Free streaming apps — encompassing Free Ad-Supported Streaming TV (FAST), Advertising-based Video on Demand (AVOD), and free streaming software — are experiencing explosive growth. The global FAST market was valued at approximately $9.73 billion in 2024 and is projected to reach $40.20 billion by 2033, growing at a CAGR of 16.9%. Platforms like Tubi, The Roku Channel, Pluto TV, and Samsung TV Plus collectively serve over 350 million monthly active users worldwide. Viewership hours on major free ad-supported streaming services surged 43% year-over-year in 2025, while 45% of U.S. households now regularly watch FAST content. As subscription fatigue intensifies and advertisers shift dollars from linear TV to connected TV (CTV), free streaming apps are positioned as the fastest-growing segment of the broader video streaming ecosystem through 2033.

Free Streaming App Market Size & Forecast (2026–2033)

FAST Market

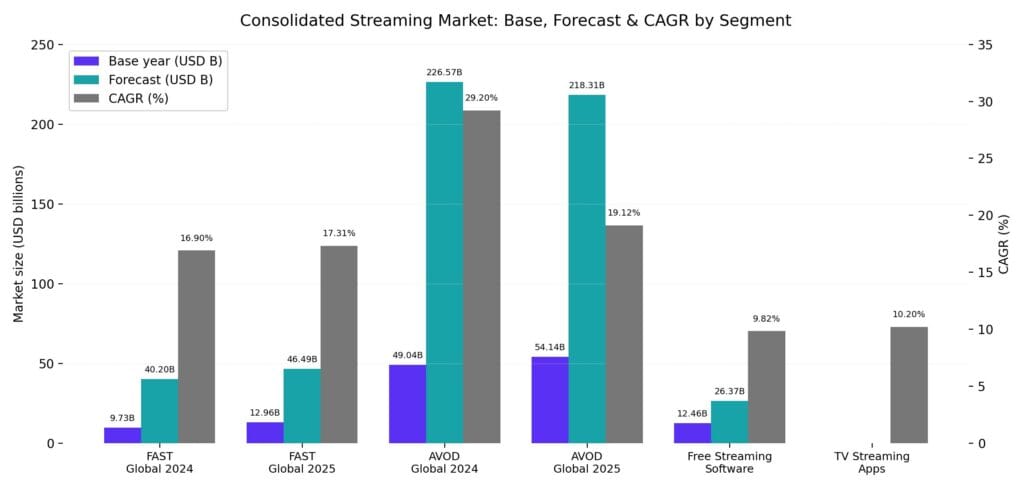

The Free Ad-Supported Streaming TV (FAST) market represents linear, channel-based free streaming — the segment closest to traditional TV. Grand View Research estimated the global FAST market at $9.73 billion in 2024, projecting it to reach $40.20 billion by 2033 at a CAGR of 16.9%. Data Bridge Market Research places the 2025 valuation higher at $12.96 billion, forecasting $46.49 billion by 2033 at a CAGR of 17.31%.

FAST revenue by region shows strong U.S. dominance: North American FAST revenue stood at $4.6 billion in 2023 and is projected to reach nearly $7.5 billion by 2029. Europe captured $1.3 billion in 2023, with forecasts suggesting a rise to approximately $3.74 billion by 2029. Digital TV Research projects total global FAST revenue of $16.5 billion by 2029, more than doubling the $7.6 billion recorded in 2023.

AVOD Market

The broader AVOD market, which includes on-demand free streaming and ad-supported tiers of premium services, is growing even faster. Grand View Research valued the global AVOD market at $49.04 billion in 2024, projecting $226.57 billion by 2030 at a CAGR of 29.2%. SNS Insider estimates the market at $54.14 billion in 2025, forecasting $218.31 billion by 2033 at a CAGR of 19.12%.

Free Streaming Software Market

Free streaming software — including tools like OBS Studio, Streamlabs, and consumer streaming apps — was valued at $12.46 billion in 2025 and is projected to reach $26.37 billion by 2033 at a CAGR of 9.82%. A separate estimate projects the market at $15.8 billion by 2033 at a CAGR of 12.5%.

Consolidated Market Forecast

| Segment | Base Year Value | Forecast (2033) | CAGR | Source |

| FAST (Global) | $9.73B (2024) | $40.20B | 16.9% | |

| FAST (Global) | $12.96B (2025) | $46.49B | 17.31% | |

| AVOD (Global) | $49.04B (2024) | $226.57B (2030) | 29.2% | |

| AVOD (Global) | $54.14B (2025) | $218.31B | 19.12% | |

| Free Streaming Software | $12.46B (2025) | $26.37B | 9.82% | |

| TV Streaming Apps | Billions (2025) | Growing | 10.2% |

Platform User Statistics

Monthly Active Users (MAUs) by Platform

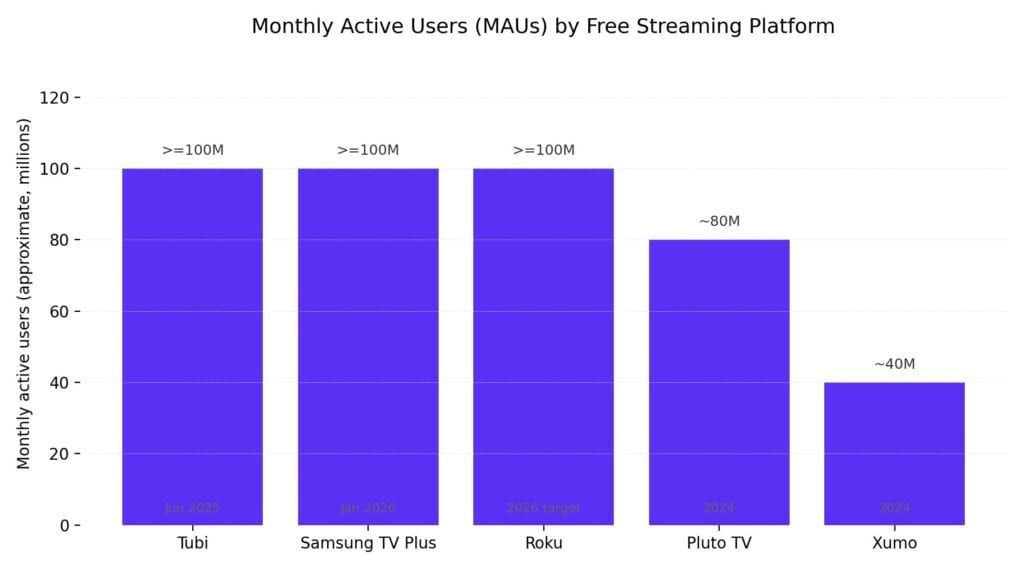

Free streaming platforms have amassed massive user bases, with several platforms surpassing 100 million monthly active users.

| Platform | MAUs | Period | Key Detail |

| Tubi | 100M+ | June 2025 | Exceeded 1B hours in a single month (May 2025) |

| Samsung TV Plus | 100M+ | January 2026 | Streaming hours up 25% YoY; 92% retention rate |

| Roku (Platform) | ~100M households | 2026 target | 89.8M active accounts in Q4 2024; nearing 100M in 2026 |

| Pluto TV | ~80M | 2024 | Bundled with Paramount+ for combined Nielsen tracking |

| Xumo | 40M+ | 2024 | Growing through Comcast/Charter partnership |

Tubi surpassed 97 million MAUs in 2024, streaming over 10 billion hours during the calendar year. By June 2025, Tubi exceeded 100 million MAUs and 1 billion hours of viewing in a single month. Samsung TV Plus crossed 100 million MAUs globally at the start of 2026, with engagement growing 25% year-over-year and a record 177% increase in on-demand hours viewed.

Roku reported 89.8 million active accounts in Q4 2024, with users streaming an average of 253.7 minutes per day. For all of 2025, Roku users collectively streamed 145.6 billion hours, a 15% increase over 2024. CEO Anthony Wood stated that Roku expects to surpass 100 million streaming households in 2026.

Viewership Share by Platform

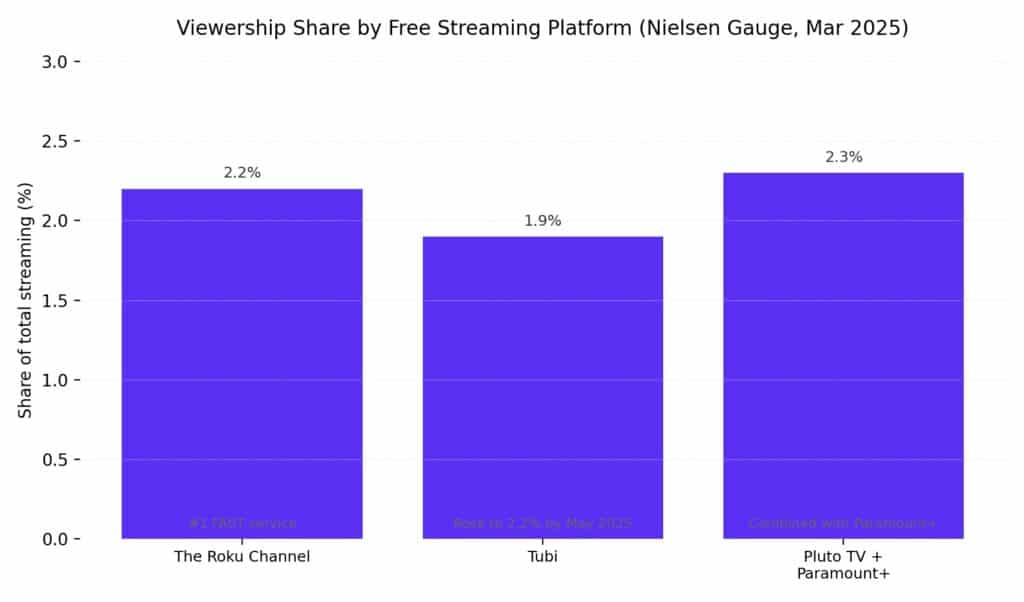

Nielsen’s March 2025 Gauge report revealed the following free streaming rankings in the U.S.:

| Platform | Share of Total Streaming | Notes |

| The Roku Channel | 2.2% | #1 FAST service in the U.S. |

| Tubi | 1.9% | Rose to 2.2% by May 2025 |

| Pluto TV + Paramount+ | 2.3% (combined) | Bundled reporting |

By September 2025, The Roku Channel captured 6.2% of all U.S. TV streaming time. In December 2025, the channel hit a record-breaking 3% share of total U.S. television viewership (including cable and broadcast). Among pure FAST viewers, the top three by share are Tubi (30%), The Roku Channel (25%), and Pluto TV (20%).

Viewership & Engagement Trends

Explosive Growth in FAST Viewing

Comscore’s 2025 State of Streaming report found that total hours watched across major free ad-supported streaming services grew by 43% year-over-year. Total U.S. hours spent watching FAST services reached 1.8 billion in August 2025 alone. Monthly active FAST households were up 12% YoY, while average daily FAST viewing hours per household climbed 16% YoY, resulting in a nearly 29% boost in total hours of viewership across ad-supported streaming channels.

FAST as a Share of Total TV

Free ad-supported streaming collectively accounts for 5.7% of all U.S. TV viewing time as of May 2025. This combined FAST share now exceeds the individual viewing share of any single broadcast network. Streaming overall captured a record 47.3% of all U.S. TV viewing in mid-2025.

Household penetration has risen sharply: 45% of U.S. internet households now regularly watch FAST services, up from 30% in 2022. Connected TV streaming reached 96.4 million U.S. households, with the average household watching content from 6.9 streaming services.

Ad-Supported Tiers of Premium Services

The ad-supported model has expanded well beyond pure FAST platforms. Netflix now sees 45% of its total U.S. household viewing hours on the ad-supported tier, up from 34% in 2024. Amazon Prime Video’s addition of ads to all viewers created the largest single ad inventory expansion in streaming history, reaching over 200 million Prime members with video access. Similar gains appeared across Disney+ (up 16 points), HBO Max, and Discovery+ (each up 10 points).

FAST Channel Ecosystem Growth

Channel Count Explosion

The number of FAST channels globally has grown from approximately 100 in 2019 to over 3,500 by 2025. Nielsen’s Gracenote tracked nearly 1,850 active FAST channels in Q3 2025, reflecting a 76% increase since 2023 and 14% growth from Q1 2025 alone. Samsung TV Plus leads the pack with nearly 700 channels in the U.S. and over 3,500 globally.

Content Genre Breakdown

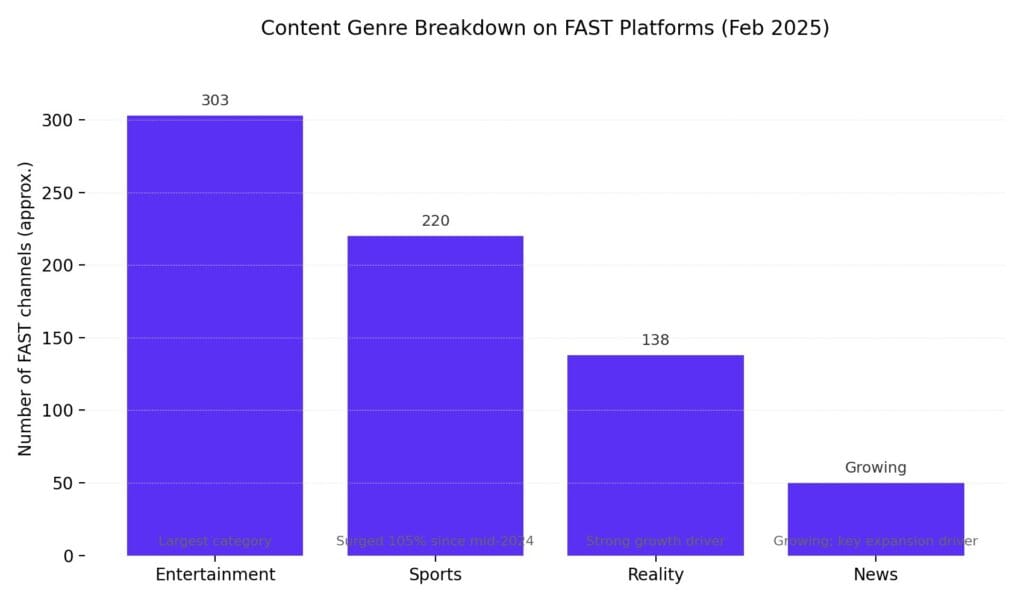

As of February 2025, the leading content genres on FAST platforms are:

| Genre | Number of Channels | Share |

| Entertainment | 303 | Largest category |

| Sports | 220 | Surged 105% since mid-2024 |

| Reality | 138 | Strong growth driver |

| News | Growing | Key expansion driver per Nielsen |

Sports-oriented FAST channels experienced the most dramatic growth, surging more than 105% between mid-2024 and February 2025, reaching 220 dedicated channels representing 13.6% of the FAST market. FOX offered a free livestream of Super Bowl LIX on Tubi in February 2025, signaling FAST’s role as a legitimate venue for marquee live events.

Notably, FAST channels offer a greater percentage of recent content than SVOD services: nearly half of current FAST programming was produced in the last 5 years, compared to roughly one-third on premium SVOD.

Advertising Revenue & CTV Ad Spend

CTV Advertising Growth

Connected TV ad spending reached $33.35 billion in 2025 and is projected to grow approximately 13.8% to around $38 billion in 2026. By 2028, CTV ad spending is expected to hit $46.89 billion, surpassing traditional linear TV advertising for the first time. By 2026, nine streaming services are expected to generate over $1 billion each in ad revenue, up from just two in 2020.

AVOD spending specifically is expected to rise by 17%, fueled by increased revenue from Prime Video, Netflix, and FAST networks, with over $15 billion projected to be spent on 11 platforms in 2025. Revenue spikes include The Roku Channel (22% growth) and Tubi (24% growth).

Platform-Level Revenue

Roku reported total revenue of $4.74 billion for 2025, a 15% increase year-over-year. Platform revenue — which includes advertising — reached $4.15 billion, an 18% year-over-year rise. Netflix’s ad revenue rose more than 250% to over $1.5 billion.

Advertising Industry Shift

By 2029, online video advertising revenue ($362 billion) is projected to far exceed subscription revenue ($185 billion), representing a fundamental shift away from the ad-free streaming model. FAST platforms offer CPMs in the $8–15 range compared to $25–40 for premium SVOD ad tiers, making them attractive for cost-conscious advertisers seeking scale. A survey found that 70% of CTV advertisers plan to boost spending in 2026.

Regional Market Analysis

North America

North America dominated the FAST market with a 31.50% revenue share in 2025. U.S. FAST revenue stood at approximately $5.78 billion in 2025, with Digital TV Research forecasting the U.S. as the only country generating more than $1 billion in FAST revenue by 2029, reaching $6.5 billion. The U.K. and Canada are projected to approach $1 billion each, with these three countries accounting for nearly half the global total.

Pluto TV, The Roku Channel, and Samsung TV Plus are projected to account for nearly half of global FAST revenues by 2029.

Asia-Pacific

The Asia-Pacific region is expected to witness the highest growth rate in the free ad-supported streaming market. The region’s video market is on track to reach $104 billion by 2030, with AVOD revenues projected to rise 69% and FAST revenues set to nearly double over five years. Together, AVOD and FAST are expected to generate more than $25 billion in APAC by 2030.

India’s FAST market is experiencing remarkable growth fueled by internet penetration, smartphone adoption, and demand for affordable entertainment. SVOD subscription numbers across APAC are expected to reach 1.2 billion by 2030.

Latin America & Europe

Brazilian FAST revenues are projected to nearly triple from $119 million in 2024 to approximately $303 million by 2029. Europe captured around 17% of global FAST revenues in 2023 ($1.36 billion), with projections suggesting a rise to about 22% ($3.74 billion) by 2029. The U.K. hosted 643 unique FAST channels by late 2023, with platforms launching an average of 40 new channels monthly.

User Demographics & Behavior

Age & Cord-Cutting Trends

Free streaming platforms skew notably younger than traditional TV. Over half of Tubi’s viewers are Gen Z or Millennials, and 67% are cord-cutters or cord-nevers. Samsung TV Plus’s growth is driven by its core audience of Gen Z, Millennials, and Gen X viewers in the 18–49 advertising demographic. Younger viewers (18–34) show higher FAST adoption rates, driven by economic factors and comfort with ad-supported models.

Viewing Patterns

More than 95% of viewing on Tubi is on-demand movies and TV shows, differentiating it from other FAST platforms that skew toward live, linear channel viewing. Movies dominate free streaming viewership, representing approximately 45% of total viewing time on FAST platforms. Over half of U.S. households stream YouTube content monthly for free, blurring the lines between user-generated and professional free content.

Multicultural Audiences

Nearly half of Tubi viewers are multicultural. One in four Tubi viewers watches Tubi Originals, suggesting demand for exclusive content reflecting diverse lived experiences. Free streaming platforms over-index among multicultural audiences, making them valuable for advertisers seeking to reach diverse consumer segments.

Key Growth Drivers (2026–2033)

Several structural forces are expected to sustain free streaming growth through 2033:

- Subscription fatigue: Rising costs across premium streaming services are pushing consumers toward free alternatives. The average U.S. household already watches content from 6.9 streaming services, creating pressure to consolidate paid subscriptions while maintaining free options.

- CTV and smart TV proliferation: Samsung TV Plus is available across 630 million active Samsung devices globally. Smart TV adoption continues to expand FAST’s addressable audience.

- Advertiser migration: Linear TV has fallen to just 12% of global ad spending, while CTV is on pace to exceed 40% by 2030. Advertisers are following audiences to streaming platforms.

- Content investment: FAST platforms are investing heavily in content — Tubi offers nearly 300,000 movies and TV episodes and 400 originals. Samsung TV Plus added 70% more on-demand titles in 2025.

- Live sports integration: Sports FAST channels surged 105% in recent months, and marquee events like the Super Bowl are now livestreamed free on FAST platforms.

- Global expansion: Markets in India, Brazil, the U.K., and Germany are experiencing rapid FAST adoption, with the Asia-Pacific AVOD market alone projected to grow 69% by 2030.

- AI-driven personalization: Integration of AI for content recommendations and targeted advertising is enhancing viewer engagement and ad effectiveness across free platforms.

Challenges & Risks

Despite strong growth tailwinds, the free streaming market faces several challenges:

- Ad load tolerance: FAST platforms typically run 12–15 minutes of ads per hour. Balancing monetization with viewer experience remains critical, as excessive ads drive viewers away.

- Content licensing costs: Competition for quality content pushes costs higher. As multiple FAST platforms bid for the same libraries, margins face pressure.

- Market fragmentation: Outside the top platforms, the FAST market remains highly fragmented with far less globalization than in the SVOD sector.

- Privacy and data concerns: Data-driven advertising on free platforms raises data privacy and security challenges that could face regulatory scrutiny.

- Economic sensitivity: Ad-supported models are more vulnerable to economic downturns, as advertising budgets are typically among the first to be cut during recessions.

- Measurement complexity: Cross-platform measurement remains a work in progress, with advertisers demanding better tools to connect CTV ad activation with outcomes.

Conclusion

Free streaming apps represent the fastest-growing segment of the global video streaming ecosystem. The FAST market alone is projected to grow from under $13 billion in 2025 to over $40–46 billion by 2033, while the broader AVOD market could exceed $218 billion. Leading platforms — Tubi, Samsung TV Plus, The Roku Channel, and Pluto TV — have each surpassed or approach 100 million monthly active users. With viewership hours growing 43% year-over-year, 45% U.S. household penetration, and CTV ad spend projected to surpass traditional TV by 2028, free streaming is no longer a niche alternative — it is becoming the default viewing experience for a growing share of global audiences.