The global smart TV market is experiencing robust growth driven by rising OTT/streaming adoption, smart home integration, AI-powered features, and declining display panel costs. While estimates vary across research firms, the market was valued between USD 245–273 billion in 2025 and is projected to reach USD 363–673 billion by 2033, with compound annual growth rates (CAGR) ranging from 5.6% to 13.9% during the 2026–2033 forecast period. Asia Pacific dominates with over 40% of global revenue, and Samsung, LG, and TCL remain the leading manufacturers.

Market Size Estimates Across Research Firms

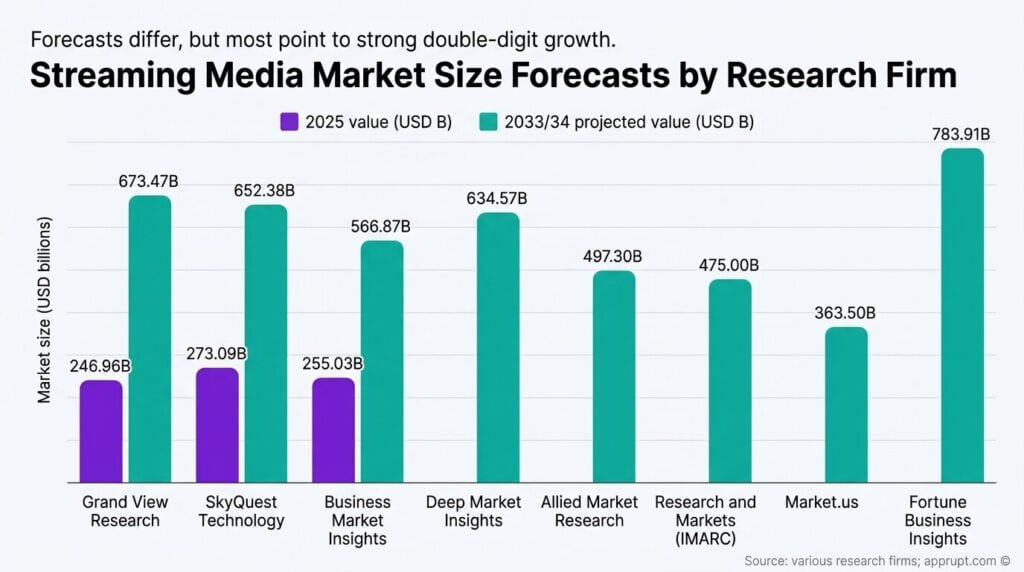

Market sizing estimates vary significantly depending on the methodology and scope used by each research firm. The table below compares the leading forecasts:

| Research Firm | 2025 Value (USD B) | 2033 Projected Value (USD B) | CAGR | Forecast Period |

| Grand View Research | 246.96 | 673.47 | 13.9% | 2026–2033 |

| SkyQuest Technology | 273.09 | 652.38 | 11.5% | 2026–2033 |

| Business Market Insights | 255.03 | 566.87 | 10.5% | 2026–2033 |

| Deep Market Insights | — | 634.57 | 12.0% | 2024–2033 |

| Allied Market Research | — | 497.30 | 9.5% | 2024–2033 |

| Research and Markets (IMARC) | — | 475.00 | 5.6% | 2025–2033 |

| Market.us | — | 363.50 | 6.9% | 2023–2033 |

| Fortune Business Insights | — | 783.91 (by 2034) | 12.98% | 2026–2034 |

The wide range in projections reflects differences in how firms define “smart TV” (hardware-only vs. services included), geographic coverage, and the inclusion of adjacent categories like connected TV advertising revenue. The median estimate clusters around USD 500–570 billion by 2033 with a CAGR of approximately 10–12%.

Key Growth Drivers

Several interconnected forces are propelling the smart TV market forward:

- OTT & streaming proliferation: The rapid shift from cable to platforms like Netflix, Amazon Prime, and Disney+ is a primary demand catalyst. Smart TVs with built-in streaming access are now the default consumer expectation.

- 5G and broadband expansion: Global rollouts of 5G and high-speed broadband enable buffer-free 4K/8K streaming, making high-resolution smart TVs more practical.

- Smart home integration: Smart TVs are increasingly serving as central hubs for IoT ecosystems, integrating with voice assistants, smart speakers, and connected appliances.

- AI-powered features: AI-driven content recommendations, voice controls, adaptive picture optimization, and personalized interfaces are differentiating modern smart TVs.

- Declining panel prices: Falling costs for LED, OLED, and QLED display panels are making smart TVs more affordable, especially in price-sensitive emerging markets.

- Gaming industry growth: Manufacturers are optimizing for low latency and high refresh rates to cater to the next-gen console gaming audience.

Market Segmentation

By Display Technology

LED technology continues to dominate, holding over 54% of market share in 2023 due to its cost efficiency and reliability. OLED and QLED are expanding in the premium segment, driven by superior color accuracy, contrast, and thinner form factors. The 4K Smart OLED TV sub-segment alone was valued at USD 12.46 billion in 2025 and is projected to grow at 9.82% CAGR through 2033.

By Resolution

4K Ultra High Definition (UHD) TVs command the largest share at approximately 48.3%, driven by consumer demand for high-resolution immersive experiences. 8K TVs are emerging but still niche, expected to gain traction as content libraries expand and panel costs decrease.

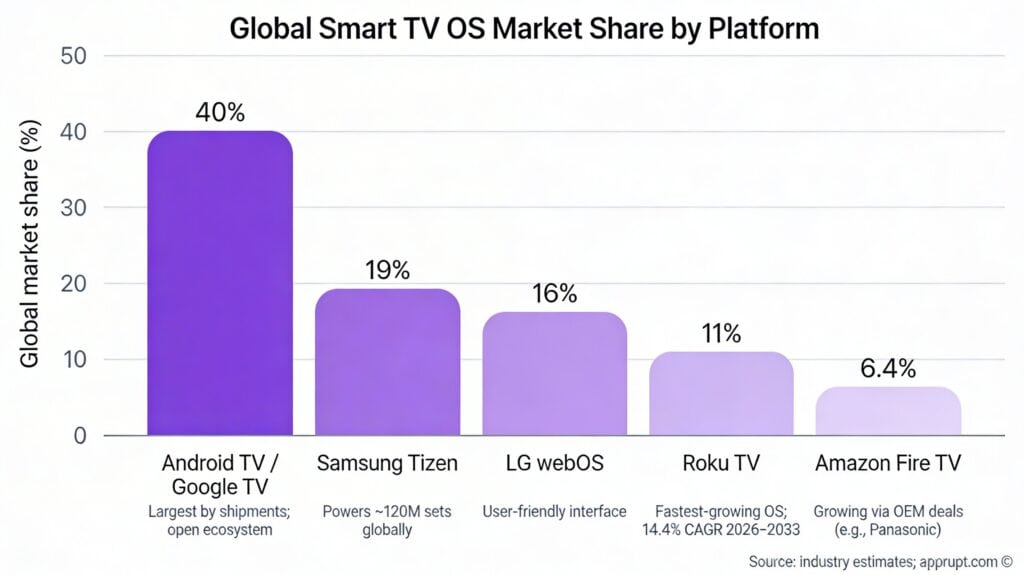

By Operating System

| OS Platform | Global Market Share | Key Details |

| Android TV / Google TV | ~40% | Largest by shipments; open ecosystem, extensive app compatibility |

| Samsung Tizen | ~19% | Powers ~120 million sets globally; strong brand integration |

| LG WebOS | ~16% | Third-largest; known for user-friendly interface |

| Roku TV | ~11% | Fastest-growing OS in the smart TV segment; 14.4% CAGR projected 2026–2033 |

| Amazon Fire TV | ~6.4% | Growing through OEM partnerships with brands like Panasonic |

Roku is expected to register the fastest CAGR of 14.4% from 2026 to 2033, driven by its simplified user interface and strategic partnerships with TV manufacturers.

By Screen Size

The 46-to-55-inch segment leads with over 35.6% market share, popular among consumers seeking a balance between immersive viewing and room compatibility. The above-65-inch segment is expected to register significant growth, fueled by home theater trends, declining large-panel costs, and gaming demand.

By Distribution Channel

Online channels account for over 58% of smart TV sales due to the convenience of comparison shopping, e-commerce discounts, and home delivery. However, offline channels remain relevant for premium and high-end purchases where consumers prefer in-store demonstrations.

Regional Analysis

Asia Pacific (Largest Market — 40%+ Share)

Asia Pacific accounted for the largest revenue share of over 40% in 2025 and is expected to grow at the fastest CAGR of over 16% from 2026 to 2033. Rapid urbanization, an expanding middle class, rising internet penetration, and government digitalization initiatives are key growth catalysts. China leads with over 180 million smart TV users, while India saw smart TV sales increase 65% year-on-year in recent years. In India specifically, Samsung leads with 23–25% market share, followed by LG at 16–18%.

North America

North America is a mature market with high streaming penetration and strong demand for premium display technologies. The U.S. Smart TV market was valued at USD 54.95 billion in 2024 and is projected to reach USD 134.97 billion by 2033, growing at a 10.5% CAGR. Approximately 87% of U.S. households have access to connected TV devices.

Europe

Europe’s smart TV market is expected to grow at a CAGR of over 12% from 2026 to 2033, driven by demand for energy-efficient electronics, rising OTT adoption, and regional sustainability standards influencing purchasing decisions. Smart TV ownership exceeds 50% of European households, reaching approximately 67% in the UK and over 80% in Italy.

Middle East, Africa & Latin America

These regions represent emerging growth opportunities. The Middle East and Africa are forecast to witness a CAGR exceeding 12% between 2023 and 2032, driven by urbanization and rising demand for connected entertainment. Latin America is also seeing rising adoption, though infrastructure constraints remain a challenge.

Competitive Landscape

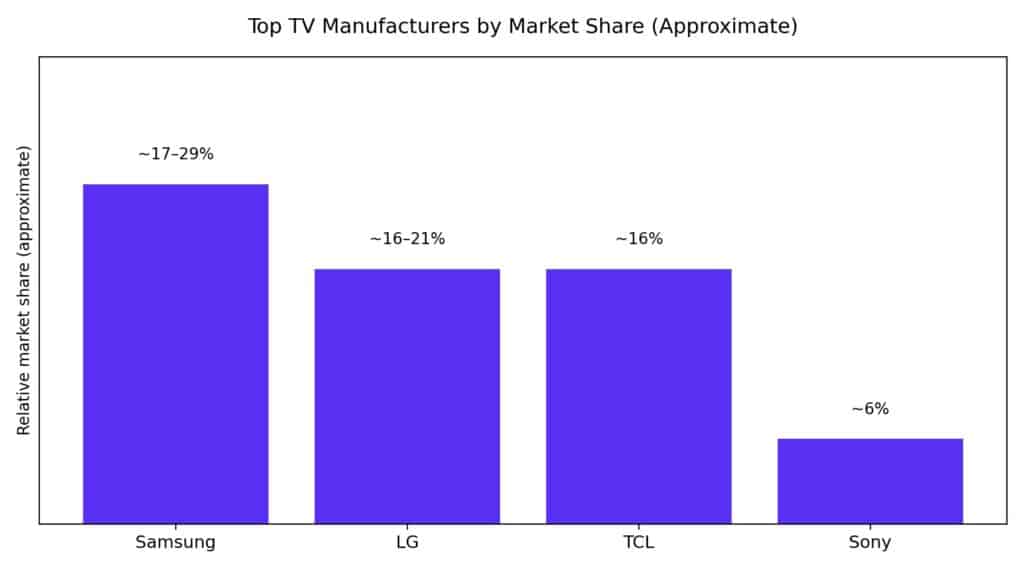

Top Manufacturers by Market Share

| Company | Global Market Share | Key Strengths |

| Samsung Electronics | ~17–29% | Market leader for 9+ consecutive years; Neo QLED, OLED, Crystal 4K; Tizen OS ecosystem |

| LG Electronics | ~16–21% | OLED leader; WebOS platform; strong in North America and Latin America |

| TCL Electronics | ~16% | #2 by shipments; 20% YoY growth; strong in emerging markets |

| Hisense | — | Growing global presence via VIDAA OS; aggressive pricing strategy |

| Sony | ~6% | Premium positioning; strong in picture/audio quality |

| Xiaomi | — | Budget/mid-range leader, especially in India; PatchWall content integration |

Other notable players include Panasonic, Philips (Koninklijke Philips N.V.), Toshiba (TVS Regza Corporation), and Vizio. The top five manufacturers collectively control approximately 58% of global volume.

Samsung remains the dominant force, but TCL is rapidly closing the gap with 22% year-over-year growth and a 16% global share. Competition is intensifying across MiniLED, OLED, and mid-to-large screen segments.

Smart TV Penetration & Advertising

Smart TV household penetration surpassed 34% globally (665 million homes) by the end of 2020 and is projected to exceed 50% (1.1 billion households) by 2026. Digital TV penetration now exceeds 92% of global households, with smart TVs accounting for 79% of installed devices.

Connected TV (CTV) advertising is a fast-growing monetization channel. CTV ad spending in the U.S. reached USD 20.69 billion in 2022 and is projected to hit USD 40.9 billion by 2027. The rise of Free Ad-Supported Streaming TV (FAST) channels is creating additional revenue opportunities for manufacturers and content platforms.

Emerging Trends (2026–2033)

- AI integration: AI-powered content recommendations, voice-activated controls, and smart image processing are becoming standard features, redefining user interaction.

- 8K and MicroLED displays: While still in early adoption, 8K content and MicroLED technology are expected to gain meaningful market share by the late 2020s.

- AR/VR TV experiences: Interactive augmented and virtual reality content is an emerging trend that could reshape the smart TV value proposition.

- Cloud-based streaming platforms: The expansion of cloud gaming and streaming services directly on smart TVs is creating new use cases beyond traditional content viewing.

- Energy efficiency standards: Regulatory emphasis on sustainability and energy labeling, particularly in Europe, is influencing both manufacturing processes and consumer purchasing decisions.

Conclusion

The global smart TV market is poised for strong expansion between 2026 and 2033, with most credible estimates placing the market at USD 475–673 billion by 2033. Growth will be led by Asia Pacific, particularly China and India, while North America and Europe sustain demand through premium upgrades and smart home ecosystem integration. Android TV and Samsung’s Tizen remain the dominant operating systems, but Roku is the fastest-growing platform. Samsung, LG, and TCL continue to lead in hardware, though intensifying competition—especially from Chinese manufacturers—is reshaping the competitive landscape. Key enablers include 5G expansion, AI feature integration, declining panel costs, and the proliferation of streaming and gaming content.