The global sports streaming market is on a steep growth trajectory, driven by accelerating cord-cutting, surging demand for live sports on digital platforms, and massive investments in sports media rights by both legacy broadcasters and pure-play streamers. Market size estimates vary significantly across research firms—from conservative projections of $22.4 billion by 2033 to bullish forecasts exceeding $108 billion—largely due to differing scope definitions (platform-only vs. broader live video streaming). Common threads across forecasts include double-digit CAGRs, North American dominance, and Asia-Pacific as the fastest-growing region. Global sports media rights spending alone is projected to surpass $78 billion by 2030, with streaming services now accounting for 20% of total rights expenditure.

Sports Streaming Market Size Projections

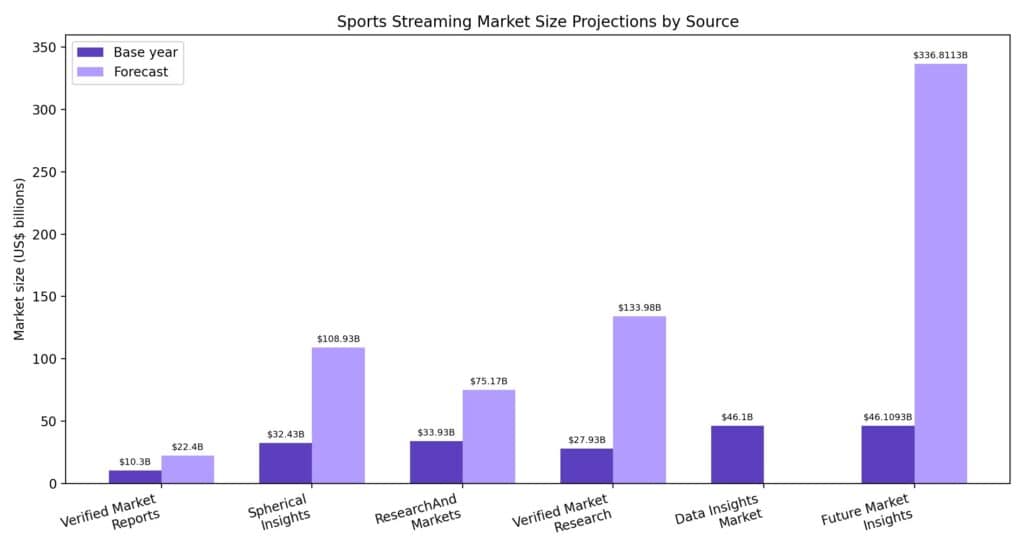

Multiple research firms have published forecasts for the sports streaming market through 2030–2033. The wide range in estimates reflects different market definitions—some focus narrowly on sports streaming platforms, while others encompass the broader online live video streaming ecosystem.

| Source | Base Year Value | Forecast Value | CAGR | Forecast Period |

| Verified Market Reports | $10.3B (2024) | $22.4B (2033) | 9.2% | 2026–2033 |

| Spherical Insights | $32.43B (2023) | $108.93B (2033) | 12.88% | 2023–2033 |

| ResearchAndMarkets (Yahoo Finance) | $33.93B (2024) | $75.17B (2030) | 12.6% | 2025–2030 |

| Verified Market Research | $27.93B (2024) | $133.98B (2032) | 24.64% | 2026–2032 |

| Data Insights Market | $46.1B (2025) | — | 22.0% | 2025–2033 |

| Future Market Insights | — | $336.8B (2035) | 22.0% | 2025–2035 |

Sources:

The more conservative estimates (9–13% CAGR) tend to focus specifically on dedicated sports streaming platforms, while the aggressive projections (22–25% CAGR) incorporate broader live sports video streaming across OTT and social platforms. Despite the variance, all forecasts point to robust double-digit growth through at least 2030.

Sports Media Rights Spending

Global Outlook

Sports media rights form the economic backbone of the streaming market. According to Ampere Analysis, global sports media rights spending totaled $64 billion in 2025 and is forecast to surpass $78 billion by 2030—a 20% increase. Streaming services collectively spent $12.5 billion on sports rights in 2025, representing approximately 20% of the global total.

DAZN led all streaming platforms with a 33% share of streaming sports rights spend in 2025, bolstered by its $1 billion deal for the FIFA Club World Cup and heavy investment in European football leagues. YouTube TV ranked third among streaming investors, driven by its reported $2 billion-per-season NFL Sunday Ticket deal, while Netflix entered the fourth position with its NFL Christmas Day games and $500 million annual WWE deal.

Regional Rights Breakdown

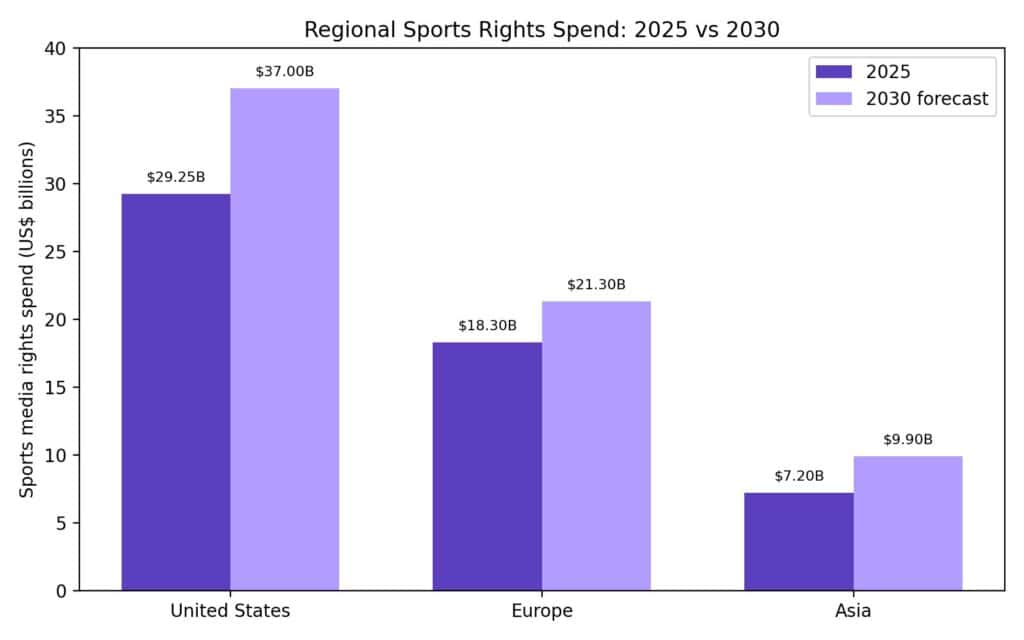

| Region | 2025 Spend | 2030 Forecast | Growth |

| United States | $29.25B | $37B+ | ~27% |

| Europe | $18.3B | $21.3B | 17% |

| Asia | $7.2B | $9.9B | 38% |

Sources:

In the United States, the new NBA rights cycle starting in the 2025–26 season and new MLB agreements from 2029 are the primary drivers. The NFL could provide further upside if it renegotiates its current deals (running through 2034), with initial discussions expected as early as 2026.

In Europe, competition from global streaming platforms is expected to offset recent downward pressure in some auctions. UEFA’s Champions League tender has already attracted bids from Paramount and Amazon Prime Video. In Asia, Indian cricket—particularly new IPL and ICC tournament rights from 2027—will be the dominant growth catalyst.

Cord-Cutting and Audience Migration

The Structural Shift

The migration from traditional pay TV to streaming continues to accelerate. Traditional pay TV penetration in the US dropped from 62% of internet households in Q1 2020 to just 42% by Q1 2025—a 20-percentage-point collapse in five years. Meanwhile, streaming services now reach 89% of internet households. Cord-cutting households more than doubled from 37.3 million in 2018 to a projected 77.2 million by 2025.

Virtual MVPDs like YouTube TV and Hulu + Live TV partially absorbed this shift, growing from 12% to 23% of US households between 2020 and 2025. YouTube TV alone surpassed 8 million subscribers, becoming a top-5 pay TV provider. In Q3 2025, vMVPDs added approximately 750,000 subscribers, bringing their total above 21 million.

Digital Sports Viewership Growth

Digital live sports audiences are projected to grow 5.8% year-over-year in 2026, far outpacing overall live sports viewership growth of just 0.4%. However, nearly 90% of sports viewing still happens on traditional TV or MVPDs, indicating that the full transition remains years away.

Ads placed in streaming-exclusive NFL games already outperform traditional TV, delivering 66% higher effectiveness than cable and broadcast averages—a signal that advertising dollars will continue flowing toward digital platforms. According to Trade Desk Intelligence research, 27% of Americans said they watch more live sports via connected TV (CTV) compared to 18% who watch more on traditional TV.

Content Expansion on Streaming Platforms

Sports programming on the five leading global SVOD services (Netflix, Amazon Prime Video, Apple TV+, Disney+, Paramount+) surged 72% since the end of 2024, according to Nielsen’s Gracenote. A follow-up report found sports content on these platforms grew 52% since January 2024, with Paramount+ leading after securing UFC rights—its sports offerings surged 219% year-over-year.

Key recent rights acquisitions across major streamers:

- Amazon Prime Video: 11-year NBA rights deal starting 2025–26, plus Thursday Night NFL, WNBA, and NWSL coverage

- Netflix: Exclusive US rights to NFL Christmas Day games, FIFA Women’s World Cup (2027, 2031), and WWE Raw

- Apple TV+: Major League Soccer (MLS Season Pass), all Formula 1 races starting 2026, and Friday-night MLB games

- Paramount+: CBS Sports content including NFL, March Madness, PGA Tour, UEFA Champions League, and exclusive UFC events starting 2026

- Peacock: Monday night NBA, college football, Olympic sports, and NBC-owned regional sports networks

- ESPN Unlimited: Launched August 2025 at $29.99/month, providing full access to all ESPN linear and digital sports content; gained 1.7 million sign-ups through October 2025

Regional Market Analysis

North America

North America is projected to hold the largest market share throughout the forecast period, driven by high internet penetration, strong sports culture, and aggressive rights acquisitions by both legacy networks and streamers. US sports media rights alone accounted for over half the global total in 2025. The market benefits from the NFL, NBA, MLB, and college sports ecosystem, which generate some of the most expensive rights deals globally.

Asia-Pacific

Asia-Pacific is the fastest-growing region, with multiple sources projecting CAGRs exceeding 15%. India dominates the region’s sports streaming growth, where cricket accounts for over 95% of sports media revenue. The IPL’s 2025 season drew 1.19 billion viewers across TV and digital platforms, with digital streaming outpacing linear TV for the first time—652 million viewers online versus 537 million on linear. CTV viewership of the IPL surged 44% year-over-year to 235 million viewers.

The IPL media rights cycle (2023–2027), valued at approximately $5.8 billion, represents one of the most valuable sports properties in the world. Upcoming new rights deals from 2027 for the IPL and ICC tournaments are expected to drive further value growth in the region.

Europe

European sports media rights spending is forecast to grow from $18.3 billion in 2025 to $21.3 billion by 2030. Growth is being fueled by global streamers entering European rights auctions—notably in the UEFA Champions League, where Amazon, Paramount, and Netflix have all bid for packages. The Premier League confirmed plans to bring international content production in-house for the 2026/27 season, potentially paving the way for its own streaming service.

Technology Trends Shaping the Market

AI-Driven Production and Personalization

AI is transforming sports broadcast workflows—from automated highlight generation and real-time metadata enrichment to personalized content recommendations. Streaming platforms are using AI-powered recommendation engines and language localization tools to enhance user engagement across diverse geographies. In 2025, AI proved valuable in focused production areas but has yet to deliver broader transformation across live broadcast workflows.

5G and Immersive Experiences

The rollout of 5G networks is enabling sub-second latency streaming and immersive features such as multi-camera angle selection. VR and AR technologies are gaining traction, allowing fans to experience virtual stadium views from anywhere. BytePlus has been testing volumetric encoding with claimed 50% bandwidth savings on immersive feeds, signaling future quality leaps.

Multi-Feed and Multi-Format Delivery

2025 marked the end of the single-feed era, as rights holders now design for multi-feed, multi-format delivery as the baseline expectation for modern sports broadcasting. This shift is powered by flexible cloud production, scalable IP video transmission, and the ability to generate multiple parallel versions of the same event for different platforms and formats.

Mobile-First Consumption

Mobile endpoints accounted for 55.2% of the live streaming market in 2025, driven by commute-time consumption peaks and the launch of foldable devices that lengthen dwell times. In India, nearly 90% of IPL streaming consumption occurred on mobile devices.

Key Market Players

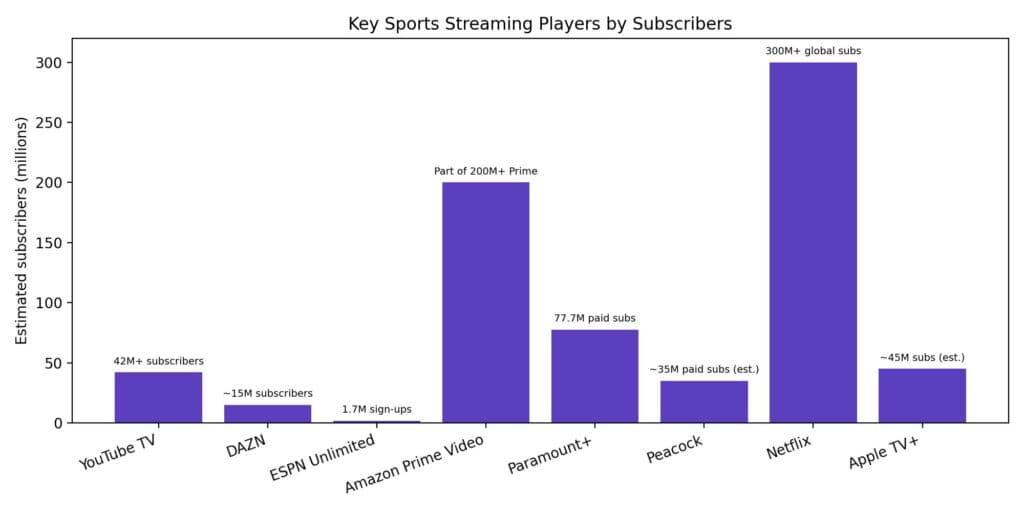

| Company | Key Sports Properties | Estimated Subscribers | Global Share |

| YouTube TV | NFL Sunday Ticket, NBA, MLB, college | 42M+ subscribers | ~14% |

| DAZN | Football (Europe), boxing, MMA, FIFA Club World Cup | ~15M subscribers | ~12% |

| ESPN Unlimited | NFL, NBA, MLB, college, WWE (2026+) | 1.7M sign-ups (launch–Oct 2025) | Emerging |

| Amazon Prime Video | NFL TNF, NBA, WNBA, NWSL | Part of 200M+ Prime | Major |

| Paramount+ | NFL/CBS, March Madness, UFC (2026+), UCL | 77.7M paid subs | Major |

| Peacock | NFL/NBC, NBA, Olympics, Premier League | ~35M paid subs (est.) | Major |

| Netflix | NFL Christmas Day, FIFA Women’s WC, WWE Raw | 300M+ global subs | Emerging sports |

| Apple TV+ | MLS, F1 (2026+), MLB Friday Night | ~45M subs (est.) | Niche sports |

Sources:

Challenges and Risks

- Fragmentation fatigue: Fans must subscribe to multiple platforms to follow their favorite teams, with 69% of viewers already watching some live games on streaming. The proliferation of exclusive deals increases total consumer spending and may drive piracy.

- Rising rights costs: Sports rights inflation may outpace revenue growth for some platforms. The $78 billion projected global rights bill by 2030 creates pressure on profitability.

- Retention challenges: Sports-driven subscriber spikes are often seasonal. During the NFL’s 2023–24 seasons, Paramount+ saw 41% higher daily sign-ups, but retention post-season remains a challenge.

- vMVPD slowdown: Despite overall growth, virtual MVPDs saw a 12% decrease in sign-ups in late 2025 as dedicated sports streamers like ESPN Unlimited and Fox One captured new demand.

- Piracy: High content acquisition costs and platform fragmentation continue to fuel sports piracy, particularly in emerging markets.

Outlook Through 2033

The sports streaming market is entering its most transformative phase. Several macro forces will shape the 2026–2033 period:

- NFL renegotiation upside: Although current deals run through 2034, the NFL believes its rights are undervalued. Early renegotiation discussions expected in 2026 could significantly increase global rights valuations.

- India’s next cricket cycle: New IPL and ICC tournament rights from 2027 will reset Asian market valuations, building on the IPL’s already record-breaking viewership numbers.

- Major event catalysts: The 2026 FIFA World Cup (US/Mexico/Canada), 2028 Los Angeles Olympics, and 2030 FIFA World Cup will drive subscription spikes and rights fee escalation.

- Consolidation: The Disney-Reliance joint venture in India ($8.5 billion) and DAZN’s acquisition of Foxtel in Australia signal that consolidation will continue as platforms seek scale.

- Advertising growth: As CTV sports viewership expands, ad-supported models will increasingly complement subscription revenue, with streaming sports ads already outperforming traditional TV in effectiveness.

The consensus across all major research firms is that the sports streaming market will at least double from 2024 levels by the early 2030s, with growth rates ranging from 9% to 25% CAGR depending on market scope. The convergence of technological innovation, changing viewer habits, and escalating competition for premium live content ensures that sports streaming will remain one of the most dynamic segments of the global media landscape through 2033.