The Asia-Pacific region is the fastest-growing frontier for Free Ad-Supported Streaming TV (FAST), driven by rapid CTV adoption, massive population bases, and ad-supported viewing cultures that naturally align with the FAST model.

The APAC FAST market is projected to grow at a 15.2–16.5% CAGR through 2030–2033, potentially reaching $38.77 billion by 2033. India leads the charge with 129.2 million CTV users (85% YoY growth) and CTV ad spending racing toward ₹8,000 crore ($1B) by 2026. South Korea is emerging as Asia’s next FAST powerhouse, with revenues projected to double from $23 million (2024) to $48 million by 2030.

Meanwhile, Samsung TV Plus has grown its Southeast Asian channel catalog six-fold in its first year, reaching 230+ channels across Singapore, the Philippines, and Thailand. The infrastructure enabling this growth is increasingly Indian-built: Amagi Media Labs, the Bangalore-based FAST technology unicorn, listed on Indian stock exchanges in January 2026 after recording ₹1,162 crore ($137M) in FY2025 revenue.

APAC FAST Market Overview

Market Size & Forecast

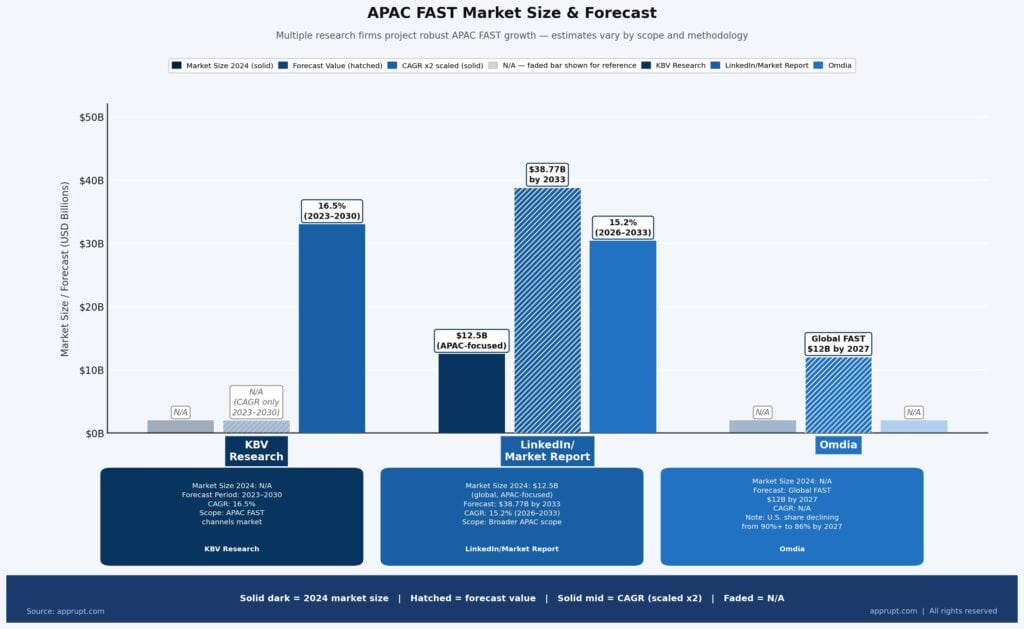

Multiple research firms project robust growth for the APAC FAST market, though estimates vary depending on scope and methodology:

| Research Firm | Market Size (2024) | Forecast | CAGR | Notes |

| KBV Research | — | 2023–2030 | 16.5% | APAC FAST channels market |

| LinkedIn/Market Report | $12.5B (global, APAC-focused) | $38.77B by 2033 | 15.2% (2026–2033) | Broader APAC scope |

| Omdia | — | Global FAST $12B by 2027 | — | U.S. share declining from 90%+ to 86% by 2027 |

The APAC region is the fastest-growing market globally for FAST, fueled by large population bases, rapid urbanization, and government initiatives supporting digital modernization. The key structural drivers include the proliferation of connected devices (smart TVs, streaming boxes, mobile devices), accessibility of high-quality content from established networks, improvements in ad targeting and personalization, and the accelerating cord-cutting trend.

APAC FAST Hierarchy

Omdia’s research positions the top APAC FAST markets in the following order by revenue:

- Australia — Largest APAC FAST market; projected to exceed $480 million by 2027

- Japan — Second largest; FAST revenue projected at $297.43 million in 2025; premium streaming sector hit $7.2B total in 2025

- South Korea — Third largest APAC FAST market; revenues to double from $23M to $48M by 2030

- India — Rapidly emerging; CTV ad market the fastest-growing segment

- Southeast Asia — Early-stage but accelerating, particularly in the Philippines, Indonesia, and Thailand

India: The Breakout FAST Market

CTV Audience Explosion

India’s CTV ecosystem experienced a transformative year in 2025. The key metrics paint a picture of a market crossing critical mass:

- 129.2 million active CTV users as of 2025, an 85% year-over-year surge from 2024

- 60–70 million CTV households, adding over 35 million new viewers in 2025 alone

- 21% of India’s 601.2 million OTT audiences now use CTV to stream, up from 13% in 2024

- CTV has overtaken laptops and tablets to become the #2 device for streaming in India, behind smartphones

- 55%+ of CTV viewers belong to villages and towns with populations under one million, signaling Tier 2/3 penetration

- Indian viewers spend over 3.5 hours daily on TV, with 80% of viewing shared with mobile devices

Industry observers now estimate that CTV households could surpass 60 million by end-2025, overtaking India’s shrinking pay-DTH base of ~57 million subscribers. This crossover represents a structural inflection point: India is moving from a linear TV-first market to a CTV-first market.

CTV Advertising Revenue

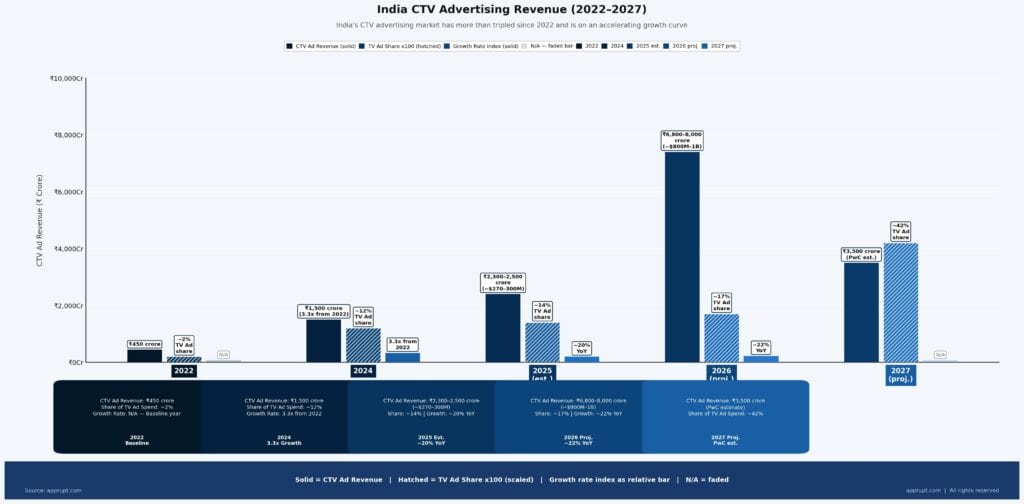

India’s CTV advertising market has more than tripled since 2022 and is on an accelerating growth curve:

| Year | CTV Ad Revenue (India) | Share of TV Ad Spend | Growth Rate |

| 2022 | ₹450 crore | ~2% | — |

| 2024 | ₹1,500 crore | ~12% | 3.3x from 2022 |

| 2025 (est.) | ₹2,300–2,500 crore (~$270–300M) | ~14% | ~20% YoY |

| 2026 (proj.) | ₹6,800–8,000 crore (~$800M–1B) | ~17% | ~22% YoY |

| 2027 (proj.) | ₹3,500 crore (PwC est.) | ~42% | — |

GroupM’s TYNY 2025–2026 projections highlight that streaming TV now makes up over 12.6% of total TV ad revenue. The broader Indian advertising market is projected to reach ₹2,01,891 crore in 2026, growing at 9.7%, with CTV and retail media identified as the two fastest-growing segments.

A PwC report projects global CTV ad revenues will reach ₹4.26 lakh crore by 2029, equivalent to 45% of traditional broadcast TV advertising. India is catching up fast, with 92% of Indian marketers expecting video budgets to increase and more than half planning to increase CTV investments specifically.

FAST Platform Landscape in India

India’s FAST ecosystem features both global OEM-embedded platforms and domestic content providers:

Samsung TV Plus India

- 160+ channels as of November 2025 (up from 27 at launch in March 2021)

- Available on 14+ million Samsung Smart TVs in India

- India was the first APAC market to achieve 100 FAST channels

- Content partners include NDTV, Republic, Zee News, Times Now, ABP News, ETV Network, B4U, and Shemaroo

- On Samsung Smart TVs in India, AVOD (including Samsung TV Plus) accounted for 89% of all streaming time (Q1 2023 data)

LG Channels India

- ~100 live TV channels as of March 2025, up from 9 at launch in September 2023

- Samsung TV Plus still leads with 134 channels vs. LG’s ~100

- ZEE5 launched five FAST channels on LG Channels in August 2025

ZEE5 FAST Channels

- Launched FAST channels in August 2025 in partnership with Amagi

- Curated 24/7 channels spanning comedy, drama, horror, and cult classics

- Available on LG Smart TVs and expanding to Samsung TV Plus and other platforms

- Represents the first time India’s largest OTT platform committed to the FAST model at scale

Atrangii

- Launched FAST channels on LG and Xiaomi Smart TVs in July 2025 — positioned as the first Indian OTT brand to debut a Hindi GEC on LG’s FAST ecosystem

- Expanding to TCL and RUNN TV, with testing on Yupp and CloudWalker

- Powered by Amagi’s cloud playout and SSAI infrastructure

Swastik Stories

- Launched India’s first cultural storytelling & entertainment FAST channel in November 2025

- Targeting 90% penetration of CTV households by March 2026

- IPs reach 10M+ followers across social platforms; FAST distribution expands potential reach to ~50 million viewers

Amagi: India’s FAST Infrastructure Unicorn

Amagi Media Labs, headquartered in Bangalore, is the global backbone of FAST channel delivery and arguably India’s most important contribution to the FAST ecosystem:

- Listed on BSE/NSE on January 21, 2026, becoming the first cloud-native SaaS company offering end-to-end broadcast/streaming solutions to list on Indian exchanges

- IPO raised ₹1,789 crore (₹816 crore fresh issue + ₹973 crore OFS) at ₹361 per share

- FY2025 revenue: ₹1,162 crore (~$137M), with streaming unification accounting for 57% of revenue

- 9M FY2026: 30% revenue growth with 10x+ increase in Adjusted EBITDA

- Powers 5,000+ channels across 50+ FAST platforms globally

- Key Indian partnerships: Shemaroo, B4U, ZEE5, Atrangii, Swastik Stories

- Monetization segment (Thunderstorm SSAI, ADS Plus, Amagi Connect) generated ₹280 crore in FY2025, up 38% YoY

South Korea: Asia’s Next FAST Powerhouse

South Korea is establishing itself as one of the world’s most dynamic FAST markets, according to Omdia research presented at the International Streaming Festival in Busan.

Market Metrics

- FAST revenue: $23 million in 2024, projected to double to $48 million by 2030

- Positioned to become the 12th largest global FAST market by 2030

- Third-largest FAST market in APAC, behind Australia and Japan

Platform Hierarchy

The South Korean FAST ecosystem is led by domestic platforms with strong global content partnerships:

- Wavve — Market leader, jointly owned by SK Telecom and South Korean broadcasters

- Samsung TV Plus — 5th most-watched video service on Korean connected TVs

- LG Channels — 10th most-watched video service on Korean connected TVs

- LG U+ — Gaining ground from its telecom base

- Diva (formerly D’Live) — Emerging competitor

K-Content Driving Global FAST

The Korean FAST boom is inseparable from the global K-content phenomenon. Netflix, which offers over 8,000 Korean titles in South Korea (more than Amazon, Apple TV+, and Disney+ combined), has been the “global ambassador for K-content”. Squid Game remains Netflix’s most-watched show ever with 1.65 billion hours viewed. This SVOD-driven popularity is now spilling over into FAST, where Korean series and formats are gaining ground on ad-supported platforms globally.

Japan: Mature Market with FAST Upside

Japan’s premium streaming sector reached $7.2 billion in revenue in 2025 (15% YoY growth), driven by ad-supported tiers, local content investment, and live sports. The FAST-specific opportunity within this ecosystem is significant.

FAST Revenue & Users

- Japan’s FAST market revenue projected at $297.43 million in 2025 (Statista)

- Estimated to reach $113 million by 2027 with 26.6 million users (alternative estimate focusing on pure FAST)

- Total streaming viewing hours: 8.1 billion hours in 2025

Key Platforms

- TVer (broadcaster-supported FAST/AVOD): Largest share of viewing time at 23% of premium video hours

- ABEMA (CyberAgent): Weekly active users exceeding 28 million; 60% of users under 30; turned profitable for the first time in FY2025 with ¥7.2 billion (~$47M) operating profit

- Prime Video: 19.3 million subscribers, 22% of total viewing hours

- Netflix: Slightly trails Prime Video in viewing hours but leads in per-subscriber engagement (~20 hours/month)

ABEMA’s profitability milestone is particularly significant for the FAST model — it proved that a free, ad-supported streaming platform can achieve sustainable profitability in Asia’s most mature content market.

Australia: APAC’s Largest FAST Market

Australia holds the distinction of being the largest FAST market in the Asia-Pacific region and among the top five globally, behind only the U.S., UK, and Canada.

Market Data

- FAST revenue projected to reach $480 million by 2027, according to Samsung Ads’ “Behind the Screens” report

- 522 FAST channels available across Australian services (as of September 2023), with 278 unique channels

- 1 in 3 Australians watches FAST multiple times per week

- 60% of non-paid Australian streamers believe there is enough quality free content to avoid paying for streaming

- Sports channels over-index in Australia compared to global averages

Key Platforms

- 7Plus, 10Play, 9Now — Local broadcaster-owned BVOD/FAST services dominate

- Samsung TV Plus — Expanded from 21 to 96+ channels within two years in Australia

- Pluto TV — Launched in Australia via 10Play partnership with 50+ channels

- Tubi — Also present in the Australian market

Southeast Asia: Early-Stage but Accelerating

Southeast Asia represents the newest and most rapidly expanding FAST frontier in the APAC region.

Samsung TV Plus SEA Growth

Samsung TV Plus launched in Southeast Asia in late 2024 and has achieved remarkable first-year metrics:

- 230+ channels across Singapore, the Philippines, and Thailand — a six-fold increase from the initial 20+ channels per country

- Monthly active users up 70% YoY

- Total viewing hours up 125% YoY

- 12 million unique viewers across 4.4 million Smart TVs in the region

- 13 new channels added in December 2025 from A+E Global Media and wedotv

- New FAST channels from allrites (VILN, The Apartment, Inspire) launched in April 2025

Regional Streaming Context

The broader Southeast Asian premium VOD market added 1.5 million net new subscribers in Q2 2025 alone (nearly double Q1), with Netflix leading at 12.8 million subscribers, followed by Viu (9.9M) and iQIYI. Total viewing hours across both small and large screens surpassed 3.1 billion in Q2 2025 across Indonesia, Malaysia, the Philippines, Singapore, and Thailand.

FAST channels are positioned to capture a significant incremental audience in this region, particularly given the strong cultural acceptance of ad-supported viewing and the high price sensitivity of many Southeast Asian consumers.

Platform & Provider Landscape

Key FAST ecosystem players across Southeast Asia include:

- Samsung TV Plus — First OEM FAST service in the region; dominant position

- Indonesia: Orbit OTT, Transvision, Vidio

- Malaysia: Astro, Unifi TV, Select-TV

- Philippines: Converge, ABS-CBN, GMA, TV5

- Thailand: AIS, True ID

- Technology providers: Amagi, SoFast, and OTTclouds power FAST infrastructure

Cross-Regional Growth Drivers

Smart TV Adoption

Smart TV penetration is the single most important enabler of FAST growth across APAC. Samsung has been the world’s best-selling TV brand for 19 consecutive years, and its OEM-embedded Samsung TV Plus reaches 630 million active devices worldwide. In India specifically, sales of 55-inch+ smart TVs grew 43% in 2024, while broadband homes and sub-₹10,000 smart TVs together account for 46 million homes.

Ad-Supported Viewing Culture

APAC audiences are significantly more receptive to ad-supported models than Western counterparts. In India, 91% of CTV viewers engage with ads while watching content, and many take immediate second-screen actions such as browsing or shopping. On Samsung Smart TVs in India, AVOD accounted for 89% of all streaming time in recent measurements. This cultural alignment with ad-supported viewing gives FAST an inherent advantage over subscription-only models in price-sensitive markets.

Regional Content Demand

Local and Asian content remains dominant and continues to rise in popularity across the region. Korean, Japanese, and Chinese originals drive engagement on both SVOD and FAST platforms. The success of K-content globally is now directly fueling Korean FAST channel exports, while Indian mythological, devotional, and regional content is driving FAST adoption among CTV households in India.

Risks & Challenges

Despite the growth trajectory, several structural challenges could temper FAST expansion in APAC:

- Content discovery fragmentation: With 4,300+ channels globally on Samsung TV Plus alone, viewers face increasing difficulty finding content, potentially leading to engagement plateaus

- Low ad CPMs: APAC markets generally command significantly lower CPMs than the U.S. or Europe, limiting per-user revenue potential

- Smartphone-first viewing: In India and Southeast Asia, 80%+ of streaming still happens on mobile devices, where the lean-back, channel-surfing FAST experience is less natural

- Competition from ad-supported SVOD tiers: Netflix, Disney+, and Amazon Prime Video have all launched ad-supported tiers in APAC, competing for the same advertising budgets with higher-profile content

- FAST accounts for only 2–3% of total advertising OTT revenue even in mature European markets — APAC markets are even earlier in this adoption curve

- Infrastructure gaps: Broadband penetration in rural India and parts of Southeast Asia remains patchy, limiting CTV adoption to urban and semi-urban areas