The global streaming media device market is on a strong growth trajectory, valued at approximately USD 15.7–16.8 billion in 2024 and projected to reach USD 43.9–50.8 billion by 2032–2033, depending on the research firm and scope of definition. This represents a compound annual growth rate (CAGR) of roughly 12–14% over the forecast period. The market expansion is driven by accelerating cord-cutting trends, the proliferation of OTT platforms, smart home integration, 5G rollout, and rising demand for high-resolution (4K/8K) content. North America remains the dominant region with ~46% market share, while Asia-Pacific is the fastest-growing market.

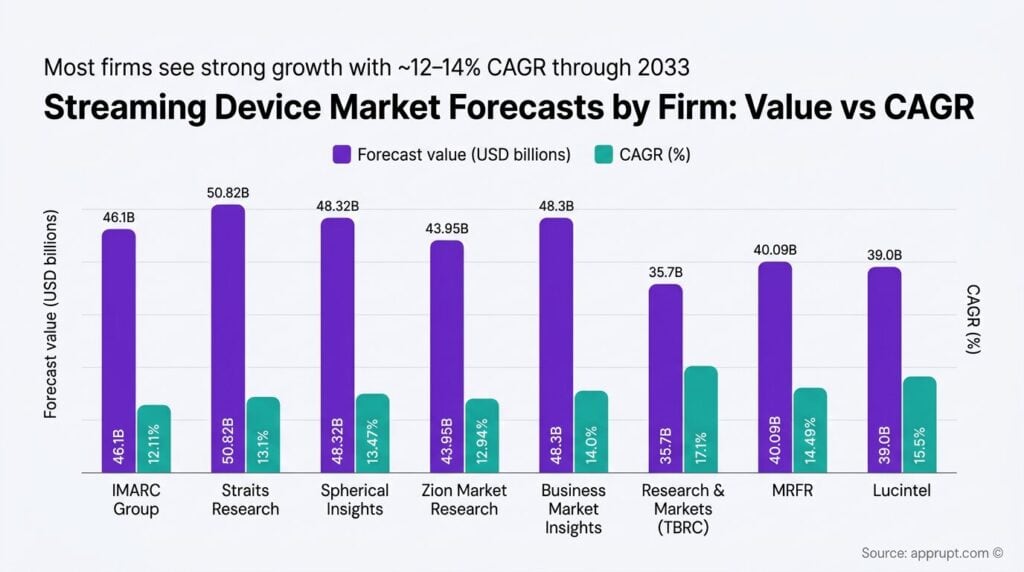

Streaming Devices Market Size Estimates Across Research Firms

Multiple market research firms have published forecasts for the streaming media device market through 2033. The table below consolidates key estimates, revealing a general consensus around a 12–14% CAGR for narrowly defined “streaming devices” (media streamers, gaming consoles, smart TVs):

| Research Firm | Base Year Value | Forecast Value | CAGR | Forecast Period |

| IMARC Group | USD 15.7B (2024) | USD 46.1B (2033) | 12.11% | 2025–2033 |

| Straits Research | USD 16.78B (2024) | USD 50.82B (2033) | 13.1% | 2025–2033 |

| Spherical Insights | USD 13.61B (2023) | USD 48.32B (2033) | 13.47% | 2023–2033 |

| Zion Market Research | USD 14.70B (2023) | USD 43.95B (2032) | 12.94% | 2023–2032 |

| Business Market Insights | USD 16.7B (2025) | USD 48.3B (2033) | 14.0% | 2025–2033 |

| Research & Markets (TBRC) | USD 16.61B (2024) | USD 35.7B (2029) | 17.1% | 2024–2029 |

| MRFR | USD 9.17B (2024) | USD 40.09B (2035) | 14.49% | 2025–2035 |

| Lucintel | — | USD 39.0B (2030) | 15.5% | 2024–2030 |

Sources:

Variations across firms largely reflect differences in market scope—some include gaming consoles and smart TVs alongside media streamers, while others use a broader definition that includes associated software and content delivery ecosystems. The Research & Markets report using a broader scope estimates the market at USD 94.25 billion in 2026 growing to USD 182.12 billion by 2030 at a 17.9% CAGR.

Key Market Segmentation

By Device Type

Gaming consoles hold the largest market share (40%), followed by media streamers (35%). Smart TVs are an increasingly important category as built-in streaming OS platforms reduce the need for standalone devices.

- Gaming consoles — PlayStation, Xbox, and Nintendo Switch serve dual roles as gaming and streaming platforms; their high processing power and large user bases give them an edge.

- Media streamers — Devices like Roku Streaming Stick, Amazon Fire TV Stick, Apple TV 4K, and Google Chromecast dominate the dedicated streaming device category.

- Smart TVs — Increasingly competing with standalone streamers, as 68% of U.S. internet households now own a smart TV compared to 43% using standalone streaming players.

By Resolution

4K resolution is the largest segment, driven by declining prices of 4K displays and expanding 4K content libraries on platforms like Netflix, Disney+, and Amazon Prime Video. HDR and emerging 8K formats represent the next frontier of premium content delivery.

By End Use

The residential segment generates the lion’s share of revenue, fueled by the global rise in home entertainment spending and subscription-based streaming. The commercial segment is the fastest-growing, driven by enterprise adoption for digital signage, corporate communications, and live-streamed events.

By Application

Video streaming is the dominant application segment. Gaming is the fastest-growing application, propelled by cloud gaming services (Xbox Cloud Gaming, NVIDIA GeForce Now) and the convergence of streaming and gaming ecosystems.

Regional Analysis

North America (Largest Market, ~46% Share)

North America dominates the streaming device market and is estimated to hold around 46% of global revenue through 2035. This leadership is underpinned by:

- High broadband penetration and early OTT adoption

- Massive cord-cutting wave — 77.2 million U.S. households had cut the cord by 2025, more than doubling from 37.3 million in 2018

- Strong ecosystem of device manufacturers (Roku, Amazon, Apple, Google) headquartered in the region

- Streaming-only homes projected to reach 100 million in the U.S. by 2026

Asia-Pacific (Fastest Growing)

Asia-Pacific is the fastest-growing regional market, with streaming device adoption accelerating rapidly across China, India, Japan, and South Korea. Key drivers include:

- Rapidly expanding broadband and 5G infrastructure

- Over 547 million video streamers in India alone, with surging OTT platform adoption

- Growing middle-class population and rising disposable incomes

- Aggressive market entry by both global players (Amazon, Google) and regional champions (Xiaomi)

Europe

The European market is approaching maturity for OTT viewership, with Western European nations like Germany, France, and the UK showing strong adoption of both streaming services and devices. The cord-cutting trend and 5G expansion are expected to sustain growth.

Competitive Landscape

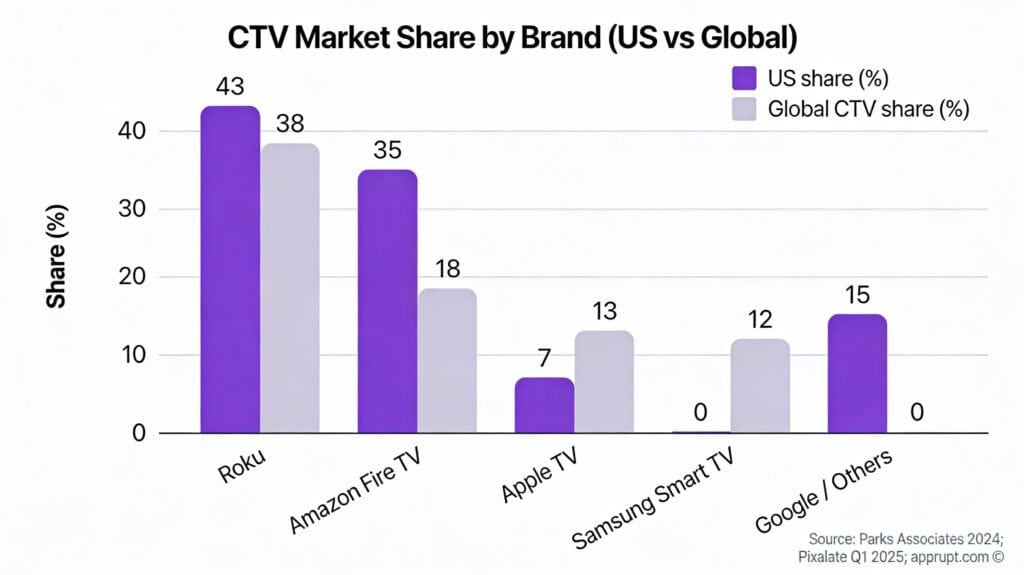

U.S. Market Share by Brand

| Brand | U.S. Market Share (Parks Associates, 2024) | Global CTV Share (Pixalate Q1 2025) |

| Roku | 43% | 38% (US) |

| Amazon Fire TV | 35% | 18% (US) |

| Apple TV | ~7% | 13% (US) |

| Samsung Smart TV | — | 12% (US) |

| Google / Others | ~15% | — |

Sources:

Roku remains the market leader in standalone streaming media players in the U.S., while Amazon Fire TV is the primary challenger with over 250 million Fire TV devices sold globally by late 2024. Apple TV has seen significant global growth—its CTV device market share increased 186% year-over-year in 2024. Samsung and LG compete primarily through smart TV platforms rather than standalone devices.

Key Players

Major companies shaping the market include Roku Inc., Amazon.com Inc., Apple Inc., Google LLC, Sony Corporation, Microsoft Corporation, Samsung Electronics, Xiaomi Corporation, NVIDIA Corporation, LG Electronics, and Huawei Technologies.

Growth Drivers

Cord-Cutting Acceleration

The shift from traditional pay-TV to streaming continues to accelerate. U.S. cable TV subscribers declined to 68.7 million in 2024 from 72.2 million in 2023—a 4.9% drop—while cord-cutting households exceeded 77 million by 2025. Pay-TV households are projected to fall to 50 million by 2027. Price is the primary motivator, with 86.7% of cord-cutters citing high cable costs.

OTT Platform Proliferation

The growth of streaming platforms like Netflix, Amazon Prime Video, Disney+, and regional OTT services directly drives demand for compatible devices. Global OTT subscription adoption reached 66% of Australian households in 2023, up from 59% the prior year—a pattern replicated across major markets.

Smart Home Integration

Streaming devices are evolving from simple media players into smart home hubs. Google’s TV Streamer (2024) doubles as a smart home hub with AI-powered content discovery. Amazon’s Alexa ecosystem powers over 600 million devices globally, with streaming devices serving as central control points. Voice control, IoT integration, and automation features are now standard expectations.

5G and Broadband Expansion

The global rollout of 5G networks and expanding fiber broadband infrastructure reduce latency and enable seamless 4K/8K streaming, particularly in emerging markets. This infrastructure development is critical for Asia-Pacific and Latin American market growth.

AI and Personalization

AI-driven features are becoming a key differentiator. Smart recommendation engines personalize content delivery, while automation in firmware updates and predictive analytics enhance user experience. Devices equipped with large language model (LLM)-integrated voice assistants offer more natural and context-aware interactions.

Challenges and Restraints

Bandwidth Limitations

Despite advances in broadband, the surge in high-resolution streaming (4K, 8K) and simultaneous multi-device usage creates bandwidth bottlenecks, especially during peak hours. Networks face increasing strain as content quality and consumption volumes rise simultaneously.

Content Piracy

Streaming piracy remains a multi-billion dollar problem. Approximately 90 million users accessed pirated video content outside India in 2024, causing an estimated $1.2 billion in losses—a figure projected to double to $2.4 billion by 2029. CDN leeching during live events can account for over half of all CDN traffic. Subscription fragmentation across platforms is a key driver of piracy, as users face growing costs to access content spread across multiple services.

Smart TV Competition

Standalone streaming devices face increasing competition from smart TVs with built-in streaming platforms. Smart TVs are now in 68% of U.S. internet households, compared to 43% using separate streaming players. Only 34% of consumers consider streaming media players their primary viewing device, while 56% favor smart TVs. Roku, Amazon, and Google have responded by embedding their operating systems directly into third-party TV brands.

Subscription Fatigue

Rising streaming subscription costs and platform fragmentation are leading to consumer fatigue. The average household now juggles multiple subscriptions, prompting some users to churn between services or turn to ad-supported and free tiers.

Market Outlook (2026–2033)

The streaming device market is expected to roughly triple in size between 2024 and 2033. Based on the consensus of major research firms, the market is projected to grow from approximately USD 17–19 billion in 2025 to USD 44–51 billion by 2032–2033, maintaining a CAGR of 12–14%.

Key trends shaping the 2026–2033 outlook include:

- Convergence of streaming and gaming — Cloud gaming services will further blur the line between streaming devices and gaming consoles, expanding the addressable market.

- AI-first device experiences — AI-powered content curation, voice interaction, and smart home orchestration will become primary purchase drivers.

- Emerging market expansion — Asia-Pacific and Latin America will deliver the highest growth rates as broadband infrastructure matures and middle-class populations grow.

- Sustainability and energy efficiency — Growing regulatory focus on energy-efficient consumer electronics will influence device design and manufacturing.

- Portable and compact form factors — Continued demand for affordable streaming sticks and ultra-compact streamers will keep hardware accessible.

The market faces headwinds from smart TV integration (which reduces standalone device demand) and subscription fatigue, but the overall trajectory remains firmly positive as global streaming adoption deepens and device capabilities expand.