The U.S. cable TV industry is in structural decline, with no realistic prospect of recovery. As of 2025, approximately 66.1 million U.S. households subscribe to cable TV — down 37% from the 105 million peak in 2010. Pay TV penetration has dropped below 50% for the first time in history, meaning fewer than half of American households now pay for any form of traditional television service. The major cable operators — Comcast, Charter, and Dish — collectively lost over 2.1 million TV subscribers in 2025 alone. By 2027, total U.S. pay TV subscribers are forecast to fall to approximately 60 million, and by 2028, only 32% of homes will have a traditional pay TV service. The industry is responding with mega-mergers (Charter-Cox for $34.5 billion), cable network spinoffs (Comcast’s Versant), and a strategic pivot from video to broadband and wireless as the primary revenue drivers.

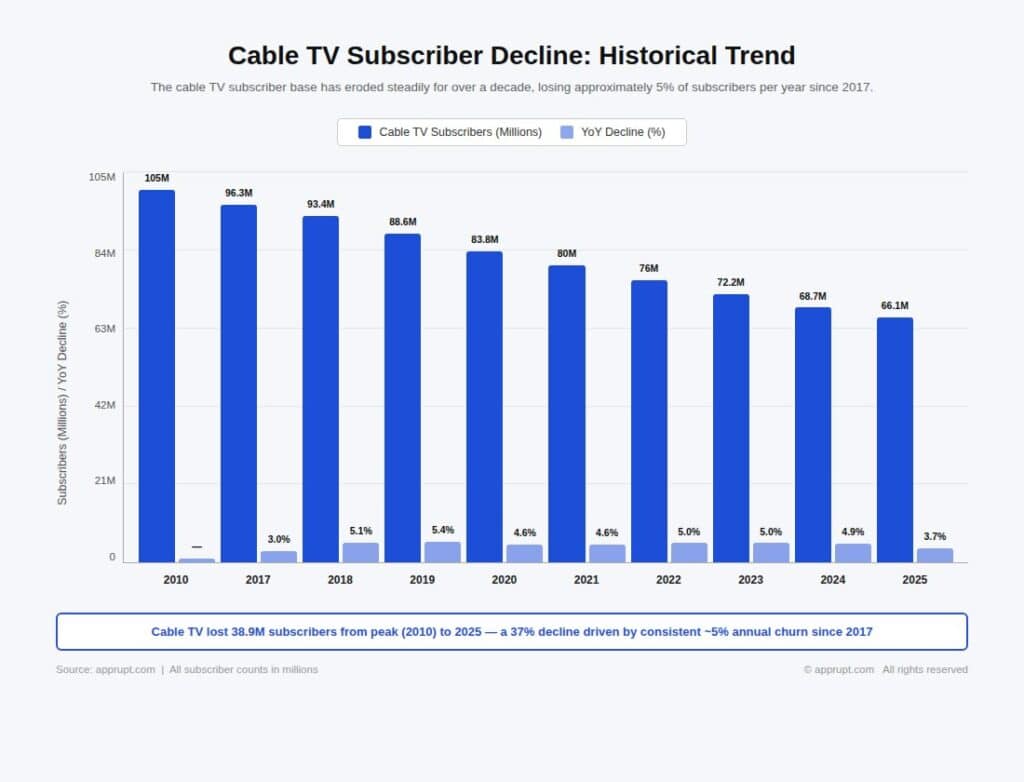

Cable TV Subscriber Decline: Historical Trend

The cable TV subscriber base has eroded steadily for over a decade, losing approximately 5% of subscribers per year since 2017.

| Year | Cable TV Subscribers | YoY Decline |

| 2010 | 105 million | — |

| 2017 | 96.3 million | 3.0% |

| 2018 | 93.4 million | 5.1% |

| 2019 | 88.6 million | 5.4% |

| 2020 | 83.8 million | 4.6% |

| 2021 | 80 million | 4.6% |

| 2022 | 76 million | 5.0% |

| 2023 | 72.2 million | 5.0% |

| 2024 | 68.7 million | 4.9% |

| 2025 | 66.1 million | 3.7% |

Source: IBISWorld / Evoca TV

Since 2012, U.S. pay TV providers have shed roughly 25 million subscribers. The slight deceleration in 2025 (3.7% decline vs. ~5% average) is driven partly by bundling strategies — particularly Charter’s inclusion of streaming services in its cable packages — and partly by vMVPD substitution masking the true cable decline.

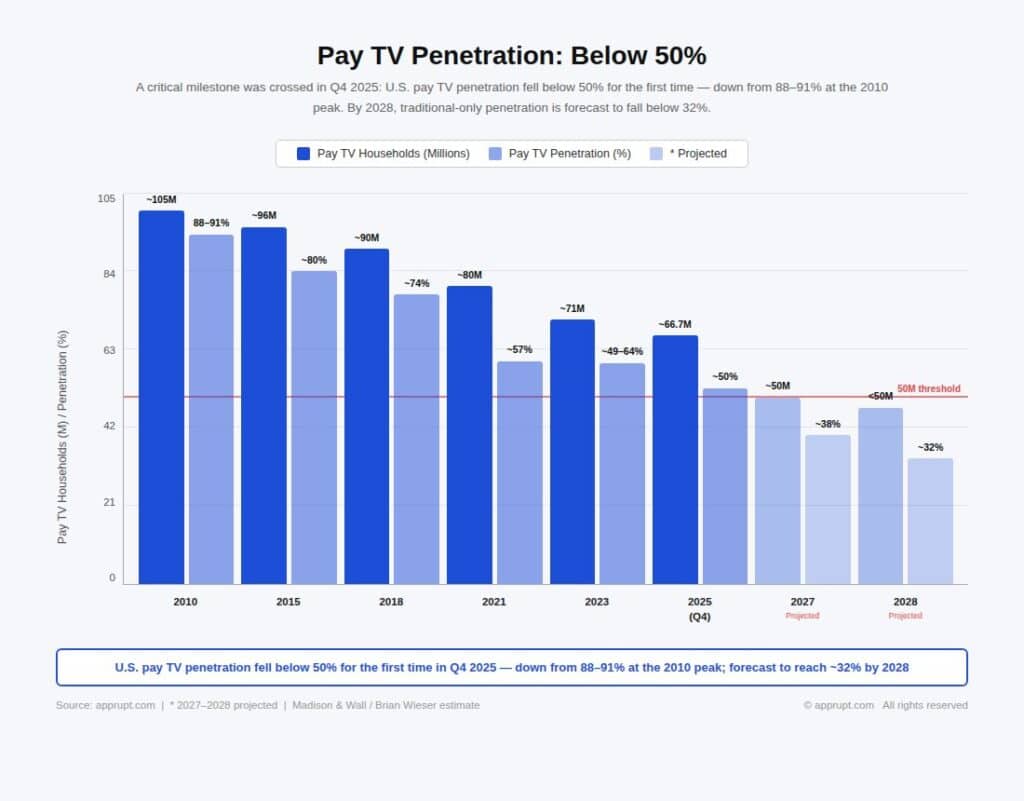

Pay TV Penetration: Below 50%

A critical symbolic milestone was crossed in Q4 2025: U.S. pay TV penetration fell below 50% for the first time. Madison & Wall’s Brian Wieser estimated 66.7 million pay TV households in Q4 2025, representing roughly 50% of the 133 million U.S. TV households — down from nearly 80% penetration in Q1 2018 and 88% at the 2010 peak.

| Year | Pay TV Penetration | Pay TV Households |

| 2010 | 88–91% | ~105 million |

| 2015 | ~80% | ~96 million |

| 2018 | ~74% | ~90 million |

| 2021 | ~57% | ~80 million |

| 2023 | ~49% (traditional); 64% (incl. vMVPDs) | ~71 million |

| 2025 (Q4) | ~50% (all pay TV) | ~66.7 million |

| 2027* | ~38% | ~50 million |

| 2028* | ~32% (traditional only) | <50 million |

Sources: Madison & Wall, PwC, GlobalData

This steady decline has enormous implications for advertisers. As Wieser noted, “Linear TV can still deliver high levels of reach and retains an outsized share of inventory, but higher levels of audience reach can be found elsewhere” — pointing to streaming, digital video, and social video platforms.

Major Operator Subscriber Losses (2025)

The four largest traditional pay TV providers all reported continued subscriber erosion throughout 2025.

Comcast (Xfinity)

Comcast lost 1.25 million video subscribers in 2025, ending the year with 11.3 million — down from 12.5 million at the end of 2024 and 14.1 million in 2023. In Q1 2025 alone, Comcast shed 427,000 TV subscribers — the steepest quarterly decline among all operators. Comcast’s video subscriber base has declined by nearly 40% since 2019. In a strategic pivot, Comcast completed the spinoff of its cable networks (CNBC, USA Network, MSNBC NOW, E!, Oxygen, SYFY, Golf Channel) into a new standalone public company, Versant Media Group, which began trading on Nasdaq on January 5, 2026. Versant generates approximately $7 billion in annual revenue but saw its stock drop 13% on its first day of trading, reflecting investor skepticism about the future of cable networks.

Charter Communications (Spectrum)

Charter lost 255,000 pay TV subscribers in 2025, ending the year with 12.07 million — a significant improvement from losses of 1.2 million in 2024 and 1 million in 2023. Notably, Charter added 49,000 residential video subscribers in Q4 2025 — its first positive quarter since 2020, driven by its strategy of bundling ad-supported streaming services (Disney+, Peacock, HBO Max) into Spectrum TV packages.

Dish Network / EchoStar

EchoStar (Dish’s parent) ended 2025 with 7.00 million total pay TV subscribers: 5.02 million on Dish TV satellite and 1.98 million on Sling TV. Dish TV lost 636,000 subscribers during 2025 (improved from 785,000 in 2024), while Sling TV lost 167,000 subscribers — a reversal from a gain of 37,000 in 2024. EchoStar reported a staggering full-year net loss of $14.5 billion in 2025, driven largely by non-cash asset impairment charges.

DirecTV

DirecTV lost approximately 288,000 subscribers in Q3 2025 alone. For the full year, the company continued its multi-year decline, with total U.S. subscribers estimated to have dropped well below 10 million. DirecTV had 11.3 million subscribers at the end of 2023, down from a peak of 20.3 million in 2014. In response, DirecTV has begun reducing satellite service availability in certain regions and pivoting toward streaming offerings.

Altice USA (Optimum)

Altice USA, rebranded to Optimum in late 2025, reported Q3 2025 video subscribers of just 1.67 million — down 14% year-over-year. The company lost 61,000 video subscribers in Q3 alone, with video revenue declining 9.8% to $645 million. Altice also lost 68,000 TV customers in Q1 2025. Total revenue fell 5.4% year-over-year, and the company recorded a net loss of $1.63 billion in Q3 driven by impairment charges on cable franchise rights.

Combined Q1 2025 Losses

In Q1 2025 alone, the four largest traditional operators lost over 1 million TV subscribers combined:

| Operator | Q1 2025 TV Subscriber Losses |

| Comcast | −427,000 |

| Dish Network | −383,000 |

| Charter (Spectrum) | −181,000 |

| Altice USA | −68,000 |

| Total | −1,059,000 |

This translates to more than 11,700 households canceling cable or satellite service every single day.

Revenue Decline

Cable TV’s revenue trajectory mirrors its subscriber losses. Pay TV revenue peaked at approximately $101 billion in 2014 and has been declining steadily since.

| Metric | Value | Year |

| Peak pay TV revenue | $101 billion | 2014 |

| Pay TV subscription revenue | ~$73 billion | 2023 |

| Pay TV subscription revenue (forecast) | ~$54 billion | 2027 |

| Total decline from peak | −$47 billion | 2014 → 2027 |

Advertising Revenue Collapse

Linear TV advertising is declining even faster than subscriptions. MoffettNathanson projects linear TV ad revenues (local TV, broadcast networks, and cable networks) fell 7% in 2025, with further declines of 6% forecast for 2026 and 8% for 2027.

| Advertising Segment | 2024 Revenue | 2025 Revenue | Change |

| Cable network ads | $22.5 billion | $20.2 billion | −10.2% |

| Broadcast network ads | $12.7 billion | $11.7 billion | −7.9% |

| Local TV ads | $21.6 billion | $16.9 billion | −21.8% |

The steep 21.8% drop in local TV advertising reflects the loss of political ad spending from the 2024 election cycle. However, ad-supported connected TV (CTV) continues to grow, projected to rise from $16 billion in 2025 to $22 billion in 2027, a 16% annual increase.

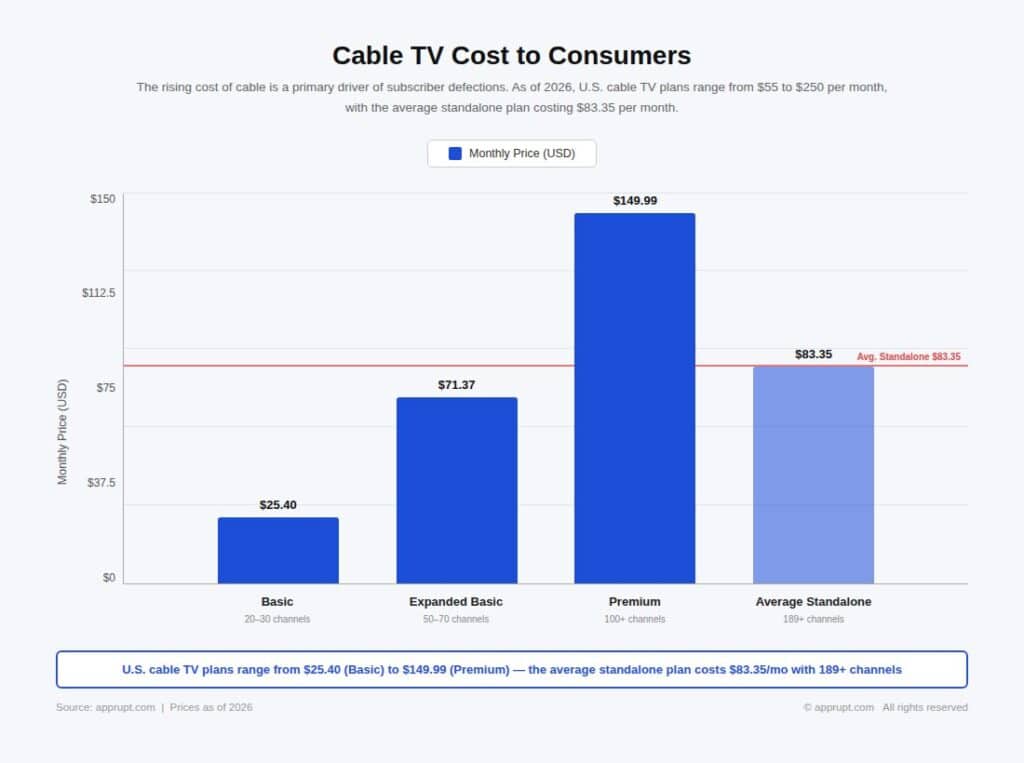

Cable TV Cost to Consumers

The rising cost of cable is a primary driver of subscriber defections. As of 2026, U.S. cable TV plans range from $55 to $250 per month, with the average standalone plan costing $83.35 per month.

| Cable Service Type | Monthly Price | Channels |

| Basic | $25.40 | 20–30 |

| Expanded Basic | $71.37 | 50–70 |

| Premium | $149.99 | 100+ |

| Average Standalone | $83.35 | 189+ |

By comparison, the average cord-cutter pays approximately $48 per month for about three streaming services — nearly 42% less than the average cable bill. An All About Cookies survey found that 95% of cord-cutters are satisfied with their decision, and only 5% regret switching.

The Charter-Cox Mega-Merger

The most significant structural response to the cable decline is the $34.5 billion merger between Charter Communications and Cox Communications, announced in May 2025 and approved by the FCC in February 2026.

Deal Structure

- Valuation: $34.5 billion ($21.9 billion equity + $12.6 billion net debt)

- Combined entity: Largest U.S. cable operator with 69.5 million locations passed, 37.6 million total customers, and over 100,000 employees

- Revenue: $68.2 billion combined (fiscal 2024: $55.1B Charter + $13.1B Cox)

- Ownership: Cox Enterprises receives 23% of fully diluted shares + $4 billion cash

- Branding: Combined company will operate under the Cox Communications name, with Spectrum as the consumer-facing brand

The merger creates a company that surpasses Comcast (63.96 million homes passed) in footprint. Charter CEO Chris Winfrey emphasized that the deal’s primary value lies in broadband and wireless connectivity — not video — noting the combined network will span 46 states and 78 million homes.

Strategic Rationale

The merger is fundamentally a scale play designed to:

- Reduce per-subscriber costs for infrastructure upgrades (DOCSIS 4.0, fiber expansion)

- Compete more effectively against fixed wireless and fiber overbuilders

- Grow the wireless subscriber base (Charter’s Spectrum Mobile has been its fastest-growing segment)

- Leverage combined negotiating power with content providers to slow programming cost inflation

Video subscribers are no longer the deal’s strategic centerpiece. Both companies are pivoting toward broadband and mobile as primary revenue drivers, with video positioned as an add-on bundling tool rather than a standalone profit center.

Comcast’s Versant Spinoff

Comcast completed the separation of its legacy cable TV networks into Versant Media Group on January 2, 2026. This move explicitly acknowledges that cable networks are a declining business that was dragging down the valuation of Comcast’s more promising assets (NBC, Telemundo, Peacock streaming, Universal Studios theme parks).

What Versant Includes

- Cable networks: CNBC, MSNBC NOW, USA Network, E!, Oxygen, SYFY, Golf Channel

- Digital platforms: Fandango, Rotten Tomatoes, GolfNow, GolfPass, SportsEngine

- Revenue: ~$7 billion annually

- Viewership: 14 billion hours of content consumption in 2024; ~65 million households tuning in monthly

- Retained by NBCU: Bravo (strong Peacock content pipeline)

- Stock: Trades on Nasdaq as VSNT; closed down 13% on first trading day at $40.57/share

Versant’s first standalone earnings report (Q4 2025) showed an 8.9% drop in advertising revenue year-over-year. Reuters noted investor skepticism, with analyst Ross Benes of eMarketer stating: “Traditional TV networks continue to produce steady revenue, yet their future prospects appear grim. It’s hard to generate enthusiasm among investors for businesses whose peak performance is behind them”.

Who Still Watches Cable TV?

Despite the exodus, approximately 30% of Americans still watch TV through traditional cable or satellite services. The demographic profile of remaining cable subscribers skews older and more habitual:

- Baby Boomers: 40% still use traditional cable/satellite — the highest of any generation

- Gen Z: Only 21% use cable/satellite

- Primary reasons for keeping cable: Live sports, local news, familiarity, bundled internet discounts

- Average cable subscriber: Over 55 years old, often in a bundle with broadband

The “cord-never” generation — consumers under 32 who have never subscribed to cable — represents a permanent, irreversible loss for the industry. As this demographic ages into primary spending years, the traditional cable subscriber base will continue its structural decline regardless of pricing or content strategies.

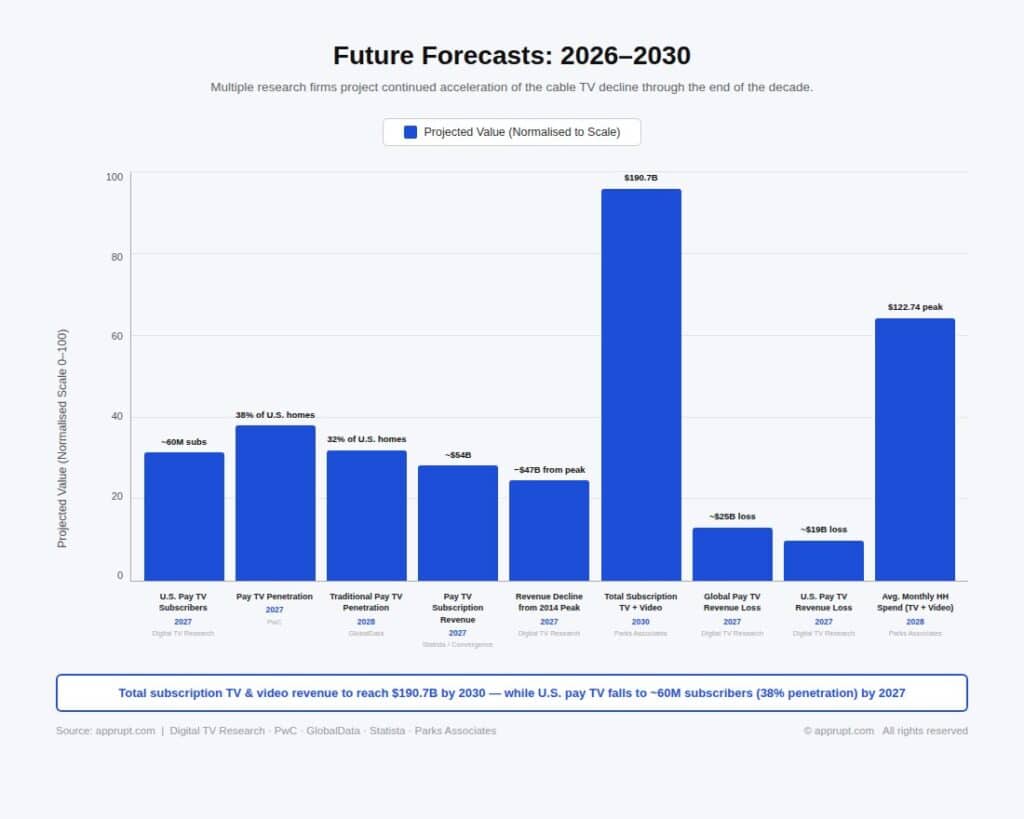

Future Forecasts: 2026–2030

Multiple research firms project continued acceleration of the cable TV decline through the end of the decade.

| Metric | Projection | Year | Source |

| U.S. pay TV subscribers | ~60 million | 2027 | Digital TV Research |

| Pay TV penetration | 38% of U.S. homes | 2027 | PwC |

| Traditional pay TV penetration | 32% of U.S. homes | 2028 | GlobalData |

| Pay TV subscription revenue | ~$54 billion | 2027 | Statista/Convergence |

| Revenue decline from 2014 peak | −$47 billion | 2027 | Digital TV Research |

| Total subscription TV + video revenue | $190.7 billion | 2030 | Parks Associates |

| Global pay TV revenue loss | −$25 billion (vs. 2021) | 2027 | Digital TV Research |

| U.S. pay TV revenue loss | −$19 billion (vs. 2021) | 2027 | Digital TV Research |

| Average monthly household spend (TV + video) | $122.74 (peak) | 2028 | Parks Associates |

Parks Associates forecasts total U.S. subscription TV and video revenue (cable + streaming combined) will grow modestly from $186.5 billion in 2025 to $190.7 billion by 2030. However, virtually all growth comes from streaming services, while traditional pay TV revenue continues to contract. As Parks’ Michael Goodman noted: “Growth is no longer about adding new households — it’s about optimizing value. Consumers are stacking more services, gravitating toward ad-supported tiers, and demanding more flexibility”.

S&P Global’s Network-Level Forecast

S&P Global Market Intelligence projects the average U.S. cable network will lose subscribers at a 5.4% annual rate from 2025 through 2029. Widely distributed networks like C-SPAN and Food Network are expected to lose 15–20 million subscribers by 2029, as cable bundles shrink and operators drop less-watched channels to reduce programming costs.

The Pivot: From Video to Connectivity

The cable industry’s future lies not in video but in broadband internet and wireless services. This strategic pivot is already well underway across all major operators.

Broadband as the Core Business

Even as cable companies hemorrhage video subscribers, their broadband businesses remain large — though increasingly pressured by fiber and fixed wireless competition. Charter’s combined company (with Cox) will have 37.6 million broadband customers across 69.5 million homes passed. Comcast still serves approximately 30 million broadband subscribers.

However, broadband is no longer immune to competitive pressure. Comcast lost 199,000 broadband subscribers in Q1 2025, while Charter lost 60,000. Fixed wireless services from T-Mobile and Verizon added nearly 1 million new subscribers in Q2 2025 alone.

Wireless Growth

Wireless has emerged as the brightest spot for cable operators. Comcast’s Xfinity Mobile added 1.5 million net wireless lines in 2025, reaching 9.3 million total wireless customers — a 19% increase. Charter’s Spectrum Mobile has similarly been growing rapidly. EchoStar ended 2025 with 7.51 million retail wireless subscribers. This trend will likely accelerate as the Charter-Cox combination creates a wireless platform spanning 46 states.

Conclusion

The U.S. cable TV industry is in an irreversible decline that will halve its subscriber base from peak to under 50 million by 2028. No amount of bundling, price adjustments, or content deals can reverse a structural shift driven by generational change, streaming economics, and technological disruption. The cable companies that survive will do so not as video distributors but as connectivity providers — delivering broadband internet and wireless services to the same homes that once relied on them for television. The Charter-Cox merger, Comcast’s Versant spinoff, and the industry-wide pivot to wireless represent explicit admissions that the cable TV era, as a standalone business model, is ending. What remains is a legacy subscriber base that will continue to shrink by 5–7% per year, generating diminishing but still meaningful revenue for operators wise enough to treat video as a retention tool rather than a growth engine.