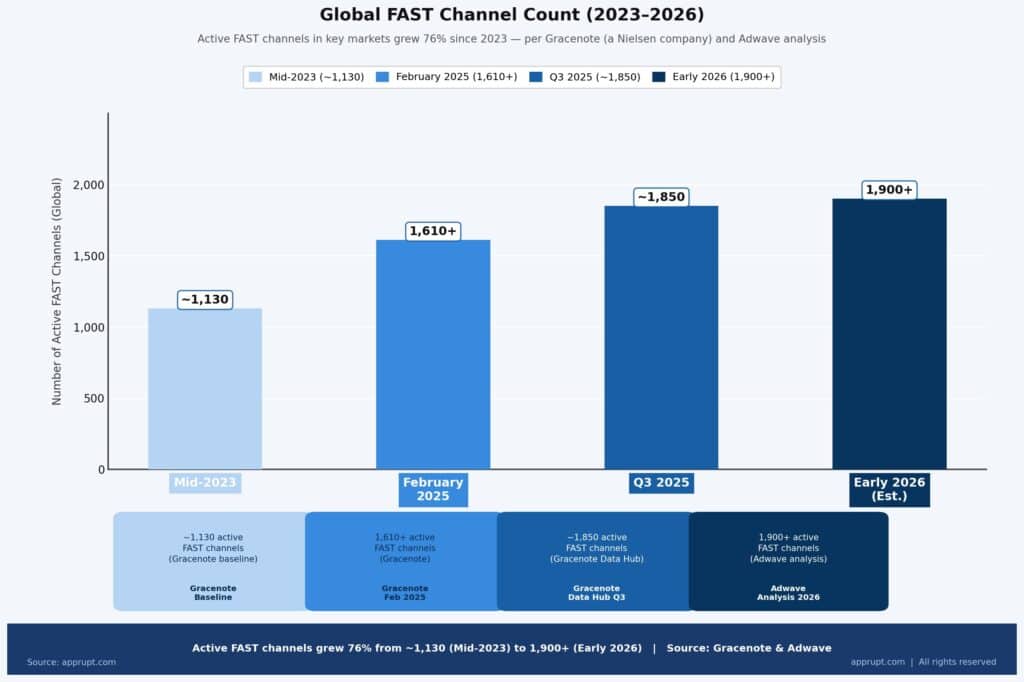

FAST Channel Count

The number of active FAST channels globally has expanded rapidly. According to Gracenote (a Nielsen company), active FAST channels in key markets grew 76% since 2023:

| Period | Active FAST Channels | Source |

| Mid-2023 | ~1,130 | Gracenote baseline |

| February 2025 | 1,610+ | Gracenote |

| Q3 2025 | ~1,850 | Gracenote Data Hub |

| Early 2026 (est.) | 1,900+ | Adwave analysis |

By country, the United States dominates with approximately 74% of all active FAST channels (1,189 channels as of February 2025), followed by the United Kingdom (153), Germany (109), and Canada (89). Samsung TV Plus alone offers more than 4,300 free channels across 30 countries, with nearly 700 available in the U.S..

Content Across FAST Channels

FAST channels now host more than 197,000 individual programs. Entertainment is the most common genre (300+ channels), followed by sports (220+) and reality (138). Notably:

- Reality programming channels surged 626% since mid-2024

- Sports channels grew 105%+ over the same period

- Nearly 50% of current FAST programming was produced in the last 5 years, compared to about one-third on premium SVOD

- 93.1% of available FAST content is TV programming (by episode count)

U.S. FAST Viewership Statistics

Viewing Hours & Household Penetration

FAST viewership in the United States has reached a critical inflection point. Key metrics as of late 2025 and into 2026 include:

- 1.8 billion hours of FAST content streamed through August 2025, up 43% year-over-year from 1.3 billion hours

- 64% of U.S. homes currently watch FAST content

- 47% of U.S. households watch FAST channels on a weekly basis

- 57% of households that were streaming only ad-free in 2020 now watch FAST content

- FAST services reach 45% of U.S. internet-connected households

- By 2026, FAST viewership is expected to exceed 120 million annual viewers in the U.S., a 21% increase

Engagement Metrics

Viewer engagement is deepening, not just broadening. According to Wurl’s 2025 CTV Trends Report:

- Monthly active FAST households grew 12% year-over-year

- Average daily FAST viewing hours per household climbed 16% YoY

- Total hours of viewing across ad-supported streaming channels surged 29% YoY

- Average FAST channel session duration increased 25%

- Viewers spent 25% more time on a single channel before switching

Share of Total TV Viewing

According to Nielsen’s The Gauge, the three leading FAST platforms—Pluto TV, The Roku Channel, and Tubi—combined for 5.7% of total TV viewing in May 2025. This figure is larger than any individual broadcast network’s share during the same period. If FAST viewership across all channels were aggregated as a single app, it would rank as the fourth-largest on Roku by reach.

In December 2025, The Roku Channel captured a record-breaking 3% share of total U.S. television viewership.

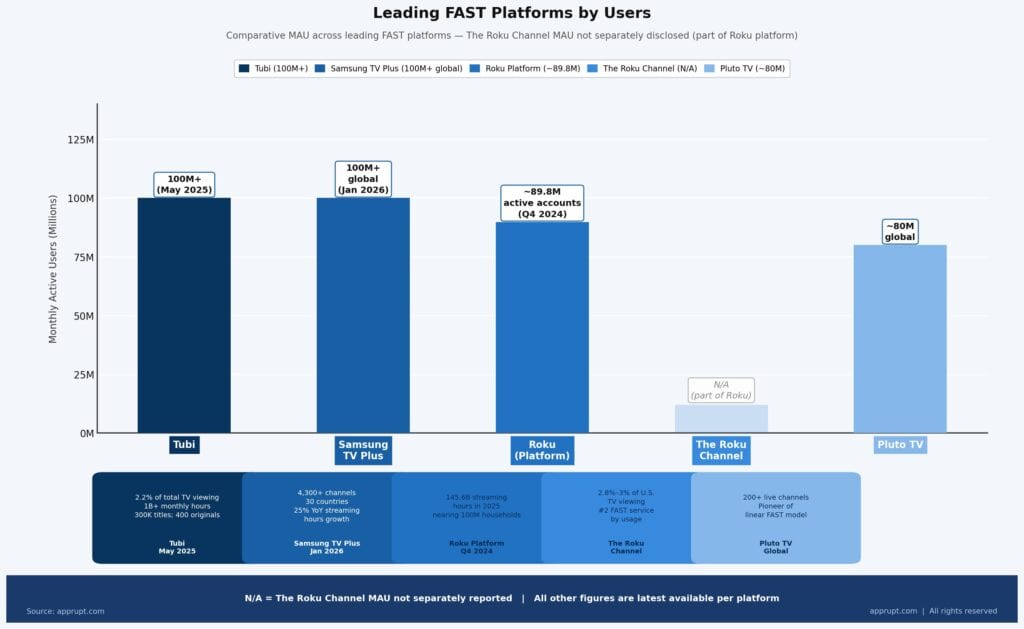

Leading FAST Platforms by Users

| Platform | Monthly Active Users | Key Highlights | Source |

| Tubi | 100M+ (May 2025) | 2.2% of total TV viewing; 1B+ monthly hours; 300K titles; 400 originals | |

| Samsung TV Plus | 100M+ global (Jan 2026) | 4,300+ channels; 30 countries; 25% YoY streaming hours growth | |

| Roku (platform) | ~89.8M active accounts (Q4 2024) | 145.6B streaming hours in 2025; nearing 100M households | |

| The Roku Channel | N/A (part of Roku) | 2.8%–3% of U.S. TV viewing; #2 FAST service by usage | |

| Pluto TV | ~80M global | 200+ live channels; pioneer of linear FAST model |

Market Share Among FAST Viewers

Among viewers who use FAST services specifically, the top three by share are Tubi (30%), The Roku Channel (25%), and Pluto TV (20%). Tubi distinguishes itself with a heavily on-demand model—over 95% of Tubi viewing is on-demand movies and TV shows, compared to other FAST platforms that lean toward linear channel programming. Over half of Tubi viewers are Gen Z or Millennials, and 67% are cord-cutters or cord-nevers.

Samsung TV Plus reported 88 million MAU in 2024, growing to surpass 100 million globally by January 2026, with Q1 2025 engagement surging over 30% year-over-year.

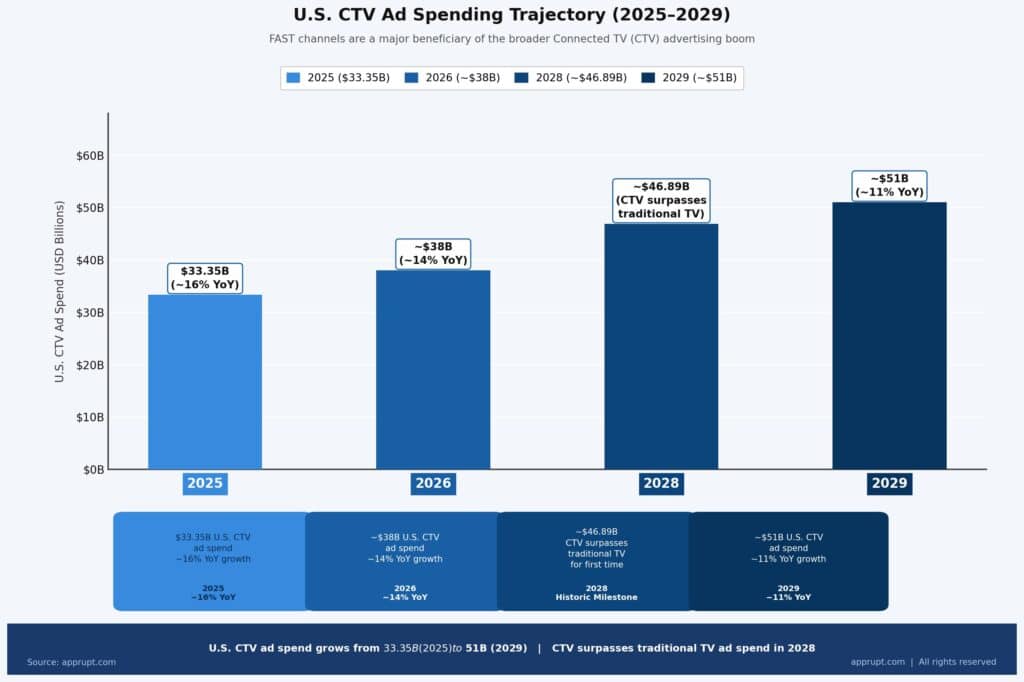

CTV Advertising & FAST Ad Economics

CTV Ad Spending Trajectory

FAST channels are a major beneficiary of the broader Connected TV (CTV) advertising boom:

| Year | U.S. CTV Ad Spend | Growth Rate | Source |

| 2025 | $33.35B | ~16% YoY | |

| 2026 | ~$38B | ~14% YoY | |

| 2028 | ~$46.89B | CTV surpasses traditional TV for first time | |

| 2029 | ~$51B | ~11% YoY |

By 2028, CTV ad spending is expected to surpass traditional TV ad spending for the first time in history. Linear TV has already fallen to just 12% of global ad spending, while CTV is on pace to exceed 40% of video ad spending by 2030.

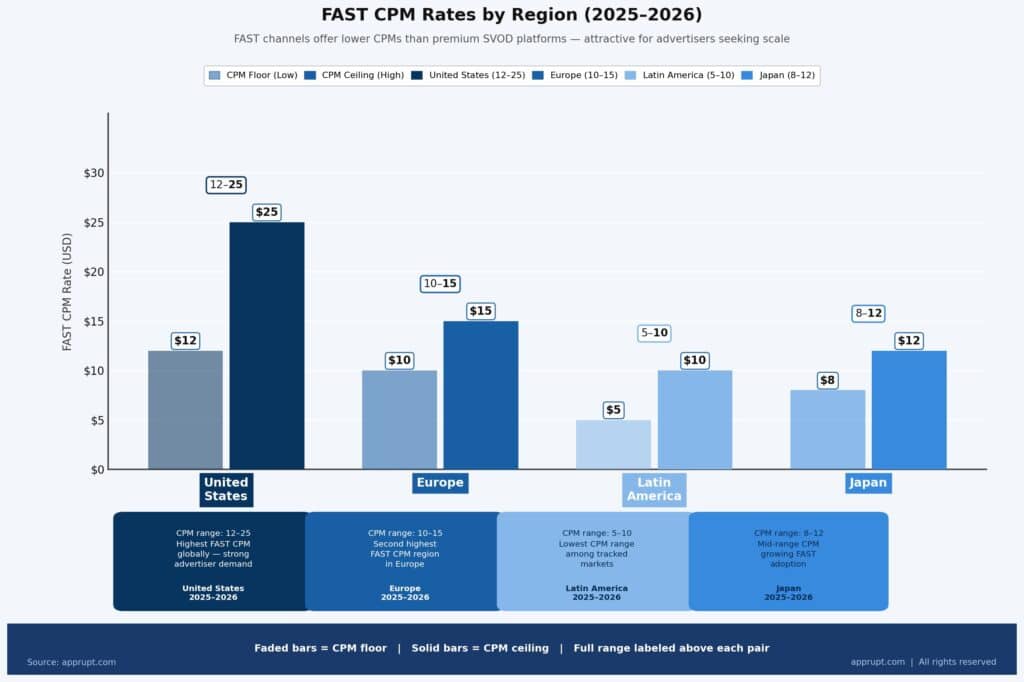

FAST CPM Rates (2025–2026)

FAST channels typically offer lower CPMs than premium SVOD platforms, making them attractive for advertisers seeking scale:

| Region | FAST CPM Range | Source |

| United States | $12–$25 | |

| Europe | $10–$15 | |

| Latin America | $5–$10 | |

| Japan | $8–$12 |

For comparison, premium CTV inventory on platforms like Netflix or Hulu commands CPMs of $40–$65. Most FAST channels run 8–12 minutes of ads per hour, lighter than cable TV’s typical 14–16 minutes.

Emerging Challenge: Inventory Oversupply

A growing concern in the FAST ecosystem is the risk of ad inventory oversupply. As major SVODs introduce ad tiers and FAST platforms proliferate, the volume of available ad slots has grown faster than advertiser demand, creating downward pressure on CPMs. Industry analysts warn that platforms pushing beyond 10 minutes of ads per hour risk seeing effective CPMs fall below $6.00, below the standard programmatic floor. This has prompted calls for platforms to cap ad loads at 6 minutes per hour and delist underperforming “zombie channels” to preserve pricing power.

Geographic Breakdown

United States

The U.S. remains the dominant FAST market, accounting for approximately 90% of global FAST revenue. By 2027, the U.S. FAST channel market alone is forecast to exceed $10 billion in revenue. Free streaming penetration exceeds 80% of households, and connected TVs dominate long-form viewing.

International Markets

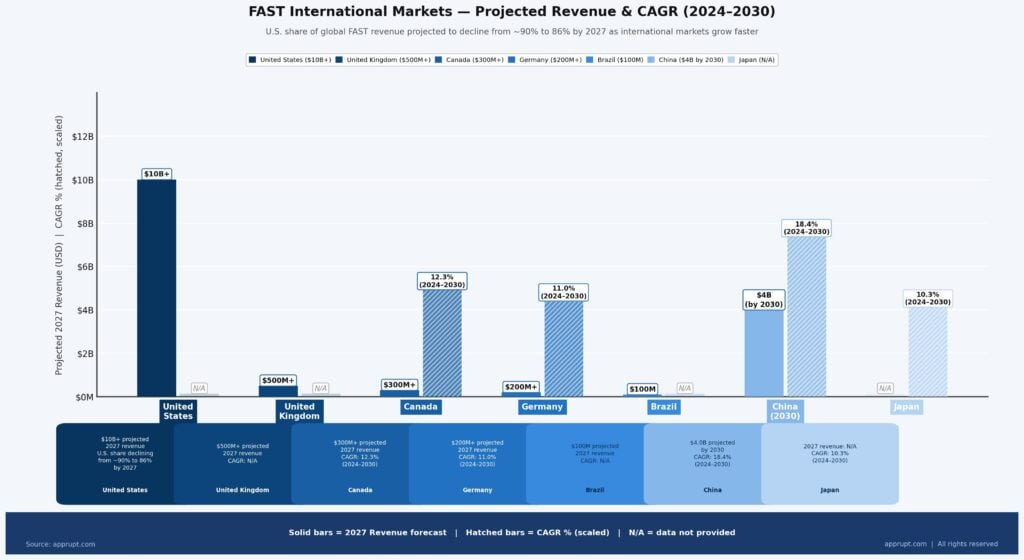

FAST is expanding rapidly beyond the U.S., with the U.S. share of global revenue projected to decline from ~90% to 86% by 2027 as international markets grow faster:

| Market | Projected 2027 Revenue | CAGR (2024–2030) | Source |

| United States | $10B+ | — | |

| United Kingdom | $500M+ | — | |

| Canada | $300M+ | 12.3% | |

| Germany | $200M+ | 11.0% | |

| Brazil | $100M | — | |

| China | $4.0B by 2030 | 18.4% | |

| Japan | — | 10.3% |

Asia-Pacific

Asia-Pacific is projected to be the fastest-growing FAST region. Premium AVOD revenues in Asia-Pacific are projected to grow from $8 billion in 2025 to over $12 billion by 2030, led by India, Japan, and Australia. India’s CTV user base has grown about 87% in recent years, with approximately 50 million CTV households as of mid-2025, expected to reach 60 million by year-end. India’s CTV ad spending is projected to grow from INR 2,000 crore ($240M) in 2025 to INR 3,500 crore ($420M) by 2027.

About 91% of the Indian population engages with advertisements while consuming content, signaling strong advertiser interest. Platforms like Samsung TV Plus host over 140 channels in India, and regional FAST services like Swastik Stories have already reached approximately 50 million viewers.

Key Trends Shaping 2026–2027 and Beyond

International and Regional Content

Demand for international content on FAST—particularly Korean dramas, Japanese anime, and Southeast Asian series—has surged. Korean TV series alone are estimated to have generated $8 billion in global streaming revenue between 2020 and 2024. This trend is expected to accelerate as platforms invest in multilingual and culturally localized programming.

Live Sports Migration

Live and near-live sports have become a cornerstone of FAST growth. Sports channels are up over 105% since mid-2024. A watershed moment came when Tubi simulcast Super Bowl LIX in February 2025—a first for any FAST platform. Despite this growth, sports still accounts for only about 2.6% of overall FAST viewing time, indicating significant room for expansion.

Local News Expansion

Local news is emerging as a key FAST category. In August 2025, an average of 61,000 viewers tuned into local stations via OTT, a 69% year-over-year increase. Currently, 25% of U.S. households have consumed news content on a FAST channel. Samsung TV Plus alone provides local news coverage across 114 U.S. markets.

AI-Driven Personalization

AI-powered content discovery and personalization are becoming standard across FAST platforms. As the channel count surpasses 1,900 globally, improving content discovery is seen as critical to sustaining viewer engagement and reducing churn. Advertising sophistication is also increasing, with AI-driven audience segmentation and measurement becoming table stakes by 2027.

Mobile-First Consumption in Emerging Markets

In Africa, South and Southeast Asia, and Latin America, mobile-first consumption is driving FAST adoption. Short-form and regional content strategies shape the OTT landscape in Asia, with increasing demand for bite-sized, mobile-friendly storytelling. In Latin America, mobile viewing dominates and consumers favor low-cost or bundled, ad-supported options.

Subscription Fatigue Tailwind

About 73.6% of total television viewing now involves ad-supported streaming models. As subscription prices rise across major SVOD platforms—Netflix, Disney+, and others have all raised prices recently—consumers are gravitating toward free alternatives. In 2025, ad-supported tiers accounted for 50% of subscriptions across major SVOD platforms. This subscription fatigue acts as a structural tailwind for FAST growth.

Challenges & Risks

Content Discovery

With nearly 2,000 channels available globally, content discovery remains a significant challenge. Very few FAST channels (and their content) are exclusive to any single platform—in contrast, across five global SVODs, 93% of content is exclusive to one provider. This lack of differentiation makes it harder for individual channels to build loyal audiences.

Ad Inventory Oversupply

The rapid expansion of FAST channels and SVOD ad tiers has created a surplus of ad inventory. If platforms do not manage supply carefully, effective CPMs could fall below sustainable levels. The industry consensus suggests that approximately 400 channels per platform represents a sustainable ceiling, beyond which advertising economics deteriorate.

Market Saturation Concerns

Some industry experts have noted potential signs of plateauing in new user acquisition during early 2025, although viewing hours among existing users continue to increase. The key question for 2026–2027 is whether FAST can continue to convert new viewers or whether growth becomes primarily engagement-driven among existing audiences.

Outlook: 2028 and Beyond

The long-term outlook for FAST remains strongly positive across all major forecasts. By 2028, CTV advertising is expected to surpass traditional TV for the first time, and FAST will be a primary beneficiary of this shift. The global FAST market is projected to reach $18.8 billion–$20.7 billion by 2030 and potentially $40 billion–$46.5 billion by 2033.

Key structural drivers supporting continued growth include:

- Cord-cutting acceleration: Traditional pay-TV subscriber losses continue to accelerate, funneling viewers to free streaming alternatives

- Smart TV penetration: Smart TVs with built-in FAST apps are now standard in most markets, lowering adoption barriers

- Advertiser demand shift: Advertisers are actively redirecting budgets from linear TV to CTV/FAST as measurement capabilities improve

- Global expansion: Non-U.S. markets represent a $1.6 billion+ revenue opportunity by 2027, with China, India, and Latin America as the highest-growth regions

- Content investment: Platforms are increasingly investing in originals (Tubi has 400+ originals) and premium live events to differentiate

The FAST sector is evolving from a repository for library content into a full-fledged entertainment platform with original programming, live sports, and interactive features—positioning it as a permanent fixture of the television landscape rather than a transitional format.