Free trials have been a foundational acquisition strategy in the streaming industry, though the landscape has shifted dramatically in recent years. Major platforms like Netflix and Disney+ have eliminated free trials, while others like Hulu and Amazon Prime Video continue offering 30-day trials as key competitive differentiators. Conversion rates from free trials to paid subscriptions in streaming range from 58% to 78% depending on the study, significantly higher than the SaaS industry average. Meanwhile, monthly churn rates across the video streaming industry have surged from 2% in 2019 to 5.5% by early 2025, with 23% of the U.S. streaming audience qualifying as “serial churners” who rotate services and exploit free trial windows.

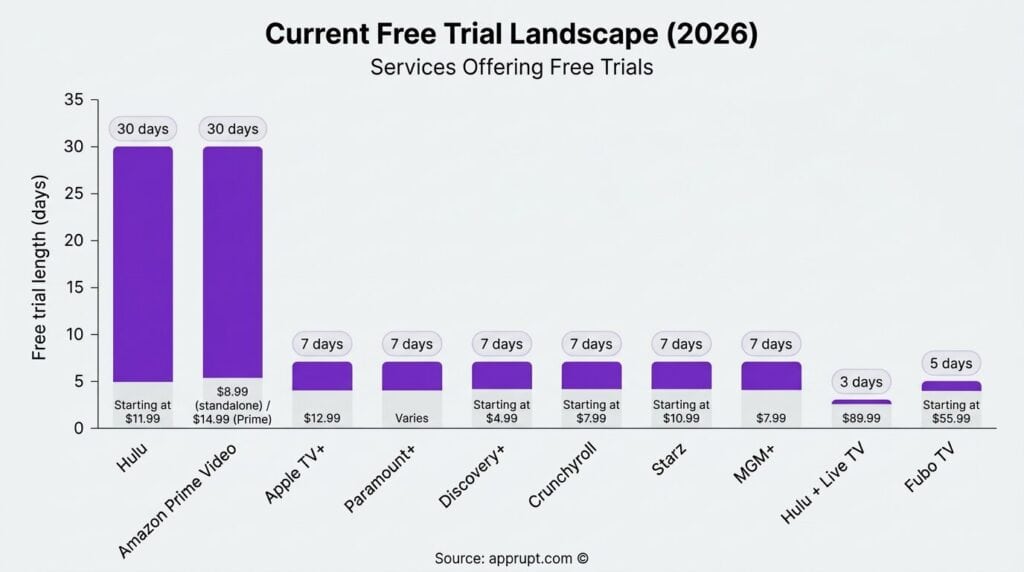

Current Free Trial Landscape (2026)

Services Offering Free Trials

Not all major streaming services offer free trials in 2026. The availability and duration of trials vary significantly across platforms.

| Service | Free Trial Duration | Monthly Price (Post-Trial) |

| Hulu | 30 days | Starting at $11.99 |

| Amazon Prime Video | 30 days | $8.99 (standalone) / $14.99 (Prime) |

| Apple TV+ | 7 days | $12.99 |

| Paramount+ | 7 days | Varies |

| Discovery+ | 7 days | Starting at $4.99 |

| Crunchyroll | 7 days | Starting at $7.99 |

| Starz | 7 days | Starting at $10.99 |

| MGM+ | 7 days | $7.99 |

| Hulu + Live TV | 3 days | $89.99 |

| Fubo TV | 5 days | Starting at $55.99 |

Hulu stands out with its 30-day trial — the most generous among dedicated streaming platforms — while Amazon Prime Video matches this with its own 30-day offer available to both new and returning members.

Services That Eliminated Free Trials

Several major platforms have discontinued direct free trials:

- Netflix ended its 30-day U.S. free trial in October 2020, after having more than 192 million global subscribers. A spokesperson cited exploration of “different marketing promotions” to attract new members. However, as of early 2026, Netflix appears to have reintroduced a 7-day free trial in certain markets.

- Disney+ removed its free trial in June 2020 ahead of the premiere of Hamilton, citing its “compelling entertainment offering” and “attractive price-to-value proposition” as sufficient without a trial. Disney+ does not currently offer a standalone free trial, though limited access is available through a 3-day Hulu + Live TV trial.

- Max (formerly HBO Max) does not offer a direct free trial, though carrier bundles and promotional partnerships sometimes include trial access.

- Peacock does not offer a standard free trial directly, but can be accessed free through Walmart+ membership or Instacart Plus bundles.

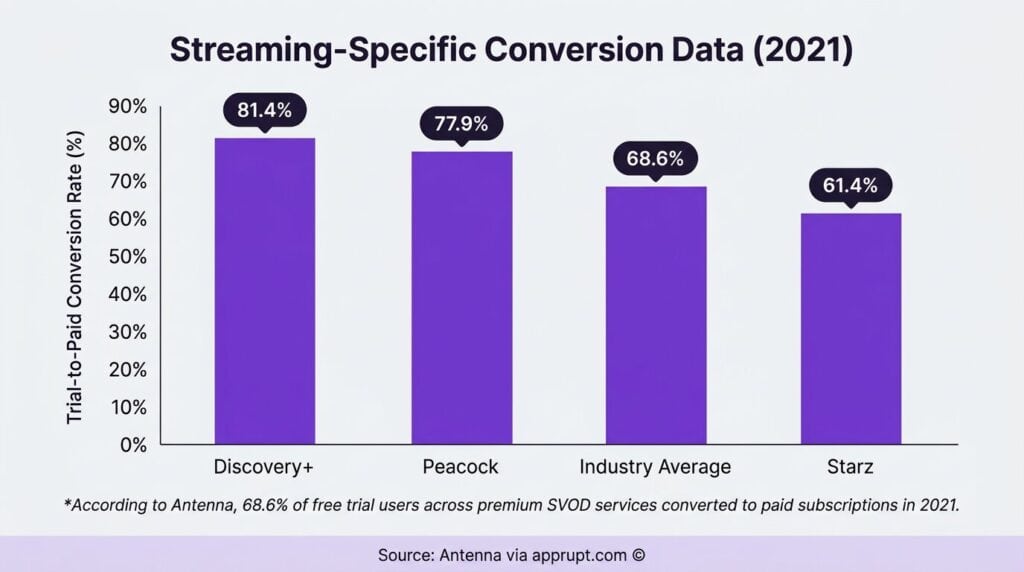

Free Trial Conversion Rates

Streaming-Specific Conversion Data

Free trial conversion rates in the streaming industry are substantially higher than in other subscription sectors. According to Antenna data, 68.6% of free trial users across premium SVOD services converted to paid subscriptions in 2021, up from 66.3% the prior year. Individual platform conversion rates varied considerably:

| Platform | Trial-to-Paid Conversion Rate (2021) |

| Discovery+ | 81.4% |

| Peacock | 77.9% |

| Industry Average | 68.6% |

| Starz | 61.4% |

Broader industry studies place the streaming free trial conversion rate between 58% and 78%. Market.us reports that approximately 60% of users who sign up for free trials end up converting to paid subscriptions. Netflix historically boasted an exceptionally high conversion rate of 93% during its free trial era, while Amazon Prime Video achieved around 73%.

Total Trial Volume

The U.S. premium SVOD category generated approximately 61 million trial sign-ups in 2021, a slight increase from 60.4 million in 2020 — this despite Disney+ and HBO Max not offering free trials during that period. Promotional price sign-ups surged from 3.3 million in 2020 to 8.4 million in 2021, indicating a shift toward discounted introductory offers as a complement or alternative to free trials.

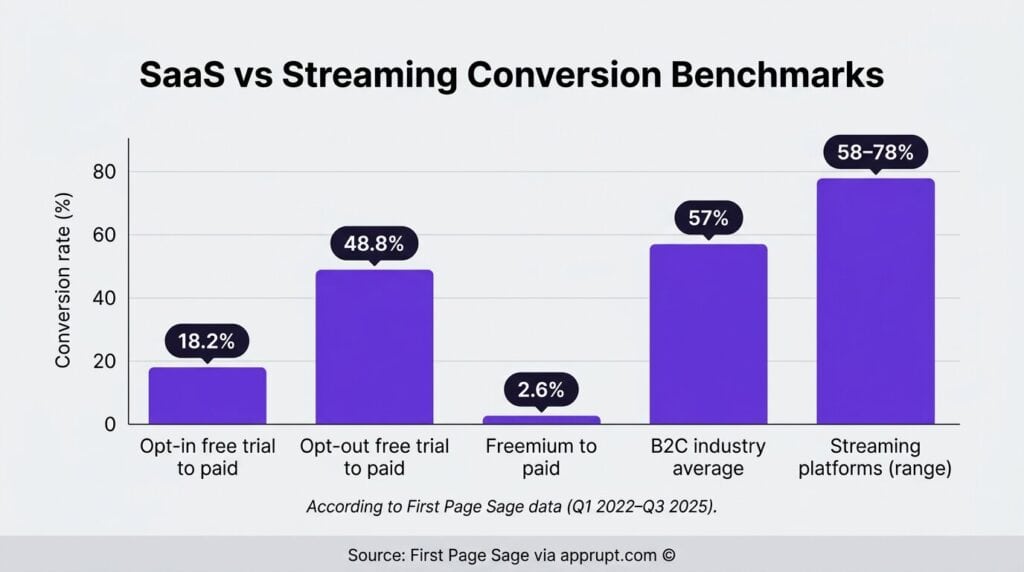

Comparison With SaaS Industry Benchmarks

Streaming conversion rates far exceed SaaS averages. According to First Page Sage data (Q1 2022–Q3 2025):

| Model Type | Conversion Rate |

| Opt-in free trial to paid | 18.2% |

| Opt-out free trial to paid | 48.8% |

| Freemium to paid | 2.6% |

| B2C industry average | 57% |

| Streaming platforms (range) | 58%–78% |

The higher streaming conversion rate is attributed to the opt-out model most services use (requiring credit card upfront), the habitual nature of content consumption, and the endowment effect — users develop attachment to the service during the trial.

Consumer Behavior Around Free Trials

Forgotten Cancellations

Free trials rely partly on consumer inertia. A 2025 CableTV.com survey of 1,000 Americans found that 48% have forgotten to cancel a free trial and accidentally paid more than expected. Among those who forgot, 48.1% said it had happened multiple times. Millennials and Gen Z were the most forgetful, with 65% and 59% respectively reporting at least one forgotten cancellation.

Of those who accidentally let trials expire, 43.7% were charged between $20 and $50, while 9% spent over $100 on accidental subscriptions. This pattern is one reason 42% of consumers report still paying for subscriptions they no longer use.

Serial Churning and Trial Exploitation

Serial churners — subscribers who cancel three or more services within two years — now represent 23% of the U.S. streaming audience. These consumers chase free trials, time subscriptions around new season releases, and cancel after finishing target content. However, less than 6% of subscribers are classified as “serial offenders” who cancel four or more services during free trial periods within a 12-month window.

Role of Trials in Subscription Decisions

Free trials remain an important factor in consumer decision-making. Antenna’s 2024 insights found that among factors consumers consider when signing up for a new service, 74% cite cost, 51% content variety, and 31% the availability of free trials. A McKinsey report found that 68% of subscribers prioritize trial offerings as a key factor in subscription decisions. Meanwhile, 75% of direct-to-consumer businesses now offer some form of free trial.

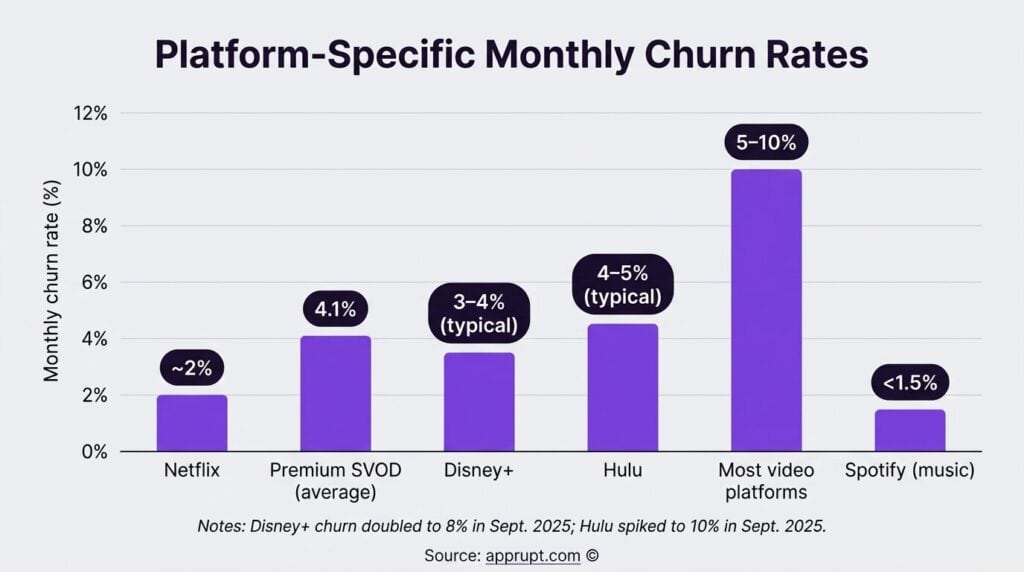

Churn Rate Benchmarks

Industry-Wide Trends

Monthly churn rates across the streaming industry have climbed significantly over recent years. The average monthly churn jumped from 2% in 2019 to 5.5% by early 2025. The annual churn rate for video streaming now stands at approximately 40%, compared to just 12% for audio streaming.

Platform-Specific Churn Rates

| Platform | Monthly Churn Rate | Notes |

| Netflix | ~2% | Lowest among video platforms |

| Premium SVOD (average) | 4.1% | Q2 2025 data |

| Disney+ | 3–4% (typical); 8% (Sept. 2025 spike) | Doubled during Kimmel controversy |

| Hulu | 4–5% (typical); 10% (Sept. 2025 spike) | Reported a 35% drop in cancellations in Q1 2025 |

| Most video platforms | 5–10% | Broad range depending on content and pricing |

| Spotify (music) | <1.5% | Lowest among all subscription services |

Churn Drivers

Cost is the primary reason subscribers cancel, cited by 45% of users. Since 2021, the average cost for ad-free streaming has risen 54%, outpacing inflation and wage growth. Subscription prices surged 25% in the past year alone, with platforms increasing rates by an average of 9% annually. Other major churn factors include:

- Content completion: 26% of subscribers cancel after finishing the content they came for.

- Content fragmentation: One-third of consumers report fragmentation across platforms damages their TV experience, rising to 40% among the 25–34 age demographic.

- Decision fatigue: Consumers spend an average of 14 minutes searching for content per viewing session, and 49% are willing to cancel a service when finding something to watch takes too long.

Strategies Replacing Free Trials

Ad-Supported Tiers

As free trials decline, ad-supported tiers have emerged as a powerful acquisition and retention tool. Nearly 46% of subscriptions are now ad-supported among SVOD services offering both tiers, with ad-supported subscriptions growing 32.7% year-over-year. Some 71% of net additions over the past nine quarters came from ad-supported plans. Ad-supported net adds grew from 19.8 million in 2023 to 27.4 million in 2024.

Bundling

Bundling has become the single most powerful retention strategy in streaming. Disney+ and Hulu’s combined bundle reduced churn significantly, and new partnerships like the Apple TV+ and Peacock bundle ($14.99/month) offer consumers consolidated value. Bundled subscribers are 59% less likely to churn than single-service subscribers, according to industry research.

Promotional Pricing

Promotional offers are increasingly replacing traditional free trials. Showtime attracted nearly 20% of its 2021 sign-ups at a promotional price. By Q4 2021, promotional price sign-ups accounted for over 13% of all streaming sign-ups. Platforms now frequently offer discounted first months ($0.99–$1.99) or extended promotional periods instead of free trials.

Password-Sharing Crackdowns

Netflix’s password-sharing crackdown in mid-2023 initially triggered cancellations but ultimately led to 50 million net new subscribers between late 2023 and Q4 2024, growing from 238 million to over 300 million globally. Disney followed with similar measures in 2025.

Market Context

Subscriber Growth

U.S. streaming subscriptions climbed 10% in Q2 2025, reaching 339 million, while individual CTV users grew 8% year-over-year to 177 million. Premium streamers (Apple TV+, Disney+, Netflix, etc.) account for 79% of all streaming subscriptions. As of mid-2025, Disney+ had 128 million core subscribers and Hulu had 55.5 million.

Stabilization Trend

The streaming industry appears to be entering a phase of more stable growth. Between Q4 2024 and Q1 2025, U.S. SVOD services gained 5 million net subscribers. Churn rates are decreasing, with over one-third of individuals who cancel an SVOD subscription resubscribing within the same year. This suggests the market is maturing beyond the volatile subscriber churn patterns of 2022–2024.

New Subscriber Acquisition

An average of 3.5 million new subscribers entered the premium SVOD market each quarter through the first three quarters of 2024, down from 4.3 million in 2023 and 4.8 million in 2022. Netflix captures the largest share, with 23% of new subscribers choosing it as their first premium SVOD service.

Key Takeaways

- 58%–78% of streaming free trial users convert to paid subscribers, with the industry average at approximately 68.6%.

- 48% of Americans have forgotten to cancel a free trial, resulting in unintended charges.

- 23% of the U.S. streaming audience are serial churners who cycle through services and free trials.

- Monthly churn has risen from 2% (2019) to 5.5% (2025), with cost cited as the #1 cancellation reason by 45% of users.

- Major platforms are increasingly replacing free trials with ad-supported tiers (46% of subscriptions), bundles, and promotional pricing.

- Total U.S. streaming subscriptions reached 339 million in Q2 2025, with premium services holding 79% market share.