The blockchain, also known as distributed ledger technology, is the talk of the town at the moment. While still commonly associated with cryptocurrency trading, the technology is increasingly recognized for its potential across numerous industries and business sectors for its ability to do more than just let you buy Bitcoin.

In fact, the system could contribute to safe, fair, and transparent development. Analysts estimate that blockchain is set to go far beyond its cryptocurrency roots and affect almost every single production and manufacturing area.

Apart from finance and banking services, the most prominent examples are all the areas that require strict record-keeping, such as healthcare. Supply chains are commonly understood to be the backbone of any well-functioning enterprise.

The decentralized ledger equips the supply chain with the ability to ensure real-time visibility and track goods from manufacture to the distribution end. This increases the trust the involved parties need to keep the procedures moving while minimizing the risk of undesirable situations such as counterfeits or fraudulent events.

The beginnings

American computer scientist and cryptographer David Chaum first proposed a network reminiscent of the blockchain as part of his 1982 dissertation. Later, Stuart Haber and W. Scott Stornetta continued the work by describing the possibility of a network that works by securing a chain of blocks.

The main advantage of this network would have been that once the information entered the system, it couldn’t be altered or tampered with in any way. The blockchain has kept in line with this, and it’s why the technology is currently believed to be so reliable.

A year after the creation of this concept, Merkle trees were added to the design as a means of improving efficiency. Several certificates could also be gathered into a single block through the use of this system.

Also known as a hash tree, this data structure has each “leaf” representing a node and is labeled with a cryptographic hash. The Merkle tree permits the secure verification of the content available in large data structures.

The first blockchain to be directly conceptualized by an individual or a group was created by Satoshi Nakamoto in 2008. The identity of this person remains unknown, although the internet is rife with speculation. Some even wonder if it’s just one person or a group. Nakamoto is now best known as the developer of Bitcoin, as well as the currency’s white paper and original reference implementation.

Since then, the views towards the blockchain have changed, and many now believe the system can be implemented across a wide area in different business sectors.

How it works

When it comes to storing and managing information at a company level, spreadsheets and databases are the most common methods.

The blockchain is somewhat similar, with the primary difference being how the data is accessed and structured within the system. The decentralized ledger uses programs known as scripts that carry out the tasks and procedures traditionally associated with databases.

Since the system is entirely distributed, multiple copies of the same information are saved on different machines. All copies must match perfectly for the data to be considered valid. This way, it is much easier to maintain transparency when using the blockchain compared to the classic systems. Keeping records is more straightforward, as is creating and fostering trustworthiness at

The blockchain collects all the information resulting from transactions and deposits it into a block. This data structure is closed once the network validates the information. Afterwards, a new block is created, data is added, and it is then closed upon completion.

The records are permanent and, once written, cannot be altered or removed. A hacker attack is virtually impossible this way since the cybercriminal would have to control more than 50% of the mining hash rate. Being in direct possession of 51% of the nodes could, at least theoretically, give you the ability to alter the blockchain.

However, this is impossible in the case of the Bitcoin blockchain, as altering the historical blocks isn’t feasible.

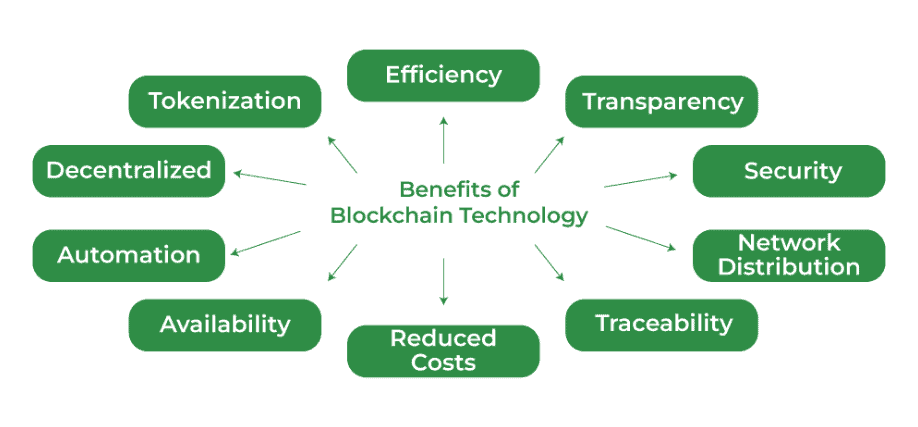

The advantages

Depending on the platform, transactions must undergo different processes to achieve completion.

For instance, in the case of the BTC blockchain, your undertaking will reach a memory pool, where it automatically enters a queue. You must then wait for a validator to get to it. It is then entered into a block, and once that structure fills with an average of 2,000 transactions, the valid block is verified and sealed.

While other blockchains use different systems, which tend to be faster and perhaps less energy-intensive, Bitcoin’s main advantage is that it is much safer. This has made it the preferred digital currency among institutional and retail investors.

All transactions can be viewed transparently due to the decentralized quality of the blockchain. Therefore, if you want to track the direction of a payment, you can do so easily.

Hackers will naturally choose to remain anonymous, but the extracted coins are traceable because the wallet addresses are directly published on the blockchain. All records are, of course, encrypted, so only an individual assigned an address can reveal their identity. This is the best way to blend transparency with anonymity.

The industries

There are several sectors that could benefit directly from blockchain implementation within their own systems. Among them are:

- Law enforcement: Using the blockchain can protect evidence from being tampered with, including videos. With the rise of deepfake software, this is becoming a growing concern.

- Supply chains: Even in the case of small enterprises, supply chains can be quite large. Tracing all the data is difficult, but the blockchain can ease the process.

- Identity management: With the rise of data breaches, identity theft has also become more common. The blockchain guarantees that no third party can access sensitive information and use it for their personal gain.

- Apps: Messaging applications are one of the favorite destinations for hackers looking to extract data. With the help of the blockchain, there’s no need to provide any personal information anyway. You can just sign up with your wallet address.

Technology is becoming increasingly crucial for daily life, and new additions like the blockchain are bound to change the economic landscape.