Samsung TV Plus, the manufacturer-embedded FAST (Free Ad-Supported Streaming TV) service from Samsung Electronics, crossed 100 million monthly active users (MAU) globally in January 2026. This milestone — up from 88 million MAU reported in October 2024 — cements Samsung TV Plus as one of the largest FAST platforms in the world, alongside Tubi and the Roku Channel. The platform now offers over 4,300 channels across 30 countries, with 700+ channels in the U.S. alone. Streaming hours increased 25% year-over-year in 2025, while Samsung Ads generates an estimated $700–$750 million in annual advertising revenue. Samsung TV Plus has also become Europe’s top-grossing FAST platform, overtaking Pluto TV in late 2025.

User Growth Timeline

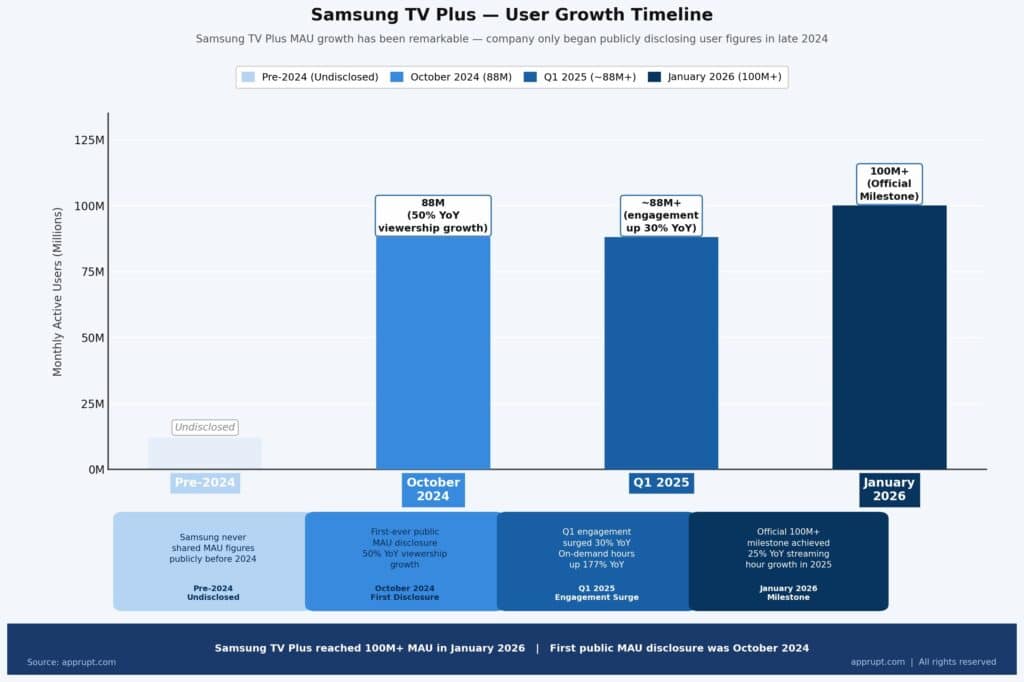

Samsung TV Plus’s MAU growth has been remarkable, particularly given that the company only began publicly disclosing user figures in late 2024.

| Period | Monthly Active Users | Key Context |

| Pre-2024 | Undisclosed | Samsung never shared MAU figures publicly |

| October 2024 | 88 million | First-ever public MAU disclosure; 50% YoY viewership growth |

| Q1 2025 | ~88M+ (engagement up 30%) | Q1 engagement surged 30% YoY; on-demand hours up 177% YoY |

| January 2026 | 100+ million | Official milestone; 25% YoY streaming hour growth in 2025 |

Samsung was the last of the major FAST players to begin sharing user data. When the 88 million figure was released in October 2024, it put Samsung TV Plus on par with Tubi (81M MAU as of September 2024) and Roku (83.6M streaming households as of mid-2024). By January 2026, the 100M+ milestone placed Samsung TV Plus at the top of the FAST MAU rankings alongside Tubi, which also reported 100M+ MAU in mid-2025.

Active Device Ecosystem

A critical differentiator for Samsung TV Plus is its hardware-embedded distribution model. The platform is available across 630 million active Samsung devices worldwide. This includes:

- Samsung Smart TVs (all models from 2016 onward)

- Galaxy smartphones and tablets

- XR headsets

- Smart Monitors

- Family Hub smart refrigerators

- 2026 CES lineup: Micro RGB TV, Neo QLED, OLED, The Frame, The Frame Pro

Samsung has been the world’s best-selling TV brand for 19 consecutive years, giving Samsung TV Plus a built-in distribution advantage that standalone FAST apps cannot match. The service comes pre-installed and requires no sign-up, account creation, or credit card — reducing friction to near-zero.

Viewership & Engagement

Streaming Hours Growth

Samsung TV Plus has delivered consistent double-digit viewership growth across multiple measurement periods:

- 2024 full year: Global viewership increased 50% year-over-year (measured in total engagement hours)

- Q1 2025: Engagement surged over 30% year-over-year

- 2025 full year: Streaming hours increased 25% year-over-year

- On-demand viewing (2024): Surged 400% YoY globally

- On-demand viewing (Q1 2025): Grew 177% YoY after Samsung added 70% more shows and movies to its library

The shift toward on-demand content is notable. While Samsung TV Plus was historically a linear-only FAST service, its aggressive expansion into VOD has transformed the platform into a hybrid FAST/AVOD service, mirroring the strategies of Tubi and The Roku Channel.

U.S. TV Share

Samsung TV Plus has not yet been broken out individually in Nielsen’s monthly “Gauge” report, which tracks TV viewing share at the platform level. However, Samsung claims it is the #1 most-used app on Samsung TVs in the U.S., and it over-indexes in the 18–49 advertising demographic as well as during primetime and late-night viewing periods.

For context, competitor Tubi held approximately 2.2% of total U.S. TV time in mid-2025, while The Roku Channel reached a record 3.0%. Pluto TV held roughly 1.0%. Samsung TV Plus likely falls in the 0.5–1.5% range based on available data, though the company has not disclosed a specific figure.

Audience Retention

Samsung TV Plus reports a 92% retention rate after three months — an industry-leading figure that the company uses to position itself as one of the “stickiest” streaming services for advertiser campaigns. This retention is partly structural: because Samsung TV Plus is pre-installed on Samsung hardware, users don’t need to actively re-engage with an app store or re-download the service.

Revenue & Advertising

Samsung Ads Revenue

Samsung does not break out Samsung TV Plus revenue as a standalone line item. However, Samsung Ads — the advertising division that monetizes Samsung TV Plus inventory alongside other Samsung advertising surfaces — generates approximately $700–$750 million per year in advertising revenue, according to rough industry estimates reported by MediaPost.

This figure encompasses all Samsung advertising revenue, not just Samsung TV Plus, and includes:

- In-stream video ads on Samsung TV Plus FAST channels

- Display ads on the Samsung TV home screen

- Programmatic and direct-sold CTV inventory

- Data monetization and audience insights

- Cross-promotion of Samsung services

Advertising Reach

According to an ARF (Advertising Research Foundation) Dash Study released in August 2025, Samsung had an advertising reach of 45.54 million smart TV households in the U.S., virtually tied with Amazon Prime Video at 45.48 million advertising-supported smart TV households. Samsung has stated it draws first-party viewing and ACR (automated content recognition) data from 77 million active Samsung Smart TVs in the U.S..

Revenue Model

Samsung TV Plus monetizes through multiple streams:

- Ad-supported streaming: Traditional in-stream commercials similar to linear TV advertising

- Revenue-sharing with content partners: Samsung takes a percentage of ad revenue generated from third-party channels

- Premium ad placements: Targeted advertising based on viewer preferences, including sponsored content, banner ads, and in-stream commercials

- Data monetization: Samsung collects viewership data and offers advertisers premium access to audience insights and targeting

- Unified auction technology: Via a multi-year partnership with Publica by IAS, Samsung uses OpenRTB 2.6 framework-based unified auctions to maximize yield

- Data Clean Room (Data+): Launched with Snowflake in January 2026, allowing brands to combine their first-party data with Samsung’s audience and campaign data

European Market Leadership

Samsung TV Plus achieved a major milestone in late 2025 by overtaking Pluto TV to become Europe’s highest-revenue FAST platform.

Key European FAST market data from Dataxis:

- European FAST pure-players generated €630 million in revenue over the prior 12 months, a 33% increase year-over-year

- Samsung TV Plus and LG Channels together accounted for 71% of additional revenue growth

- Each platform (Samsung TV Plus and LG Channels) added more than €15 million in additional Q3 2024 revenue compared to the prior quarter

- Tubi (Fox) and Pluto TV (Paramount) ranked third and fourth respectively, contributing a significantly smaller share to overall growth

The European shift is driven by what Dataxis calls the “hardware advantage” — CTV-embedded services like Samsung TV Plus and LG Channels benefit from native access to millions of smart TV screens, bypassing the need for app downloads. However, Dataxis also notes that FAST still accounts for only 2–3% of the total advertising OTT market in Europe, suggesting substantial room for growth.

Channel & Content Expansion

Channel Count

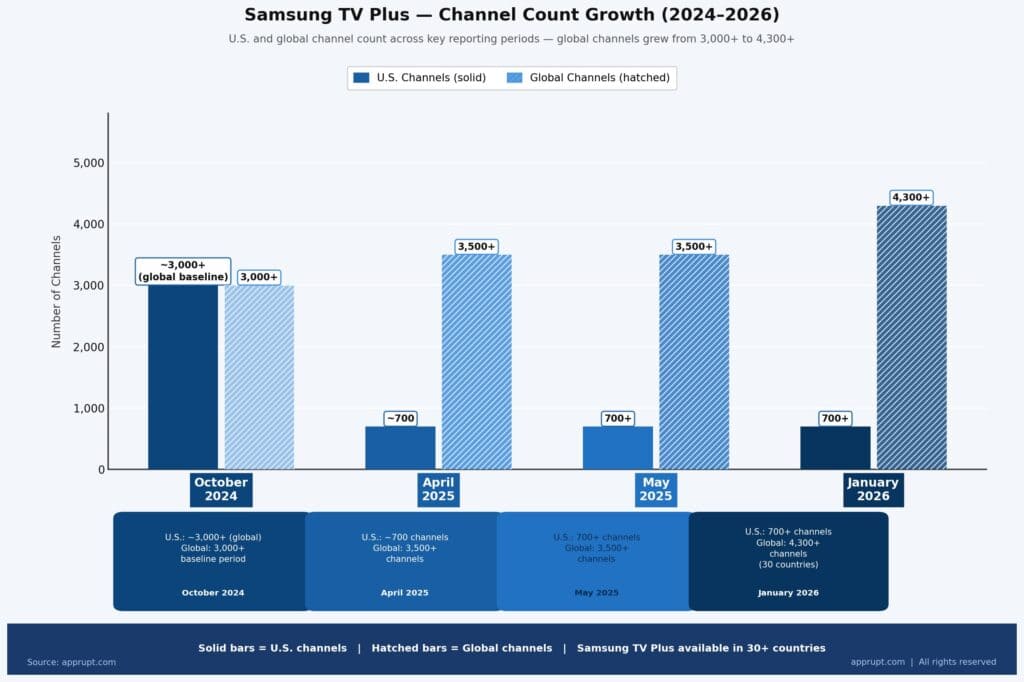

| Period | U.S. Channels | Global Channels |

| October 2024 | ~3,000+ (global) | 3,000+ |

| April 2025 | ~700 | 3,500+ |

| May 2025 | 700+ | 3,500+ |

| January 2026 | 700+ | 4,300+ |

Samsung TV Plus offers more FAST channels in the U.S. than any other major platform, including over 100 exclusive channels such as Conan O’Brien TV and Letterman TV.

Content Partners

Samsung has established partnerships with dozens of major studios, media companies, and sports leagues:

- Studios/networks: Disney, Lionsgate, Paramount, A&E, NBC, CBS

- Sports leagues: NFL, NBA, MLB, NHL, FIFA+, PGA Tour

- Creator partnerships (2025): Mark Rober, Dhar Mann (first-ever scripted FAST original deal), Michelle Khare, Smosh, The Try Guys, Epic Gardening, Donut Media

- Entertainment partners: Spotify, David Letterman, Conan O’Brien

- Live events: Jonas Brothers “JONAS 20: Greetings From Your Hometown” tour (first FanVote interactive feature)

Local News

Samsung TV Plus provides local news coverage in 114 U.S. DMAs (Designated Market Areas), making it one of the most comprehensive local news FAST providers in the country.

India & Asia-Pacific Expansion

India Market

Samsung TV Plus describes itself as India’s leading free ad-supported streaming TV service. Key India metrics:

- Channels: 160+ channels as of November 2025, up from 100+ in May 2023

- Reach: Available on more than 14 million Samsung Smart TVs across India

- Content mix: More than half of content from local providers, including NDTV, Republic, Zee News, Zee Business, Times Now, ABP News, ETV Network, and B4U channels

- Growth: India was the first APAC market to achieve 100 FAST channels

- AVOD dominance: On Samsung Smart TVs in India, AVOD (including Samsung TV Plus) accounted for 89% of all streaming time in Q1 2023, outpacing SVOD

India’s broader CTV advertising market was projected to reach ₹2,500 crore (~$300M) by end of 2025, marking 35% growth in 2024. Samsung TV Plus is well-positioned to capture a significant share given Samsung’s dominant smart TV footprint in the Indian market.

Southeast Asia

In February 2026, Samsung Ads announced a partnership with Teads to introduce next-generation CTV homescreen display and video advertising across Southeast Asia, Hong Kong, and Taiwan. Samsung Smart TVs have a “dominant footprint” among affluent, tech-savvy households in the region. Samsung TV Plus launched in Singapore and the Philippines in 2024, with Thailand following shortly after.

Competitive Positioning

FAST Platform Comparison (2025–2026)

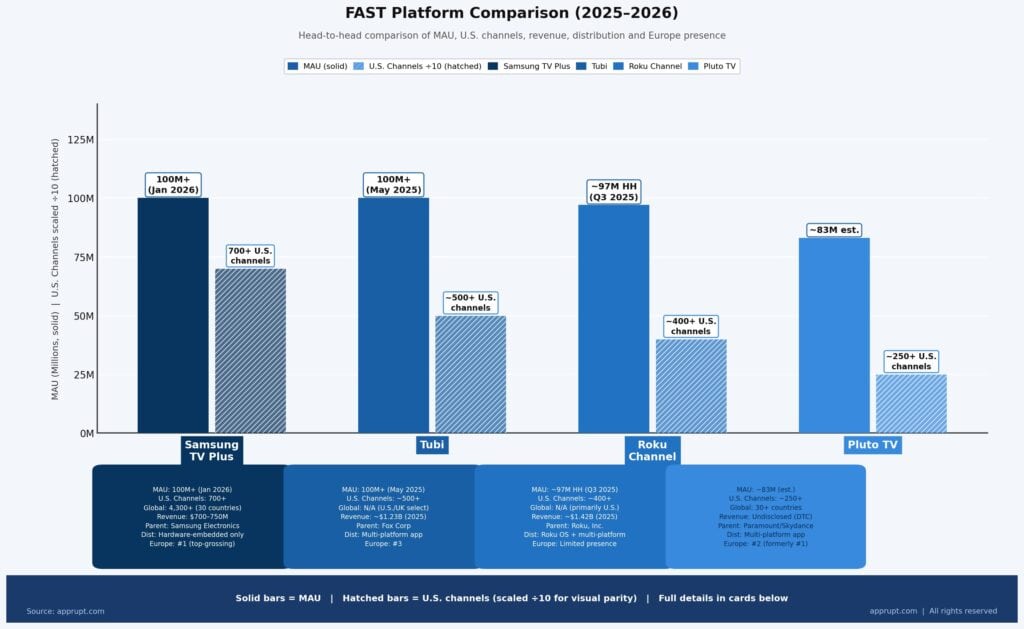

| Metric | Samsung TV Plus | Tubi | Roku Channel | Pluto TV |

| MAU (latest) | 100M+ (Jan 2026) | 100M+ (May 2025) | ~97M households (Q3 2025) | ~83M (est.) |

| U.S. Channels | 700+ | ~500+ | ~400+ | ~250+ |

| Global Channels | 4,300+ | N/A (U.S./UK/select) | N/A (primarily U.S.) | Available in 30+ countries |

| Countries | 30 | 5+ | Primarily U.S. | 30+ |

| Revenue (est.) | $700–750M (Samsung Ads total) | ~$1.23B (2025) | ~$1.42B (2025) | Undisclosed (within Paramount DTC) |

| Parent | Samsung Electronics | Fox Corp | Roku, Inc. | Paramount/Skydance |

| Distribution | Hardware-embedded only | Multi-platform app | Roku OS + multi-platform | Multi-platform app |

| Europe leader? | Yes (top-grossing) | No. 3 | Limited presence | No. 2 (formerly No. 1) |

Structural Advantages

Samsung TV Plus has several distinctive competitive advantages:

- Zero-friction distribution: Pre-installed on all Samsung Smart TVs since 2016, eliminating download and sign-up barriers

- First-party data moat: Samsung’s ACR technology on 77 million active Smart TVs provides granular viewership data unmatched by app-based competitors

- Hardware lock-in: Available exclusively on Samsung devices, meaning every Samsung TV sold expands the addressable base automatically

- Home screen real estate: Samsung TV Plus occupies prime positioning on the Samsung TV interface, driving higher discovery than app-store-based competitors

Structural Limitations

- Exclusivity constraint: Unlike Tubi and Pluto TV, Samsung TV Plus is only available on Samsung devices, capping its addressable market to Samsung’s hardware install base

- Nielsen visibility gap: Samsung TV Plus has not yet achieved the threshold needed to be individually broken out in Nielsen’s monthly Gauge report, limiting third-party validation of its TV share claims

- Revenue opacity: Samsung does not separately disclose Samsung TV Plus revenue, making direct financial comparisons difficult

2026 Outlook & Growth Drivers

Near-Term Growth Catalysts

- New hardware cycle: The 2026 Samsung TV lineup (Micro RGB, Neo QLED, OLED, The Frame Pro) launched at CES will expand the addressable device base further

- Creator-led content: Samsung’s exclusive partnerships with top digital creators (Mark Rober, Dhar Mann originals, Smosh) represent a differentiated content strategy that no other FAST platform has matched at similar scale

- Interactive features: The FanVote interactive polling feature (13%+ CTV response rate) signals Samsung’s push toward “active engagement” viewing that could command premium ad pricing

- Data Clean Room monetization: The Data+ with Snowflake launch opens new lower-funnel advertising opportunities

- Sports expansion: Partnerships with MLB, NBA, NHL, NFL, and FIFA+ position Samsung TV Plus to capitalize on the FAST sports boom

Industry Tailwinds

S&P Global Market Intelligence estimates global FAST channel ad revenue could rise at a compounded annual growth rate of 15–17% to $9 billion globally in 2026. Samsung TV Plus is positioned to capture a growing share of this expanding market, particularly as cord-cutting accelerates and subscription fatigue drives consumers toward free alternatives. The broader CTV advertising market continues its rapid expansion, with India alone projected to see 35%+ annual growth in CTV ad spend.

Key Risks

- FAST market saturation: Industry analysts have raised concerns about an oversupply of FAST channels in the U.S., making content discovery increasingly difficult for viewers

- FAST remains niche in advertising: Despite rapid growth, FAST accounts for just 2–3% of total advertising OTT revenue in Europe, suggesting that macro advertising budgets have not yet shifted meaningfully toward FAST

- Competition from ad-supported tiers: Netflix, Disney+, Amazon Prime Video, and other premium SVOD services have launched ad-supported tiers that compete for the same CTV advertising budgets, often with higher-profile content.