Subscription fatigue has escalated from an emerging consumer annoyance into a measurable, market-shaping force in 2026. The global subscription economy has grown to an estimated $330 billion, but that expansion masks intensifying consumer pushback. Nearly half (47%) of consumers say they pay too much for streaming services, 87% of Gen Z report feeling some level of subscription fatigue, and SaaS cancellation rates climbed 23% year-over-year in 2025. The gap between what consumers think they spend ($86/month) and what they actually spend ($219/month) underscores a systemic visibility problem fueling frustration. In response, the industry is pivoting toward bundling, usage-based pricing, AI-driven retention, and regulatory reform — while consumers, especially younger ones, are rediscovering physical media as a counterpoint to digital overload.

The Subscription Economy by the Numbers

Market Scale

The subscription economy continues to expand, reaching an estimated $330 billion in 2026, with a 12% annual growth rate. Broader projections place the global subscription economy at $557.8 billion in 2025, scaling to $1.94 trillion by 2035 at a 13.3% CAGR. The subscription billing management market alone grew 19.2% to $10.92 billion in 2026. Despite fatigue signals, the model itself is not in decline — it is being stress-tested.

Consumer Spending Patterns

The average American consumer holds 4.5 active subscriptions and pays $924 annually for them. A 2025 CNET survey found U.S. adults spend roughly $90 per month ($1,080 annually) on subscriptions, with approximately $17 per month ($200 per year) going toward services they no longer use. Millennials lead in spending at about $101 per month. American households maintain an average of 12 digital subscriptions across all categories, with 4 paid streaming video-on-demand (SVOD) services per subscribing household.

| Metric | Figure | Source |

| Average active subscriptions | 4.5 per consumer | Forbes via Fortune |

| Average annual subscription spend | $924 | Forbes via Fortune |

| Average monthly spend (U.S. adults) | $90 | CNET 2025 Survey |

| Wasted spend on unused services | ~$200/year | CNET 2025 Survey |

| Perceived vs. actual monthly spend | $86 vs. $219 | C+R Research |

| Average SVOD services per household | 4 | Deloitte 2025 |

| Average digital services per household | 12 | Swell |

Consumer Sentiment: The Fatigue Indicators

Price Sensitivity and Value Perception

Deloitte’s 2025 Digital Media Trends survey of 3,595 American consumers found that 41% believe streaming content is not worth the price — up 5 percentage points from 2024. Meanwhile, 47% say they pay too much for the streaming services they use. The average cost subscribers report paying has risen 13% year-over-year, from $61 to $69 per month for SVOD services. Perhaps most alarming for providers: a price hike of just $5 would make 60% of consumers likely to cancel their favorite SVOD service.

Cancellation Behavior

Churn remains persistently high. According to Deloitte, 39% of consumers canceled at least one paid SVOD service in the last six months, a figure that has remained relatively stable for several years. In MarketWatch’s 2024 survey, 40.3% reported having cancelled a subscription service, with video streaming (54.5%) being the most commonly cancelled category, followed by music streaming (22.9%). Notably, 50.5% of customers reported resubscribing to services they had previously cancelled, indicating a “churn and return” cycle rather than permanent departures.

The Hidden Cost Problem

C+R Research uncovered one of the most telling data points: consumers estimated their monthly subscription spend at $86, but itemized spending averaged $219 — a $133 monthly gap. Additionally, 74% said recurring charges are easy to forget, and 42% admitted to paying for subscriptions they no longer used. This visibility gap is a core driver of subscription fatigue, as frustration compounds when consumers eventually confront the true scale of their commitments.

Generational Divide: Gen Z Leads the Backlash

The 87% Fatigue Rate

Gen Z (aged 18–29) has emerged as the demographic most acutely affected by subscription fatigue. CivicScience data from early 2026 shows that 87% of Gen Z respondents reported feeling some level of fatigue with the subscription economy. Between December 2025 and January 2026, 37% of Gen Z subscribers said they had canceled one or more streaming services explicitly due to subscription fatigue, and another 29% planned to do so soon. Just 13% reported no feelings of subscription fatigue at all.

Strategic Churning

Gen Z’s relationship with subscriptions is defined by intentional, rapid cycling. Roughly 8 in 10 Gen Z streamers signed up for a subscription specifically to watch a show, then canceled or paused it — a rate far higher than older cohorts. Despite this churn, 56% of Gen Z maintained three or more SVOD subscriptions, and 28% carried two. Gen Z is also the most likely age group to report spending $100+ per month on subscriptions, making their fatigue a function of both volume and cost.

Coping Strategies

To manage costs, 52% of Gen Z streamers used ad-supported subscription tiers as of January 2026. Streaming bundles are also gaining traction, with 37% of Gen Z streamers actively using a bundle and another 32% expressing interest in signing up for one. Subscription growth across major streamers dipped to 7% last year, down from 12% in 2024 — the first recorded year of single-digit growth, per Antenna data.

Millennials Under Pressure

Millennials are not far behind Gen Z. Deloitte found that millennials have the highest churn rate at 51% in the last six months, and they hold an average of 5 paid SVOD services — having seen a 20% increase in costs. Millennials also lead in total subscription spending at $101 per month, though this figure declined from $119 the prior year.

SaaS and Enterprise Subscription Fatigue

Subscription fatigue is not limited to consumers. The enterprise software market faces its own reckoning. The average business now uses 137 SaaS applications, while mid-sized companies may deploy over 200 different apps. This software sprawl has driven measurable consequences:

- SaaS cancellation rates increased 23% year-over-year in 2025

- Average customer lifetime decreased from 24 months to 18 months

- SaaS valuation multiples are compressing from 10–12x revenue (2023) to 5–7x revenue (2026)

- The overall churn rate for subscription companies stands at 3.27%, comprising 2.41% voluntary and 0.86% involuntary churn

AI is accelerating this shift. Businesses increasingly question the value of multiple specialized SaaS tools when AI agents can potentially consolidate functions. As one industry analysis noted, “Why pay for five different tools for writing, coding, and scheduling when one AI agent can potentially do it all?”. Surveys indicate 85% of SaaS firms are now mixing in usage-based pricing to combat churn.

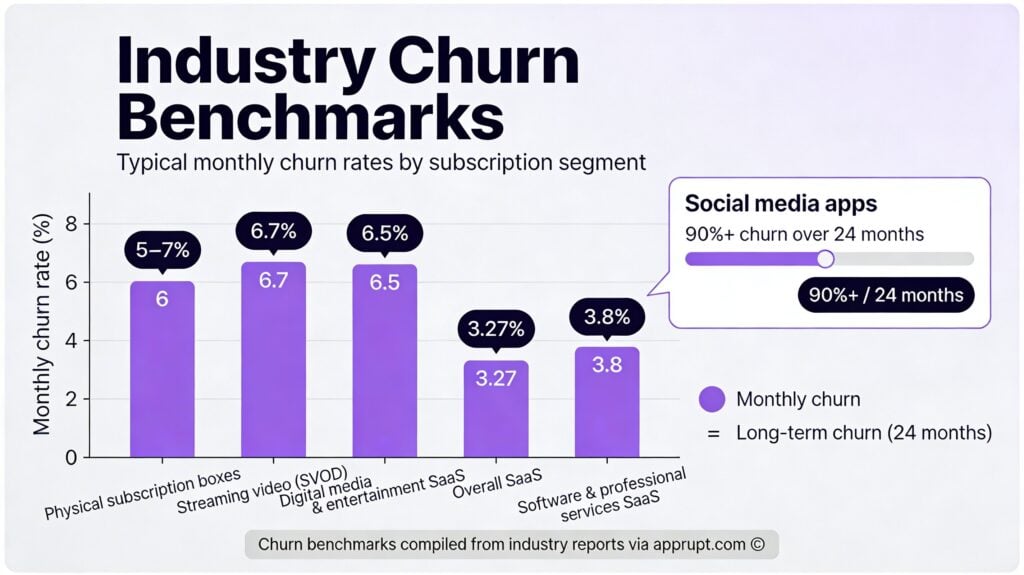

Industry Churn Benchmarks

| Segment | Monthly Churn | Key Metric |

| Physical subscription boxes | 5–7% | Industry average |

| Streaming video (SVOD) | 6.7% | Industry average |

| Digital media & entertainment SaaS | 6.5% | Category average |

| Overall SaaS | 3.27% | 2.41% voluntary + 0.86% involuntary |

| Software & professional services SaaS | 3.8% | Category average |

| Social media apps | 90%+ over 24 months | Long-term retention challenge |

At 6% monthly churn — the industry average for physical subscription boxes — a business loses nearly half its subscriber base every year, requiring constant acquisition just to maintain flat revenue.

Industry Response: Bundling, Flexibility, and AI

The Bundling Wave

Bundling has emerged as the dominant counter-strategy to subscription fatigue. Bundled subscriptions now account for over a third of all U.S. subscriptions, and 57% of subscribers have at least one bundle. The retention math is compelling: customers who sign up with multiple subscriptions at once retain at 76%, compared to 40% for single-subscription customers. Even those who upgrade to multiple subscriptions post-signup retain at 52%. Bundling reduces churn by an estimated 34%.

Major industry examples include Fox One and ESPN’s multi-product bundle, Netflix and HBO Max through Verizon, and Disney+, OSN+, and Shahid’s 3-for-2 offer in the Middle East. Retailers like Walmart+ offer Peacock and Paramount+ through their loyalty schemes. In 2026, the consensus is that bundling will outpace pure subscriber growth.

AI Subscriptions: The New Frontier

A notable emerging category is paid AI subscriptions (ChatGPT Plus, Runway, etc.), which are gaining particular traction among 18–25-year-olds. At MWC 2026, Bango identified AI subscriptions as a “perfect alternative” to SVOD for telco bundling, noting their high demand, premium pricing, and low take-up of pro tiers, making them ideal for hard bundles. However, over 56% of those already paying for AI subscriptions cannot afford all the subscriptions they would like, and over 70% would prefer AI subscriptions bundled through their mobile service or bank.

Usage-Based and Hybrid Pricing

The rigid monthly subscription is giving way to more flexible models. Usage-based pricing — charging based on actual consumption (logins, data processed, API calls) — is being adopted by 85% of SaaS firms. Hybrid models add a low base fee with usage tiers, allowing light users to save while power users scale naturally. Annual plans provide another lever, reducing churn by 40% compared to monthly billing and eliminating eleven monthly billing events that each represent a cancellation opportunity.

AI-Powered Retention

AI-based churn prediction has become a core retention tool for 2026. Models analyze behavioral data — declining engagement, changes in usage patterns — to identify at-risk customers before they decide to cancel. This enables proactive interventions including personalized offers, relevant guidance, or reminders of a service’s value. Enterprises adopting AI-enabled billing systems have reported up to a 30% reduction in involuntary churn through predictive billing failure alerts and smart retry logic.

Pause Functionality

What was once a niche feature is becoming a standard expectation. Pause functionality allows subscribers to temporarily suspend rather than permanently cancel, serving as a psychological retention buffer. Even though the subscriber churns temporarily, they maintain a self-identity as a customer who will return — shifting the focus from churn metrics to customer lifetime value (CLV).

The Analog Rebellion: Physical Media Resurgence

Subscription fatigue has fueled an unexpected countertrend: the return of physical media, led by Gen Z. Vinyl record revenues grew 7% to $1.4 billion in 2024, marking the 18th consecutive year of growth. Since 2016, vinyl album sales have increased from 13.1 million to 49.6 million units in 2023. Three-quarters of Gen Z vinyl fans buy records at least monthly, and 80% own a turntable.

Physical video media is also stabilizing. Physical media sales declined just 9% in 2025, compared to drops of over 20% in 2023 and 2024. Non-profit video rental stores like Vidiots in Los Angeles now rent over 1,000 movies per week — numbers exceeding even their peak in the early 2000s — with the average customer age skewing dramatically younger.

The motivation is both economic and philosophical. Half of Gen Z vinyl fans said they collect records to get a break from digital life, and 61% replace digital habits with vinyl listening to improve mental well-being. As one consumer put it: “Anything that’s digital is never yours. Amazon’s not going to come into your house and take your DVD movies”.

Regulatory Landscape

Consumer dissatisfaction has spurred regulatory action. The FTC finalized its “Click-to-Cancel” rule in October 2024, requiring cancellation to be as easy as signup. However, the Eighth Circuit Court of Appeals vacated the rule in July 2025, citing procedural flaws. Despite this setback, the regulatory momentum has not stalled:

- A bipartisan “Unsubscribe Act” was introduced in the U.S. House in January 2026, complementing a Senate proposal from July 2025

- Over half of U.S. states already have laws echoing click-to-cancel principles

- The FTC reported an average of nearly 70 consumer complaints daily about subscription practices in 2024, up from 42 per day in 2021

- The FTC is expected to re-issue a corrected version of the rule, and most compliance teams are preparing accordingly

- Visa and Mastercard now require online cancellation options, clear billing disclosures, and cancellation confirmations

In early 2026, the FTC intensified its scrutiny of auto-renewal practices and signaled a revival of rulemaking, keeping enforcement risk elevated for subscription businesses.

India’s Subscription Economy: Growth with Emerging Fatigue Signals

India represents the fastest-growing major subscription market, expanding at a 16.6% CAGR, driven by rapid smartphone adoption, growing internet connectivity, and an expanding middle class. The country has 601 million OTT users, with approximately one in four paying for at least one subscription. Digital media generated Rs 802 billion in revenue in 2024.

However, growth is moderating. OTT subscription growth dropped from 13–14% to 10%, which companies are characterizing as “market maturity”. Subscription-based fintechs are projected to grow revenue 2.5x faster than transaction-based counterparts by 2026. India’s 1.03 billion internet users and 500 million social media identities create a massive addressable market, but price sensitivity remains acute, requiring localized, affordable subscription models.

Key Drivers of Subscription Fatigue

The forces behind subscription fatigue in 2026 operate across financial, cognitive, and structural dimensions:

- Cost accumulation: Rising prices across services — SVOD costs up 13% year-over-year — compound across multiple subscriptions, creating genuine financial strain.

- Value erosion: 41% say content is not worth the price, driven by content fragmentation, especially in sports where fans need multiple services to follow a single team.

- Cognitive overload: Managing 12+ digital subscriptions alongside 137 SaaS tools in the workplace creates decision fatigue and behavioral burnout.

- Visibility gaps: The $133/month gap between perceived and actual spend means fatigue often builds unconsciously before surfacing as abrupt cancellation waves.

- Dark patterns: Difficult cancellation processes, hidden renewal charges, and auto-renewal inertia erode trust. Around 60% of consumers avoid new signups because they expect cancellation to be difficult.

- Loss of ownership: Consumers increasingly recognize that digital subscriptions confer access, not ownership — licenses that can be revoked.

Outlook: What Comes Next

The subscription economy in 2026 is at an inflection point. The era of “everything-as-a-subscription” — from fitness classes to meditation apps to recipe platforms — is being curtailed by consumer pragmatism. Companies that relied on passive engagement (assuming users would forget to cancel) are seeing this strategy collapse as fintech tools and banking apps now offer subscription tracking and cancellation features.

Several trends will shape the next phase:

- Consolidation through bundling will accelerate, with telcos, retailers, and payment platforms becoming the primary distribution points for digital subscriptions.

- Usage-based pricing will gain dominance in SaaS, aligning cost with actual consumption and reducing the “paying for unused features” frustration.

- AI-powered retention will become table stakes, with predictive churn models and automated intervention flows replacing blunt discount strategies.

- Regulatory tightening is inevitable, whether through a revised federal rule or the growing patchwork of state laws and payment-network requirements.

- Physical media will continue its niche resurgence, serving as both an economic alternative and a cultural statement against digital saturation.

- The “forever subscription” — services so embedded in daily life that cancellation is unthinkable — will coexist with aggressive churning of everything else; 70% of consumers already have at least one subscription they will never cancel.

The winners in 2026 will be subscription businesses that integrate data, payments, billing, and customer experience into cohesive strategies centered on demonstrable value. The fundamental challenge has shifted: it is no longer about signing customers up, but about giving them a reason to stay.