India’s over-the-top (OTT) streaming industry is one of the fastest-growing in the world, with total online video revenue projected to more than double from $4.31 billion in 2024 to $9.17 billion by 2030. The market crossed 100 million active subscribers by end-2025 and is on track to reach approximately 357 million SVOD subscriptions by 2030, positioning India to surpass China as the world’s largest SVOD subscription market. Advertising-supported video-on-demand (AVOD) remains the dominant monetization engine, expected to account for over 70% of incremental revenue growth through the decade, while subscription models continue to mature with a growing willingness among consumers to pay for premium, ad-free content.

Market Size & Revenue Forecasts

Total Market Revenue

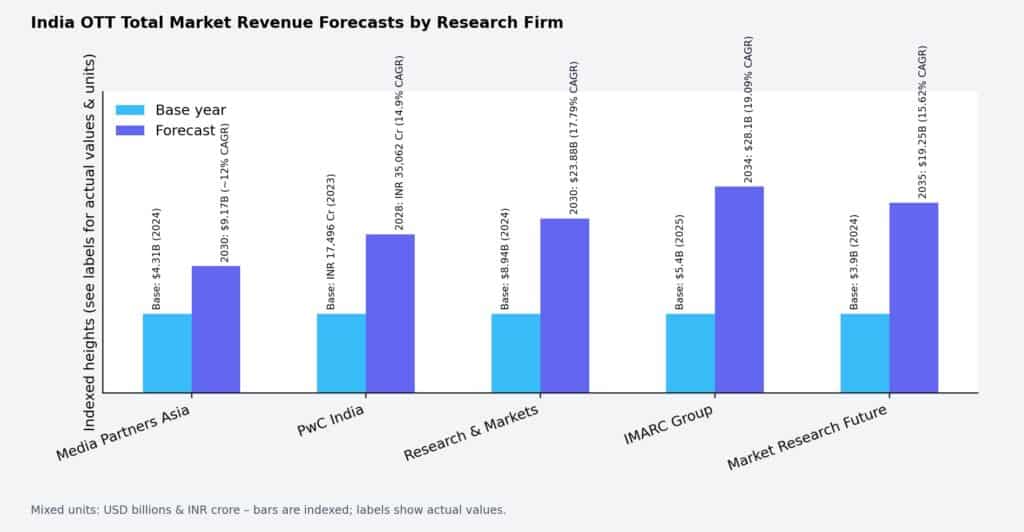

India’s digital video and OTT industry revenue stood at approximately $4.31 billion in 2024 and is forecast to reach $9.17 billion by 2030, growing at a compound annual rate of roughly 12%, according to Media Partners Asia (MPA). PwC’s Global Entertainment & Media Outlook (GEMO) pegs India’s OTT market at INR 17,496 crore ($2.1 billion) in 2023, projecting it to double to INR 35,062 crore ($4.25 billion) by 2028 at a 14.9% CAGR—the highest growth rate among the top 15 countries globally. The PwC GEMO 2025–2029 edition projects OTT revenue in India at $3.5 billion by 2029, with SVOD accounting for nearly 69% of the market.

Multiple research firms converge on a strong double-digit growth trajectory, though market size estimates vary due to differences in scope and methodology:

| Research Firm | Base Year Value | Forecast Value | Forecast Year | CAGR |

| Media Partners Asia | $4.31B (2024) | $9.17B | 2030 | ~12% |

| PwC India | INR 17,496 Cr (2023) | INR 35,062 Cr | 2028 | 14.9% |

| Research & Markets | $8.94B (2024) | $23.88B | 2030 | 17.79% |

| IMARC Group | $5.4B (2025) | $28.1B | 2034 | 19.09% |

| Market Research Future | $3.9B (2024) | $19.25B | 2035 | 15.62% |

SVOD vs. AVOD Revenue Breakdown

AVOD continues to dominate India’s OTT revenue mix, but SVOD is gaining ground. The SVOD segment crossed the $1 billion milestone in 2024 and is forecast to nearly reach $2.68 billion by 2030. AVOD revenue jumped from $1.03 billion in 2020 to $3.25 billion in 2024 and is expected to hit $6.48 billion by 2030. By the end of the decade, advertising-supported models will account for over 70% of total online video market revenue.

Industry projections for FY2025–26 place AVOD at approximately $3.5 billion and SVOD at $3.0 billion, with the revenue split moving closer to 55:45 (AVOD:SVOD) from the earlier ~70:30 ratio. OTT revenues for Indian broadcasters in FY26 are expected to grow 10–15% year-on-year, signaling a market that has moved beyond hyper-growth but continues to expand steadily.

Subscriber & User Growth

OTT Audience Universe

India’s OTT audience — defined as people who watched online videos at least once in the prior month — reached 601.2 million in 2025, representing a 9.9% year-on-year increase and 41% penetration of the total population. This figure is projected to reach 634.3 million users by 2029, with user penetration rising to 42.2%. As of 2024, an estimated 547.3 million Indians were OTT viewers, representing roughly 38% of the population.

SVOD Subscriptions

SVOD subscriptions in India have grown dramatically, from 52.6 million in 2020 to 135.6 million in 2024, and are projected to reach a staggering 357.4 million by 2030. The number of SVOD subscribing households is expected to grow from 39.3 million in 2024 to 75.7 million by 2030, meaning the average household will maintain approximately 4.7 simultaneous streaming subscriptions. Despite this massive scale, blended SVOD average revenue per user (ARPU) remains structurally low at approximately $0.5 per month — while SVOD ARPU ranges from $1.50 to $2.50/month and AVOD ARPU sits at only $0.15–$0.25/month, reflecting India’s high-volume, low-ARPU market characteristics.

India is expected to overtake China to become the world’s largest SVOD subscription market by 2030 with an estimated 358 million individual subscriptions. However, India’s combined premium VOD revenues from subscriptions and advertising will remain 4.5x smaller than China’s and 2.5x smaller than Japan’s.

Platform Landscape

Leading OTT Platforms by Subscribers (India, 2025)

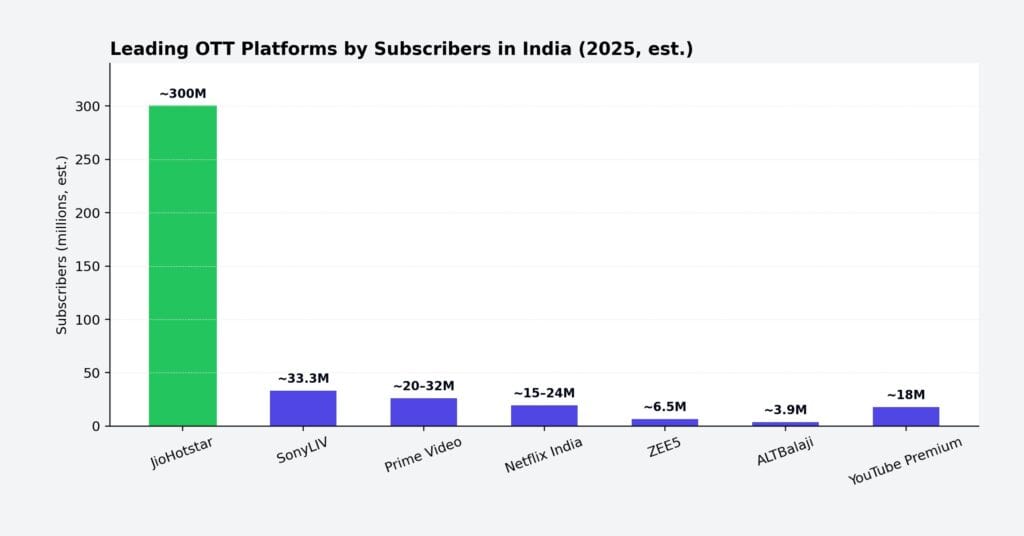

JioHotstar — formed in February 2025 by the merger of JioCinema and Disney+ Hotstar — has emerged as India’s dominant OTT platform. Driven largely by the 2025 IPL season, the platform surged from 50 million subscribers in February to 300 million by June 2025, with 503 million monthly users overall. The platform ranks second globally among OTT services, just behind Netflix’s 301.6 million worldwide subscribers.

| Platform | India Subscribers (Est.) |

| JioHotstar | ~300M |

| SonyLIV | ~33.3M |

| Amazon Prime Video | ~20–32M |

| Netflix India | ~15–24M |

| ZEE5 | ~6.5M |

| ALTBalaji | ~3.9M |

| At the revenue level, Netflix generates approximately $690 million from over 24 million Indian subscribers, while Amazon Prime Video has crossed $500 million from 32 million subscribers. JioHotstar, the largest by reach, projects revenues exceeding $1.1 billion with subscriptions surpassing 225 million (including paid tiers). YouTube Premium subscriptions are nearing 18 million in India, showing selective but growing willingness to pay for ad-free viewing. |

Key Growth Drivers

Mobile-First Consumption & Affordable Data

India’s OTT growth is fundamentally powered by mobile-first consumption and cheap data prices. With over 886 million internet users and mobile broadband penetration reaching nearly 69% in 2025, smartphones remain the primary streaming device. The country has approximately 700 million internet users with a penetration rate of about 50% as of late 2025. The GSMA projects 5G mobile connections in India to surpass 900 million by 2030, which will enable higher-quality video consumption and premium-tier adoption.

Regional Content Explosion

Regional language content has emerged as the primary growth driver for OTT platforms. In December 2025, ZEE5 reported that regional languages outside Hindi now account for more than 50% of India’s paid OTT subscriptions. Investments in regional content — in languages like Tamil, Telugu, Kannada, Bengali, and Malayalam — are expected to exceed INR 5,000 crore annually by 2028. The language barrier has been “completely broken” for Indian streaming audiences, with over 50% of viewership coming from non-Hindi content.

Connected TV (CTV) Growth

CTV penetration experienced 85% growth in 2025, with over 129 million users across 45 million households. CTV is fast becoming the preferred streaming device after smartphones, with 21% of India’s 601.2 million OTT audiences now using CTV to stream videos, up from 13% in 2024. Over 55% of CTV viewers come from towns with less than one million population, signaling significant adoption in smaller cities and rural areas. Addressable advertising on CTV in India is expected to exceed 16% of total TV ad revenues by 2026.

Revenue Mix Shift: AVOD vs. SVOD

The Indian OTT market is witnessing a significant shift in monetization strategy. For years, AVOD dominated with nearly 70% of revenue, but the split is progressively moving toward a more balanced mix. The industry is shifting toward a “premiumization” strategy where high-quality content, exclusive sports, and ad-free viewing drive revenue growth over basic ad-supported tiers.

Key monetization trends:

- Advertising dominance: OTT and digital video advertising revenues have climbed to approximately $6.5 billion, growing at close to 12% annually. YouTube alone is projected to grow from $1.84 billion in 2024 to over $3.05 billion by 2030 in India advertising revenues.

- Digital advertising growth: Overall digital advertising in India is expected to expand from $11.1 billion in 2024 to nearly $22 billion by 2030.

- Hybrid models rising: Platforms increasingly experiment with subscription, ad-supported, and hybrid approaches. Amazon Prime Video in India turned its entry-level offering into an AVOD service in June 2025. Netflix expects its global ad revenue to “roughly double” in 2025.

- Bundled subscriptions: Telecom bundling remains a key distribution strategy, with JioHotstar leveraging deep integration with Reliance Jio’s mobile subscriber base.

Industry Outlook: 2026 and Beyond

2026: Maturation Phase

Heading into 2026, the Indian OTT industry appears more mature and realistic. Growth will continue but will be measured, with OTT revenues for broadcasters expected to grow 10–15% year-on-year in FY26. The OTT video market size is estimated to reach $7 billion by 2027. Content investments are becoming more disciplined and IP-led, with sharper focus on scalable storytelling rather than sheer volume.

2028–2030: Scaling Phase

By 2028, PwC projects India’s OTT market to reach INR 35,062 crore ($4.25 billion) with SVOD accounting for 65% of the market and AVOD growing at a 26% CAGR to reach INR 11,097 crore. The number of video OTT subscriptions is projected to grow from 10.1 crore in 2023 to 16.9 crore by 2028 at a 10.8% CAGR.

By 2030, the total online video industry will have more than doubled to $9.17 billion, with India expected to become the world’s largest SVOD subscription market. Key trends shaping this period include:

- Format innovation: Micro-dramas and short-form content are gaining traction alongside traditional long-form programming.

- AI integration: AI-enabled efficiency across the content value chain, from production to personalized recommendations, is becoming a differentiator.

- Sports-led growth: Live sports, particularly cricket (IPL), remain the primary subscriber acquisition tool, with digital viewership now exceeding television.

- Market consolidation: With approximately 57 active OTT platforms, the market is expected to undergo significant consolidation and alliance formation focused on sustainable growth.

Beyond 2030

Longer-term projections indicate sustained growth. IMARC Group projects the India OTT market at $28.1 billion by 2034 at a 19.09% CAGR, while Market Research Future forecasts $19.25 billion by 2035 at a 15.62% CAGR. The Indian OTT ecosystem, which crossed 100 million active subscribers by end-2025, has the potential to reach nearly 250 million by 2030, with traditional television facing long-term structural erosion as value shifts decisively toward streaming, social platforms, and CTV-led monetization.

Key Statistics Summary

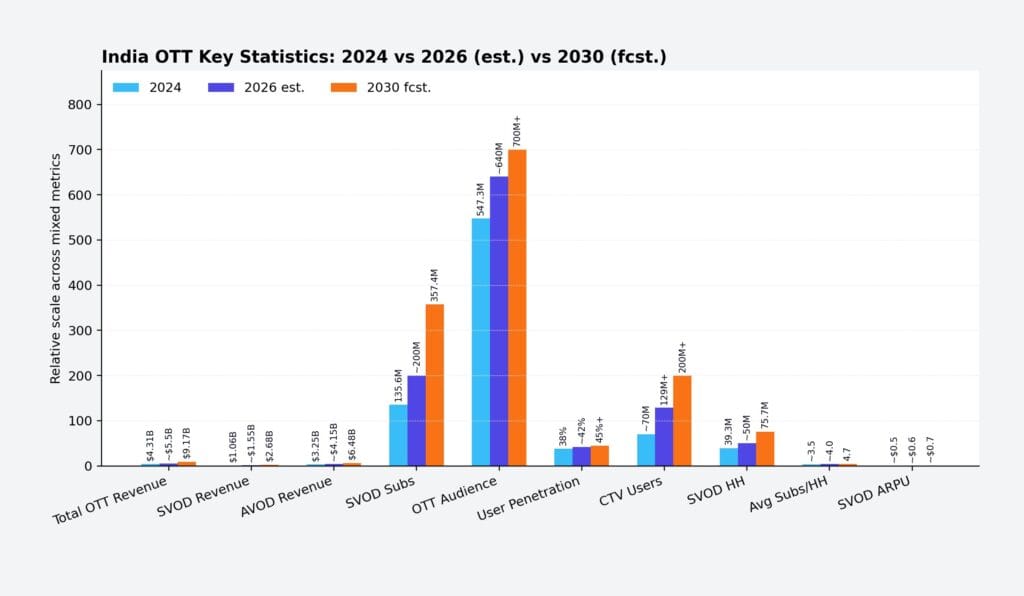

| Metric | 2024 (Actual) | 2026 (Est.) | 2030 (Forecast) |

| Total OTT Revenue | $4.31B | ~$5.5B (est.) | $9.17B |

| SVOD Revenue | $1.06B | ~$1.55B (est.) | $2.68B |

| AVOD Revenue | $3.25B | ~$4.15B (est.) | $6.48B |

| SVOD Subscriptions | 135.6M | ~200M (est.) | 357.4M |

| OTT Audience | 547.3M | ~640M (est.) | 700M+ (est.) |

| OTT User Penetration | 38% | ~42% | 45%+ (est.) |

| CTV Users | ~70M (est.) | 129M+ | 200M+ (est.) |

| SVOD Households | 39.3M | ~50M (est.) | 75.7M |

| Avg. Subs per Household | ~3.5 (est.) | ~4.0 (est.) | 4.7 |

| SVOD ARPU (monthly) | ~$0.5 | ~$0.6 (est.) | ~$0.7 (est.) |